Market Update – October 27 – Investors poised for weekly profits.

Trading Leveraged Products is risky

Stock market sentiment improved, and Asian equities bounced, alongside gains in European and US futures. Earnings reports helped tech stocks to stabilise, ahead of more key US data. The 10-year Treasury yield is up 3.2 bp at 4.88%, after strong GDP numbers yesterday. Eurozone bonds meanwhile continued to find buyers, after the ECB effectively confirmed yesterday that in the central scenario rates have peaked. The schedule for the re-investment of PEPP redemptions was also left untouched, which helped peripherals to outperform and spreads to come in. US economy expanded at its quickest pace in almost 2 years in the latest sign of the country’s economic resilience.

*Stock markets: Wall Street close in red for a 2nd session. The US100 has cratered -2.05%. The US500 has dropped -1.28% and is -3.2% lower, with the US30 down -0.77% today and -1.9%. Over the past 5 sessions the indexes are posting declines of -4.75%, -3.2%, and -1.9%, respectively. Today, stock sentiment improved.

*Asian shares rose after strong Q3 sales at Amazon helped drive a recovery in investor sentiment following weak results from other technology groups earlier in the week.

*Amazon (+5.36% after hours) sees best profits since 2021.

*Meta (+0.95% after hours) ad revenue (+23%) fuels blowout Q3, $11.6 billion in profits.

*Elon Musk just lost $28 billion as Tesla (+1.25% after hours) took a beating.

*USDIndex has lost altitude slightly to 106.36 after climbing to 106.894, just shy of the 107.000 level from October 3 that was the highest since late 2022.

*USDJPY is holding the 150.00 level, continuing to test the MoF after finance minister Suzuki warned that authorities were closely watching currency moves “with a sense of urgency.”

*EURUSD lost ground on the ECB’s stance, trading at 1.0544, though inside the day’s 1.0574 to 1.0524 range.

*USDCAD remains above at 1.3810 after the BoC’s announcement .

*GOLD flat but close to 1998 (more than 2-months highs).

*USOIL recovered to $85 after a fall due to a rise in US crude stockpiles and a climb in the US Dollar.

Today: US PCE deflator, personal consumption, University of Michigan sentiment (October), Exxon, Chevron earnings.

