Market Recap: Has US avoided recession in 2023? ECB also on tap.

Economic Indicators & Central Banks:

* Treasuries were weak with yields extending higher still, hit by the double whammy of stronger than expected PMI data and an ugly 5-year auction.

* The healthy rally on Wall Street also weighed, though stocks trimmed gains into the close.

* China bourses continued to rally after the PBOC stepped up support measures yesterday by cutting reserve requirements, while hinting at possible rate cuts.

* ECB Preview: The central bank is widely expected to keep policy settings unchanged and stick with a wait-and-see stance for now, which means rate cuts are not on the immediate agenda.

Market Trends:

* Hang Seng and CSI 300 already staged a late rally yesterday and continued to move higher today, with gains of 1.8% and 2.0% respectively.

* European futures are in the red, however, as the ECB meeting comes into view.

* US futures are slightly higher on the anticipation of US GDP later on which could provide clues as to where US rates might be headed.

* Tesla’s profits plummet! Tesla (-5.93% after hours) posted a 23% decline in profits for 2023, its 1st annual decline since 2017!

* Microsoft becomes 2nd company ever to top $3 trillion valuation on AI-driven rally. Apple remains at the top.

* FAA halts Boeing 737 MAXproduction expansion. Boeing -1.32% after hours.

Financial Markets Performance:

* The USDIndex slipped to a session nadir of 102.52 but bounced back to 103.25 to close over the 103 level for a 7th straight session.

* EURUSD is steady at 1.0880. The USDJPY regained some ground after hints at rate rises in Japan triggered selling in the Japanese government bond market. It remains below 148.

* USOIL was up 1.45% to $75.44 per barrel amid ongoing geopolitical risks and following a bigger than expected US inventory draw.

* Gold was down -0.83% to $2012.50 on the stronger PMI data and further trimming in rate cut bets. Markets have reined in expectations for early rate cuts in the US and Europe, and BoJ governor Ueda yesterday hinted that the exit from the negative interest rate environment is coming into view. That should keep gold range bound for now.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The Week Ahead – Earnings, Central Banks and Geo-Political Tensions!

* Tensions rise in the Middle East as three US Soldiers are killed in a base near the Syrian-Jordan border after being attacked by Iran-backed militants. Crude Oil price opens 1.15% higher.

* Gold rose 0.63% on Monday due to rising tension in the Middle east. Traders are evaluating whether the market will witness a “risk-off” sentiment this week.

* All eyes on the Federal Reserve’s press conference on Wednesday. Analysts expect the Federal Fund Rate to remain unchanged, but the Press Conference will signal the Fed’s future path.

* The US economy grew 3.3% in the latest quarter, beating expectations of 2.0%. In addition to this, Pending Home Sales rose 8.3% and the Core PCE Index rose from 0.1% to 0.2%.

XAUUSD – Geo-Political Tension Again on The Rise

The US Dollar Index did open Monday’s trading slightly higher, however, has fallen 0.10% over the past 2 hours as of the time of writing. Instead, investors are increasing exposure to Gold. Gold prices are trading 0.63% higher during this morning’s Asian Session and have risen above the most recent resistance levels. When evaluating technical analysis, the price of the commodity is trading above price sentiment indicators, above the neutral on most oscillators and above the day’s VWAP. Here we can see potential “buy” signals, however, investors also should note significant resistance points at $2,037.80. This level has triggered declines on eight occasions over the past month. If the price maintains momentum and crosses this level, Gold will move into the “buy” region of the Fibonacci levels.

The price is largely being driven by two factors: the decline in the Dollar and lower investor sentiment due to rising Middle East tensions. The group which conducted the attack is not yet known, however, President Biden has already advised the US will retaliate. According to the White House, the group is most likely an Iranian-backed militant group which is the main concern for investors. Though investors should note that this will only have a short-term effect if the situation does not escalate.

The next price drive will be the Federal Reserve’s Press Conference and the central bank’s forward guidance on interest rates. This will determine if institutions decide to further expose their funds to the Dollar or look for alternatives. The main alternatives will be Gold and US Bonds. If investors are unconvinced the Fed will keep rates high, Gold could benefit from a weaker Dollar. Tomorrow’s JOLTS Job Openings could also create further volatility.

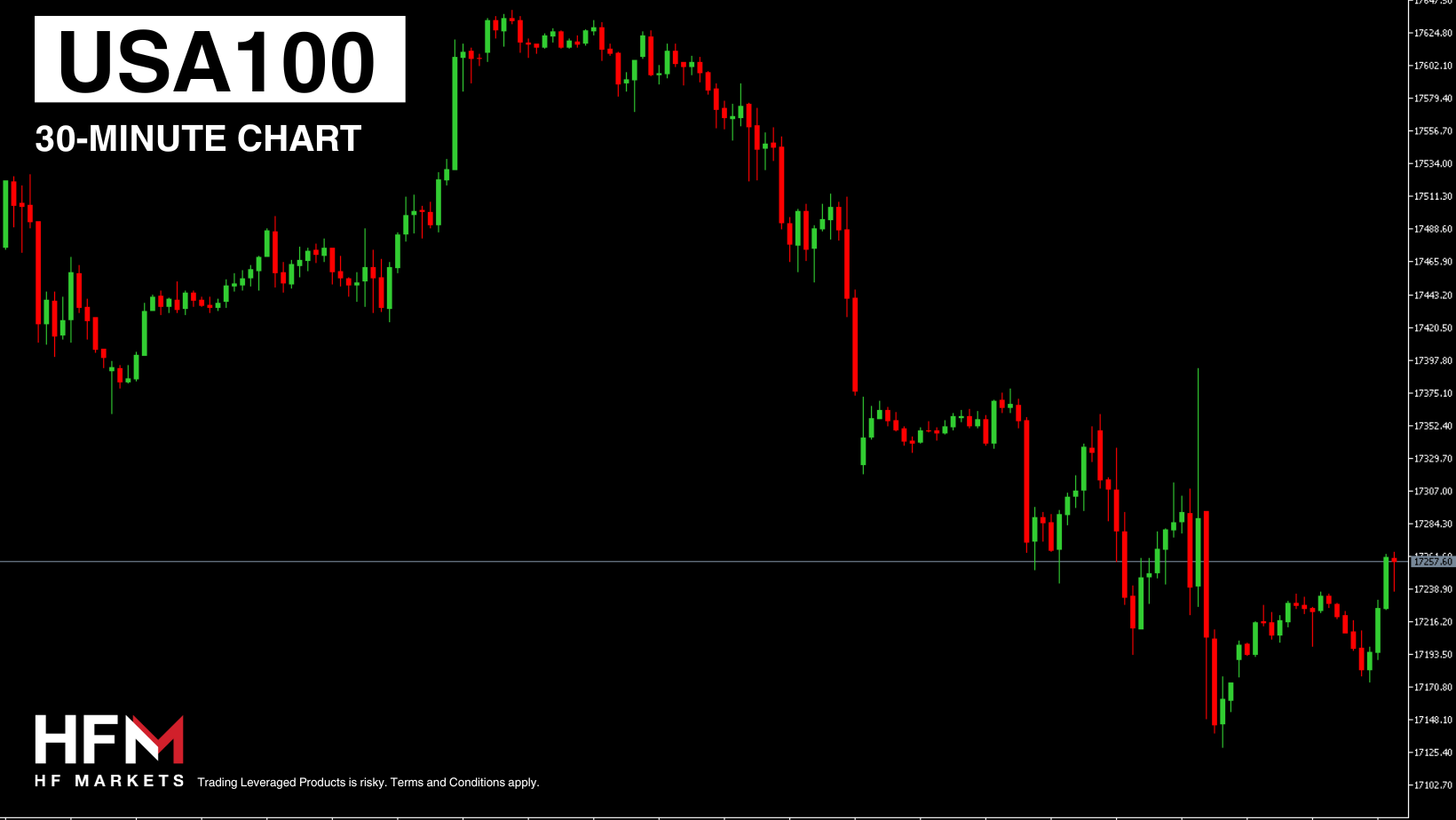

USA100 – Investors Eye Earnings and Fed Press Conference

US investors are concerned about the developments over the weekend and as a result the rising oil price. Another concern for investors is also if the Fed gives an ultra-hawkish signal on Wednesday after strong economic data last week. Last week, the US PMI rose higher than expectations as did the economy’s Gross Domestic Product. Though stocks and shareholders will equally be monitoring this week’s quarterly earnings reports from major companies.

Tuesday Quarterly Earnings Report

Microsoft – +1.01% over the past week.

Alphabet – +3.30% over the past week.

AMD – +1.58% over the past week.

Wednesday Quarterly Earnings Report

Apple – Unchanged over the past week.

Amazon – +1.35% over the past week.

Meta – +1.61% over the past week.

The performance of the USA100 will largely depend on whether the above earnings are higher than Wall Street’s expectations and on the Fed’s Press Conference. If the Fed is viewed as “ultra-hawkish”, stocks are likely to experience significant pressure if earnings do not exceed expectations.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The Yen Tops All Competitors and Investors Turn to Tech Earnings.

* Monday’s best performing currency was the Japanese Yen which took advantage of a lack of economic data and a rise in geopolitical tensions.

* Analysts advise institutions may increase exposure in the Yen due to geopolitical tensions. Japan’s unemployment rate declines to 2.4%, the lowest in 10-months.

* The USA100 rises ahead of tonight’s vital quarterly earnings reports. Of NASDAQ’s 20 most influential stocks, only three saw a slight decline.

* Tesla and Illumina were NASDAQ’s best performing stocks, rising more than 4% each.

USA100 – Microsoft and Alphabet Earnings Upcoming

The USA100 rose 1.21% on Monday as demand again rose ahead of major earnings from five of the “magnificent seven”. Tonight, investors await the quarterly earnings reports from Microsoft, which yesterday rose 1.43%, and Alphabet, which rose 0.68%. However, investors must also monitor the earnings data from AMD which is the 11th most influential stock for the index.

Even with the strong bullish price action over the past 4 weeks, investors should be cautious about short-term volatility. During this morning’s Asian session, the USA100 is trading 0.16% lower. US indices are known to decline towards the end of the US session and within the Asian session. However, if the price maintains momentum, sell signals can arise. On the 2-hour chart, the price is trading above the 75-bar Exponential Moving Average and above the “neutral” on the RSI. Both indicate strong buying sentiment. However, the latest candlestick is bearish meaning buy signals are not currently active. Fibonacci levels indicate support may be found between $17,505.88 and $17,5870. If the price rises above $17,633, signals will again arise.

So far this morning the US Dollar Index is trading lower, and bonds are increasing in value. Both are indications that the stock market can potentially gain. However, in order for the USA100 to see significant upward price movement, the index will also need to be supported by tonight’s earnings data.

XAUUSD – Fed’s Future Guidance Key For Gold

Gold is currently experiencing strong volatility in both directions but continues to see buyers overpowering sellers. If we look at the price action from the price gap, the commodity rose by 0.47% and from Friday’s close 0.72%. We can see here even with strong bearish volatility at times throughout the day, Gold still finalized a considerable increase. Gold’s price rose a further 0.15% during this morning’s session, but analysts are slightly cautious about the resistance level.

The resistance level at $2,040 has been intact throughout the whole month and was only temporarily able to break above this level. Nonetheless, trend and momentum indicators are signalling upward price movement. Today’s CB Consumer Confidence and JOLTS Job Openings will significantly influence the price action of the Dollar and subsequently Gold. If the two economic releases read higher than expectations, Gold can potentially correct back downwards. However, a lower figure can further fuel the upward movement due to its hedge against inflation and alternative to the Dollar.

According to the US Commodity Futures Trading Commission’s latest report, the number of buy contracts rose by 2.211 thousand and sell contracts fell 11.280 thousand. Here we can see a possible shift towards bullish speculation.

EURJPY – Japanese Yen Currently The Best Performance Currency

The best performing currency of the day and the week so far is the Japanese Yen. Investors are returning to the Japanese Yen as most currencies within the G7 are expected to cut rates in the upcoming months, whereas analysts expect the Bank of Japan to slightly increase rates just before the summer. According to fundamental analysts, the Yen’s haven status can also serve as an alternative to the Dollar while geopolitical tensions rise.

The Japanese Yen is increasing against all currencies but one of its strongest price movements is against the Euro. The Euro has been put under pressure from a dovish outlook set by investors, not necessarily the Central Bank representatives. In addition to this, France’s Flash GDP figures for the latest quarter read 0.0%, meaning the country was very close to officially being in a recession. Investors now turn to Germany and Italy. If both regions also see lower a lower gross domestic product growth rate, the Euro can experience further pressure.

The Japanese Yen on the other hand is likely to be influenced by three releases scheduled for tonight’s Asian Session. Japan will release the Bank of Japan’s Summary of Opinions, the Prelim Industrial Production and Retail sales. Higher data and a more hawkish central bank can support the Yen further, as did today’s Japanese Unemployment Rate. Japan’s unemployment rate today fell from 2.5% to 2.4%. investors also should note that weaker US data can also support the Japanese Yen indirectly.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

US Technology Stocks Decline Ahead of the Fed’s Press Conference.

* US Technology Stocks decline ahead of the Fed’s interest rate decision and press conference. Only the Dow Jones witnessed bullish price movement during the US session.

* Both Microsoft and Alphabet beat earnings and revenue expectations, but stocks declined. Find out why below.

* The Euro rose in value against all currencies on Tuesday, but the region’s Gross Domestic Product continues to indicate stagnation and a risk of a recession.

* The US Dollar Index trades higher but US Bond yields fall to weekly lows.

USA500

The SNP500 fell 0.33% during yesterday’s trading session and formed a 0.10% bearish gap during this morning’s Asian session. The price has since formed a price range which traders can use as a breakout level at $4,909.11 and $4,901.40. The decline in the index was largely triggered by the upcoming Federal Reserve Press Conference and “profit taking”, according to analysts.

Overnight the market focused on the quarterly earnings reports from Microsoft and Alphabet. Microsoft is the most influential stock and holds a weight of 7.31%. Microsoft stocks fell by 0.28% before the announcement and a further 0.25% after the announcement. Volatility levels were relatively low and according to analysts, the upcoming Fed announcement may potentially be the reason why. In addition to this, Microsoft did not add anything particular to their forward guidance which disappointed investors.

Microsoft Earnings beat expectations by 5.80% and Revenue by 1.45%. In addition to this, investors are also cautious about the fact that growth is largely being witnessed in the Azure and cloud services. Whereas the other 7 sectors are seeing relatively lower growth. Bloomberg advises the company earnings are solid and do not indicate a need for a selloff or significant decline. However, neither do we have any indications of upward price movement.

Alphabet stocks on the other hand saw a larger decline after their earnings report was published. The earnings per share figure was 2.50% higher than expectations and revenue only 1%. Even though the earnings were higher than expectations, shareholders were still largely disappointed. The previous 4 quarters saw earnings beat between 7% and 10%. According to analysts, investors took this as an opportunity to cash in profits and so there was no need to hold onto positions for the time being.

Of the USA500’s most influential 10 stocks, only 2 ended the day higher and from the 50 most influential stocks 28 rose in value. Here we can see that the individual stocks and components are not giving a clear picture and most likely tonight’s Fed comments will determine the price movement over the next 24-48 hours.

EURUSD

The Euro saw moderate increases against all currencies during the European session but lost momentum once the US session opened. However, the price this morning is showing much stronger volatility in favor of the Dollar. In addition to this the US Dollar Index is rising in value during this morning’s Asian Session. So, are investors increasing their exposure to the Dollar ahead of tonight’s Federal Reserve decision, statement, and press conference? Traders will monitor if this will be the pattern for the day.

The Dollar is once again being supported by considerably stronger than expected economic data. JOLTS Job Openings rose from 8.93 million to 9.03 million, higher than the previous 2 months and higher than expectations. In addition to this the CB Consumer Confidence also rose to its highest level since December 2021. If the Federal Reserve Chairman, Jerome Powell, gives a more hawkish press conference compared to recent ones, the Dollar can indeed potentially rise further. For example, if the Fed advises the FOMC will not vote for rate cuts in the first 2 quarters for the year.

When monitoring technical analysis, the price of the exchange is below trend lines, in the sell zone of oscillators and trading below the regression channels. All factors currently indicate Dollar dominance.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Dollar Rises As Fed Confirms No Rate Cut At March’s Meeting.

* The Federal Reserve Chairman advises journalists that interest rate cuts are not likely in March. However, bond yields continue to decline indicating institutions continue to believe cuts are impending.

* The USA100 declines by 2.5% over two consecutive days after earnings data was unable to support individual stocks.

* Futures market points lower in Europe and Asian stocks show no clear direction. Traders are considering if investors will take advantage of the lower price ahead of tonight’s vital earnings data.

* Stock traders turn their attention to earnings from Apple, Amazon and Meta. The three stocks make up almost 18% of the NASDAQ.

EURUSD – The US Dollar Rises Against All Currencies!

The EURUSD exchange saw one of the highest levels of volatility amongst the “major currency pair” category. The exchange rate saw two significant impulse waves which can be explained using fundamental factors. The first impulse wave was in favor of the Euro and was largely due to the German inflation data reading higher than expectations. The correction which followed in the US session was due to the Fed’s comments on future interest rates.

This morning the exchange rate trades 0.30% lower and continues to obtain sell signals against the Dollar. The US Dollar Index is trading at its highest level since early December 2023. The Euro on the other hand is not witnessing any significant price movements against other major competitors. The Euro upward price movement was generally weak against the Dollar as German inflation still fell despite the smaller decline and also French inflation fell by a considerable -0.2%.

The US Dollar saw some negative economic data for the first time in over two weeks in yesterday’s session. The ADP Non-Farm Employment Change read 41,000 lower than expectations and the Employment Cost Index for the quarter fell to its lowest level since July 2021. Nonetheless, the Federal Reserve confirmed in their press conference that a rate cut in March is not likely. According to analysts, the Fed will not likely cut at the March meeting unless employment data takes a serious hit. According to the CM Exchange, there is a 92% chance of a rate cut in May and a certain cut by June at the latest. The Fed did not give any indications that this is not possible and is being backed this morning by declining yields. The question is who will opt for larger and more frequent cuts, the Fed, the ECB or the Bank of England.

USA100 – Will Investors Continue Profit Taking?

The USA100 saw a considerable downward price movement on Wednesday and order flow analysis indicates seller overpowering buy orders. In addition to this, the assets traded below the volume weighted average price throughout the whole day. Technical analysis and order flow indicate a decline in the asset; however, traders also need to consider if investors will look to re-enter at a lower price.

This will largely depend on tonight’s earnings data. Analysts expect Apple, Amazon, and Meta to witness significantly higher earnings as well as revenue. However, the question is whether the companies will beat expectations. Investors will also be closely monitoring reviews on the new Apple headset. These reviews and future sales figures can significantly affect Apple stocks which hold 8.78% of the NASDAQ. So far, reviews are positive in terms of the technology and experience, but negative in terms of the price and demand due to the high cost.

GBPJPY – Investors Turn Their Attention to Bank of England Votes

The GBPJPY is decreasing in value for its fourth consecutive day and is trading at its lowest level since January 16th. Throughout the year the Japanese Yen is expected to perform well due to being the only Central Bank which will not be cutting interest rates. However, in the short-term, the price action will depend on this afternoon’s Bank of England Press conference and “Committee Votes”.

The rate decision is without a doubt not going to change this month, however, the change in votes can create volatility. Analysts expect 2 members of the committee to vote for another interest rate increase, which is lower than last month’s 3 votes. If the votes are more hawkish than expectations, the Pound can rise. Whereas less votes for rate increases or a vote for a decrease would significantly pressure the Pound.

Technical analysis signals a downward trend when evaluating momentum and trend-based indications. However, the price has fallen to the previous resistance level which can be flipped to a support.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The S&P500 Renews Its All-Time-Highs. Investors Turn to Upcoming US Data.

* Investors take advantage of the lower purchasing price amongst technology company stocks. The NASDAQ recovers and trades closer to previous highs.

* Apple, Amazon, and Meta earnings beat Wall Street’s expectations. Apple falls 2.92%, Amazon rises 7.11% and Meta trades more than 15% higher.

* Apple revenue rises for the first time in over 12-months. Nonetheless, investors still sold shares as the company confirmed they are encountering difficulty in China, one of their largest markets. China previously has accounted for up to 25% of Apple’s revenue.

* Analysts expect the US Unemployment Rate to rise from 3.7% to 3.8% and for the NFP Employment Change to read 188,000.

USA500 – Earnings Push the USA500 to All-Time Highs

The USA500 was the best performing index on Thursday increasing in value by 1.25% and rising to a new all-time high. Technical analysis currently continues to indicate upward price movement. The asset trades above moving averages, above the Volume Weighted Average Price and oscillators continue to indicate buyers are controlling the market. The only concern for investors is the previous resistance level and if demand will decline at such a high price.

The price this morning trades within a price range between $4,937.90 and $4,928.87. If the price breaks above this level the assets’ buy signals can potentially strengthen. The upward price movement is supported by company earnings data. Apple, Amazon and Meta easily beat earnings and revenue data. Apple was the only stock which saw a decline after earnings due to negative data from China, its second most important market. Meta and Amazon on the other hand saw a significant rise in demand.

The Unemployment Rate is expected to increase from 3.7% to 3.8% and the Average Hourly Earnings to decrease from 0.4% to 0.3%. The Nonfarm Payrolls may also decrease from 216,000 to 188,000. According to analysts, the ideal release would be slightly weaker figures but not weak enough to indicate harsher economic conditions. Though weaker data can prompt the Fed to consider a rate cut earlier. However, higher and stronger employment data can temporarily pressure the stock market as it supports rates remaining higher for longer.

Important earnings reports will continue today and on Monday for the USA500. This morning ExxonMobil and Chevron will announce their earnings. Over the past month, neither stock has seen any significant bullish price movement. On Monday, McDonald’s and Caterpillar will announce their earnings. Both stocks are trading slightly higher in 2024.

GBPUSD – Bank of England Member Votes for Rate Cut!

The price of the British Pound rose in value against the currency market as a whole and the US Dollar Index moderately fell. During yesterday’s session the Cable rose 0.46% and is also trading higher this morning. However, investors should be cautious of upward price movements as the Bank of England were deemed to be more dovish than their global partners.

The Bank of England has a Monetary Policy Committee made up of 9 members. None of the nine members have ever voted for a rate cut in the past 4 years, until now. Only 2 members of the committee voted for a hike, which is lower than previous months. 6 voted for a pause and 1 voted for a rate cut. Additionally, the Governor of the central bank also said the regulator would consider a rate cut later in the year.

Lastly, investors will have their attention fixed on this afternoon’s upcoming economic releases across the Atlantic. If the US employment data and Consumer Sentiment read stronger than expectations, the Dollar can potentially attempt a correction.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap – Dollar shines;Gold in free fall as US consistently defies recession fears.

Economic Indicators & Central Banks:

* An eyepopping January jobs report capped off a huge week of events that ended with fresh record highs on Wall Street – FOMC indicated it was done with tightening.

* Dollar up as any hopes for a March rate cut were wiped out. Meanwhile, further evidence of the robust economy added to the growing optimism for 2024 after 2023 ended on a high note.

* The China Securities Regulatory Commission has announced its commitment to intensifying the enforcement of measures targeting offenses like market manipulation and malicious short selling. Simultaneously, it aims to direct a greater influx of medium and long-term funds into the market.

* Market sentiment was also negatively impacted by remarks from former President Donald Trump, who suggested the possibility of imposing tariffs exceeding 60% on imports of Chinese goods if he were to be re-elected.

* German trade surplus widened, but exports plunged – Germany’s export oriented model is struggling with geopolitical tensions.

Market Trends:

* Treasuries fell, extending Friday’s selloff.

* Massive earnings beats from Meta (20%) and Amazon (+7.87%) saw the US major Indices surging by more than 1%, while Nvidia closed 4.74% higher.

* Asian stocks were mostly lower as Chinese shares extended declines despite a series of stimulus measures and the securities regulator’s latest pledge to shore up the market. – the FED, China’s property sector & tepid investor sentiment are all pressuring the Chinese equity market.

* European futures are also narrowly mixed, while US futures are posting broad losses.

* Today: January PMI data for France, Germany, UK & Eurozone and US ISM Services.

Financial Markets Performance:

* The USDIndex held gains, just a breath below 104, while EURUSD drifted below 1.0800. GBPUSD held in December’s range.

* The Yen crept lower to trade above $148.

* USOIL steadies above $72 as the US vowed more strikes against Iran’s forces while the Houthis promised to retaliate against bombardments over the weekend.

* Gold weakened!

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap – Stocks surge as hopes of rate cuts recede; USD, yields higher.

Economic Indicators & Central Banks:

* Treasury yields elevated and US government bonds remained in a selloff after Fed Chair Powell pointed to fewer interest rate cuts this year than markets had been projecting.

* Strong ISM services index added to the selloff for Treasuries, as did the concession building ahead of this week’s $121 bln Treasuries auction.

* RBA left its cash rate unchanged at 4.35% – 12-year high. Surprisingly the statement indicated that “a further increase in interest rates cannot be ruled out,” hence leaving a hawkish bias in place. – possibly this is more prudence and a cautious move in order to keep rate cut expectations from building. Forecasts show inflation will not be coming into the 2% to 3% target range until 2025, hence the hawkish slant, and will not hit the midpoint until 2026.

* BOE’s Huw Pill said that he did not need to see underlying inflation actually hit the 2% target to begin lowering rates.

* UK retail sales slowed in January.

* An unexpected jump in German manufacturing orders at the start of the European session reduced the pressure on the ECB to cut rates. German manufacturing orders unexpectedly jumped 8.9% y/y. This was the strongest bounce since June 2020 – glimmers of hope but overall demand subdued!

Market Trends:

* Chinese stocks rose after the announcement that China’s securities regulator will meet President Xi Jinping.

* Equities declined in Japan, Australia and South Korea. Topix fell 0.8% in the early trade ahead of earnings releases from Toyota Motor and Mitsubishi Corporation. JPN225 (Nikkei) fell 0.5%.

* US and European futures contracts showed modest gains this morning, extending the positive lead in Asia.

* UBS Group AG said it will resume share buybacks this year, vowing to hand as much as $1 billion to shareholders in the second half.

Financial Markets Performance:

* The USDIndex rallied on the less dovish Fed outlook, rising to test 104.60 before dipping back to 104.15 today.

* The AUDUSD rallied to 0.6520 as Aussie bond yields jumped with the benchmark rising over 7 bps to 4.166.

* USOIL recovered modestly from its better than -7% plunge last week, rising to $73.28 per barrel before drifting down to $72.98.

* Gold fell to an overnight nadir of $2014.95 per ounce thanks in part to the rise in bond yields, but inched up to finish at $2026.30, the weakest since January 26.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

* Treasuries bounced back after the worst 2-day stretch since June 2022. Dip buying supported along with a solid 3-year note auction & comments from the more hawkish Fed President Mester who could see rate cuts later in the year.

* China’s bourses initially rallied on stimulus hopes, but the pledge to do more and the attempt to fix the situation with a series of smaller changes hasn’t instilled lasting confidence. Stimulus hopes are priced in already and gains could fade, if there is no more decisive follow up.

* This year’s near -9% plunge in the Shanghai Composite index to the lowest since 2019, and the better than –10% drop in the Hang Seng, have rattled the officials significantly, especially as the various measures to date, including curbs on short selling, along with rate cuts and liquidity injections by the PBoC have failed to provide much umph.

* German industrial production corrected -1.6% m/m in December. A worse than expected result.

Market Trends:

* The CSI 300 is still up 0.96%, but the Hang Seng is now down -0.2% on the day.

* The Dow advanced 0.37%, with the S&P 500 0.23% higher, and the NASDAQ up 0.07%.

* European and US futures are flat!

Financial Markets Performance:

* The USDIndex was firmer but off its best levels as the gain to a 104.604 intraday high elicited some profit taking as the markets weigh central bank policies.

* The NZDUSD spiked to 0.6113, as government bond yields rose after the strong New Zealand jobs report, which indicated that the RBNZ could remain cautious about cutting interest rates. The Aussie Dollar strengthened as well.

* USOIL prices are firmer at $73.42 per barrel. Gold is 0.53% higher at $2035.66 per ounce.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap – S&P500 Breaks 5k; Gold & USD in a range!

Economic Indicators & Central Banks:

* Asian stock markets were mixed with mainland Chinese stocks swinging between gains and losses on the eve of the Lunar New Year holidays, while Treasuries stabilized.

* China CPI tumbled to an -0.8% y/y pace in January, steeper than forecast, after falling at a -0.3% y/y clip in December. It is the fastest pace of decline since September 2009 and a fourth straight month in deflation.

* Japanese bourses outperformed,after BoJ’s Uchida said it is hard to see a rapid lift-off in rates.

* Treasuries bounced back after the worst 2-day stretch since June 2022.

* Dovish Fed’s Kashkari currently sees two to three rate cuts would be appropriate this year, as things stand.

Market Trends:

* The Nikkei rallied 2.1%, mainland China bourses and the Hang Seng corrected again.

* European and US futures are higher despite a slight rise in yields.

* The S&P 500 hit a new high at the close, breaking the 5,000 level , driven by confidence in the economy despite worries like Fed policy changes and market conditions. The market remains strong with good momentum, even in a slower season.

* Ford Motor, Chipotle Mexican Grill and other big stocks climbed following their latest earnings reports.

Financial Markets Performance:

* The USDIndex is at 104.03, in a tight range as markets digest mixed Fed speeches and ahead of more economic data.

* The USDJPY depreciated against the US Dollar, reaching 148.80, following comments from BoJ Deputy Governor Shinichi Uchida indicating that the central bank is unlikely to pursue aggressive interest rate hikes, even as it moves away from negative interest rates.

* USOIL rose for the 3rd day in a row, above $74, driven by gains in financial markets and ongoing tensions in the Middle East. The rise in global stocks is boosting demand for oil, despite the Federal Reserve’s dismissal of immediate interest rate cuts.

* Gold steady at $2030-2038.

* Bitcoin rose 0.85% to $44,564.62.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap – Yen, Oil & Bitcoin Hit Key Resistance Levels Ahead of US Inflation Week.

Economic Indicators & Central Banks:

* Markets are closed for the holiday in mainland China, Taiwan, South Korea, Indonesia, the Philippines and Vietnam.

* Treasuries declined for a 2nd straight session & Wall Street closed with small gains, as the market continues to shed expectations on Fed rate cuts ahead. The catalyst for selloff was the declines in initial and continuing jobless claims, reversing some of the recent increases and indicating the job market remain solid.

* Nikkei (JPN225) saw an uptick at Friday’s close, pulling back from a 34-year peak as investors are in a profit taking mode in this 3rd week of gains. It edged up by 0.09% to 36,897.42 after surging as high as 1.15% to 37,282.26, marking its highest level since February 1990.

* German HICP inflation was confirmed at 3.1% y/y in the final reading for January. Inflation is still far above the ECB’s target, but on a clear downtrend, and for the doves at the ECB that is enough to start weighing rate cuts.

Market Trends:

* European futures declined cautiously ahead of US inflation data, while Asia geared down for the Lunar New Year holiday.

* Australian equities remained relatively stable, while Japanese stocks displayed mixed performance, partially supported by a weaker yen.

* The Nikkei rallied 2.1%, mainland China bourses and the Hang Seng corrected again.

* SoftBank Group surged by 8.72%, extending its upward trajectory for a 2nd day following the tech investment firm’s return to profitability after 5 quarters. The rally in SoftBank Group Corp. shares was propelled by a more-than-55% surge in Arm Holdings (Arm chip design unit), in which SoftBank holds a 90% stake, after the British tech company forecasted quarterly sales and profit surpassing Wall Street expectations.

* Nissan plummeted by 12% after the company failed to meet profit estimates.

Financial Markets Performance:

* The USDIndex remained steady ahead of the annual revisions to monthly US inflation data, following last year’s revisions that raised doubts about the Federal Reserve’s progress in managing consumer prices.

* The Yen stabilized after a 0.8% decline against the USD on Thursday, triggered by comments from a BoJ deputy governor hinting at the central bank’s continued accommodative policy stance. The USDJPY broke 149 and extended to 149.49.

* NZDUSD climbed to 0.6133 along with New Zealand yields following ANZ Bank New Zealand Ltd.’s forecast of 2 more interest rate hikes by the RBNZ this year.

* USOIL broke $76, eyes on $80 resistance level.

* Bitcoin spiked to 1-month high above $46,000, with historical data indicating positive returns post-Lunar New Year holidays, averaging over 10% in 10-day returns since 2014.

* Ether, Solana and Cardano also pushed upward.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Inflation Expectations Were Too Optimistic. Investors Consider More Buys.

Economic Indicators & Central Banks:

* UK inflation unexpectedly remains at 4.0% and Core Inflation data also read lower than expectations causing the Pound to decline.

* US inflation declines but at a weaker pace compared to expectations. US inflation falls from 3.4% to 3.1% (previously expectations were for inflation to fall to 2.9%).

* The best performing currency as we edge towards the European Cash Open is the Australian Dollar, followed by the Japanese Yen.

* The NASDAQ witnesses its largest daily decline in February due to the inflation rate pushing back hopes of an early rate cut.

USA100 – Core Inflation a Concern for the Fed and Investors!

After the release of January’s inflation rate and core inflation data, the USA100 as well as all US indices fell rapidly. When evaluating each component within the NASDAQ, only 6% of the index were able to hold onto their value. All stocks which held more than a 0.50% weight in the index depreciated. The reason for the decline was not that the inflation rate is “too high” or that interest rates cuts are not likely. Instead, the decline is due to investors now believing a cut in March is indeed not possible.

According to analysts, the inflation rate does not indicate any danger to the US economy, nor does it indicate there is any reason for a large lasting decline in US stocks. However, the news can weaken demand in the short term. Again, economists advised the inflation rate is not high, but simply higher than the over-optimistic expectations, and that cuts are still likely in the second quarter of 2024.

The short-term price condition of the index will largely depend on upcoming earnings reports from Cisco and Applied Materials. The two stocks make up 2.70% of the index and if these earnings read higher than expectations, it can reassure investors amid concerns. Cisco has beat earnings per share expectations consecutively over the past 12 months as has Applied Materials.

Investors’ main concern yesterday was the Core Inflation data which continues to prove difficult to tackle. Core inflation does not include products related to food and the energy sector. The monthly Core Inflation Data read 0.4%, the highest since May 2023. But slightly easing concerns is inflation elsewhere falling; the UK inflation remains at 4.0%, Chinese inflation fell as did Swiss inflation. The Producer Price Index will now be vital for investors. If the PPI reads higher than expectations, investors’ concerns could grow and the USA100 could form a correction instead of a smaller retracement.

On the daily chart, a retracement would mean a further decline between 1.89% to 4.40%, whereas a full correction would mean a 6.30%-8.00% decline. Currently the two-hour chart indicates an upward price movement towards the 75-bar exponential moving average. However, investors should note this will largely depend on earnings data, the US Retail Sales and Friday’s PPI release.

GBPUSD – The Pound Gives up Gains after Lower Inflation Data

The exchange rate continues to trade below major trendlines for a second day after stronger US inflation and weaker UK inflation. The possibility of the Bank of England opting for a rate cut first, or within the same month as the Federal Reserve grows. However, this will depend on upcoming data from the UK over the next 48-Hours.

The UK is scheduled to release their Monthly GDP and Retail Sales on Friday. If both read lower than expectations, the possibility of an earlier rate cut by the Bank of England rises. The UK’s Gross Domestic Product is believed to have declined by 0.2%, which would be the third decline in 6-months.

Technical analysis also indicates a downward trend. The price of the exchange trades below the 75-bar EMA and below the neutral on the RSI. On the 5 and 15-minute timeframes, the asset is also forming downward crossovers. These three factors indicate further bearish price movement and the Fibonacci indicates the price can fall down to 1.24990.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Investors Continue to Buy Ahead of the US Producer Inflation Release!

* UK Retail Sales witnesses its strongest increase since May 2021, but economists advise the increase is simply correcting poor data from previous months.

* The Pound gains against most currencies, but the currency market has their eyes fixed on the upcoming US Producer Price Index.

* Applied Materials soars above earnings expectations. Earnings Per Share beat expectations by almost 12% and revenue by 3%. The stock rose 12% after market close.

* Bitcoin again renews its recent highs rising another 2.15% on Thursday. Cryptocurrencies are also likely to witness strong influence this afternoon.

GBPUSD – UK Retail Sales Beat Expectations

The GBPUSD was trading lower throughout the trading session but quickly rose to the day’s open price after the UK’s Retail Sales Release. The Retail Sales read 3.4%, significantly higher than 1.5% which was expected and -3.2% from the previous month. However, economists are advising a strong increase is not as positive as it may seem considering previous months saw a decline of 3.9%. Nonetheless, investors are reacting positively, and the GBP is rising moderately against all currencies.

In terms of technical analysis, the exchange rate is seeing neither bullish nor bearish signals. The price is trading at most trend lines and is neutral on most oscillators. In order for traders to obtain a clear signal, the exchange rate must maintain momentum and show a clear direction. If the price breaks above 1.26056, which is also the resistance level of the day before, buy signals will materialize. If the afternoon’s Producer Price Release is lower than expectations, a bullish breakout is likely to take place.

The US will release the Producer Price Index, Core PPI and the Prelim Consumer Sentiment. The strongest price driver will be the PPI and Core PPI release. Analysts expect both to read 0.1%, which is only slightly higher than the previous month. However, the question is if the rate of increase will be higher than expectations. Another higher inflation reading will again support the Dollar, but pressure Gold and US Stocks.

USA100 – Investors Await PPI Release and Attempt a Full Correction!

The USA100 saw a slight decline as we were approaching the US open due to weak Retail Sales, but again investors only used this to enter at a better entry level. The index ended the day 0.22% higher and is 0.85% lower than the previous high. Technical analysis currently points towards a full correction back up to $18,058, but this will largely depend on the Producer Price Index.

If the PPI reading is higher than 0.1%, the USA100 and the stocks market in general can witness another decline. The decline may simply be a retracement or a full correction back to 1.25341, but this would depend on how much higher the reading is. If the PPI and Core PPI reads 0.1% or lower, the bullish trend potentially can continue as per indications from Crossovers, VWAP, and Oscillators.

The index was supported by Applied Materials which released their quarterly earnings report. The company’s Earnings Per Share beat expectations by almost 12% and revenue by 3%. The stock rose more than 12% after the market close and can support the index if it continues to perform well in the upcoming days. The next major earnings report will be NVIDIA next Wednesday after market close.

Bitcoin – Net Inflows of Over $1 Billion this Past Week

The cryptocurrency market capitalization rose this week, but slightly fell this morning ahead of the PPI release. However, the general rise is positive for Bitcoin as is its higher market share which rose 0.29%. Investors should note the day’s inflation reading is likely to also affect Bitcoin in a similar way to the stock market.

The cryptocurrency market is being supported by the weaker monetary policy in China, one of its largest markets. However, the price action will depend on continued relaxation from across the globe. Another reason is demand for spot-Bitcoin ETFs which remains strong, with net inflows of over $1 billion over the past week. Technical analysts also note the importance of surpassing the $50,000 mark which is a strong psychological price/level.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

* Chinese stocks climbed slightly as China returned from the long New Year holidays. Modest gains showed that investors are worried about the longterm outlook. Much of the economy’s sluggishness is a function of the collapse in the property sector as well as the bearish effects of the many regulatory restrictions in tech, problems that would not be helped much by easier policy.

* US markets are closed for the Presidents’ Day holiday.

* This week: Eyes on European inflation data, PMI data from EU, UK and US, RBA & FOMC Minutes, as well as earnings from Nvidia Corp. and BHP Group Ltd to help gauge the health of the global economy.

Market Trends:

* Nikkei (JPN225) holds near 1989 highs, pressured by Friday’s selloff but also due to decline in chip-related shares. Nintendo was the biggest percentage decliner though, slumping 5.8%. Chip-sector heavyweights Advantest and Tokyo Electron were the Nikkei’s biggest drags, shaving off 60 and 55 index points respectively with declines of 3.2% and 1.6%.

* European stock futures are in the red, US futures fractionally higher on what is likely to be a quiet day, as US markets are closed.

* S&P500(USA500) rose 0.1%, Nasdaq (USA100) rose 0.2%.

Financial Markets Performance:

* The USDIndex’s gains faded after the hot inflation stats crushed expectations for quick and deep Fed rate cuts. Currently at 104.

* The Yen is directionless, with USDJPY sideways close to 150 with volumes likely to be low through the day. The drag from higher US bond yields, particularly on tech stocks, is offsetting support from a weak yen.

* USOIL pulled back from $78 highs on the ongoing Middle East tension. The IEA signaled last week that oil markets could be oversupplied all year, and China’s soft economy has raised questions about consumption. Still, attacks on shipping in the Red Sea and the Israel-Hamas war are keeping prices from falling too far.

* Gold extends Friday’s gains, above $2020.

* Bitcoin at $52514.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap – US & European equities declined, mirroring the drop in Asian stocks.

Economic Indicators & Central Banks:

* Futures for both US and European equities declined, mirroring the drop in Asian stocks, as an adjustment to China’s mortgage reference rate did little to alleviate worries surrounding the world’s 2nd largest economy.

* China implemented a record rate cut, reducing the 5-year loan prime rate by 25 basis points to 3.95%, surpassing economists’ expectations of 5 to 15 bp cuts.

* The RBA maintained its cautious stance, further suggesting that rate cuts were not imminent. Minutes from the central bank’s February meeting, released today, indicated that policymakers require additional time to ascertain if inflation is indeed decreasing before considering any potential interest rate hikes.

* Market sentiment outside China weakened as expectations for US rate cuts dwindled following higher-than-expected producer and consumer prices.

* Today: The Canadian inflation and European wages data, which are expected to influence market movements going forward.

Market Trends:

* Nikkei (JPN225) retreated by 0.3% from its recent highs.

* US Treasury yields edged up slightly, with S&P500 (USA500) futures and European futures both declining by 0.3%.

* BHP Group, the world’s largest miner, reported $6.57 billion in underlying profits, less than consensus estimates, and stated demand from top customer China was healthy despite weakness in housing.

Financial Markets Performance:

* The USDIndex strengthened broadly surpassing 150 Yen, amid expectations of sustained higher US interest rates, despite Japan’s recession and uncertainty over its monetary policy exit.

* The Aussie, often viewed as a proxy for China’s economic health, remained largely unchanged, while iron ore futures, linked to Chinese construction demand, declined by 3%.

* The Yuan initially dropped to its lowest level in 3 months but stabilized at 7.1981 in the Asia close.

* Gold was little changed after edging higher Monday to trade around $2,020 per ounce.

* The USOIL edged higher against the backdrop of ongoing tensions in the Red Sea, a vital trade route. It is retesting again the January’s high again.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

AUDUSD – Economists Do Not Expect the RBA to Cut Until 2024’s Third Quarter.

* The Aussie Dollar increases 0.67% and sees its strongest gain this week so far. The exchange rate trades at its highest price since February 2nd.

* The FOMC’s Meeting Minutes indicate the Federal Reserve is not yet willing to cut interest rates. FOMC Members are cautious about cutting rates too fast.

* Australia’s Wage Price Index for the latest quarter continues to read higher than where the RBA would like to see it.

* The Reserve Bank of Australia advise the regulator would not consider cutting interest rates until the second half of 2024.

* The Australian Economy weakens but not enough to pressure the RBA! Inflation remains moderately higher than the US!

AUDUSD – Technical Analysis

The AUDUSD is witnessing one of the lowest spreads amongst the major currency pairs and is seeing higher levels of volatility. The Australian Dollar has been rising against the USD for seven consecutive days, similar to the NZD and the Euro. However, the AUD is performing better than the GBP, JPY and CHF against the Dollar. However, investors should note that the bullish price movement is largely being driven by the weakness in the Dollar.

The US Dollar Index has fallen 0.50% this week and trades at a 3-week low. The Australian Dollar on the other hand is witnessing mainly bullish price movements depending on the currency pair. The Australian Dollar is increasing against the GBP, Euro, Yen, and the CHF but is declining against the NZD. So here we can see there are no major conflicts between the two individual currencies. However, investors will need to continue monitoring the US Dollar Index and price condition of the AUD against other major currencies.

The AUDUSD is trading above the 75-Bar Exponential Moving Average and above the “Neutral” level on the RSI as well as the Bollinger Bands. These three factors indicate a further bullish trend as the asset is yet to be read “overbought” on most oscillators. In addition to this, the asset has managed to break above the resistance level and the previous high, meaning the continuation of the traditional wave pattern.

The only negative indication when evaluating technical analysis is the measurements of the previous 4 impulse waves. The average bullish wave size is 0.87% and the largest has been 0.92%. The current impulse wave reads 0.87%. Therefore, if the pattern is to continue the price may retrace soon, even if it is going to continue rising thereafter. However, this cannot be known for sure.

AUDUSD – Fundamental Analysis

In the Meeting Minutes, representatives stated more fear about the remaining risks of a premature decline in rates than about a persistent period of high interest rates. Against this background, markets are reconsidering the timing of a possible easing of the regulator’s position in May and June. According to the CME Groups FedWatch Tool, the likelihood of a May adjustment is currently anticipated at 30-35%. A strong possibility is considered anything above 70%.

Next week’s Core PCE Price Index will be key for the Dollar as this will be the last inflation reading for the month and short-term future. If the PCE Price Index is also higher, this means all 5 inflation readings beat expectations. As a result, the Dollar may rise. However, the Dollar’s issue is that the market’s risk profile is high, and many expect the Fed to cut first. Therefore, the Dollar may continue to struggle unless other central banks become more dovish.

Even though the Reserve Bank of Australia’s interest rate is lower than the Fed’s, analysts expect the Fed to cut first. Even though GDP Growth in Australia is weakening, the economy is still performing better than Europe and the UK. In addition to this, inflation is still above 4.00%, which is extremely high for the Aussie and the Unemployment Rate has risen to 4.1% which is still manageable according to analysts there. Therefore, most analysts believe the RBA will cut in the third quarter and after the Fed. Therefore, fundamental analysis is slightly in the Aussie’s favor here, but technical analysis will need to continue signalling a rise.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap – Global Rally Pushing Valuations To Record Highs Across the US, Europe & Japan.

Economic Indicators & Central Banks:

* It was all about Nvidia. Nvidia got a $277 billion 1-day boost to its market capitalization yesterday – the biggest single-session increase in value ever!(the previous record was a $197 billion gain by Meta Platforms Inc.)

* Treasuries continued to lose ground, hurt by the surge in risk appetite with yields cheapening to the highest levels since late last year.

* The solid jobless claims report, which followed on the heels of the hawkish bent in the FOMC minutes, added to expectations the FOMC will leave rates in restrictive territory into June at least.

* A weaker than expected S&P Global services headline saw rates dip briefly.

* Japanese markets are closed for a public holiday.

* Fed Governor Christopher Waller: ”interest rate cuts should be delayed at least two more months, but indications of healthy demand and concerns over supplies could boost prices in the coming days.”

* Today: Germany IFO business climate & GDP, ECB publishes 1- and 3-Year inflation expectations survey.

Market Trends:

* Massive global rally in risk that saw the NASDAQ(USA100) jump 2.96% to 16,041.6, falling just short of the historic peak of 16,057 from November 2021. The S&P500 (USA500) climbed 2.1% to 5100, and the Dow (USA30) was up 1.18% to 39,069, both marking new records.

* Asian stock markets today continued to move higher, with the global rally pushing valuations to record highs across the US, Europe and Japan. The Nikkei jumped a further 2.2%.

Financial Markets Performance:

* The USDIndex was little changed at 103.80, below 104 for the first time since February 2.

* The Yen has performed the worst so far this year, experiencing a 6.3% decrease against the Dollar, as investors sought higher yields in other currencies, anticipating that Japan’s interest rates would remain close to zero for the foreseeable future.

* The Yen weakened against the Euro, Sterling, and other currencies this week, marking its 4th consecutive weekly decline against the US Dollar.

* USOil slipped to $77.85 per barrel after Fed speeches indicated delay to rate cuts.

* Gold dipped to $2021 per ounce.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!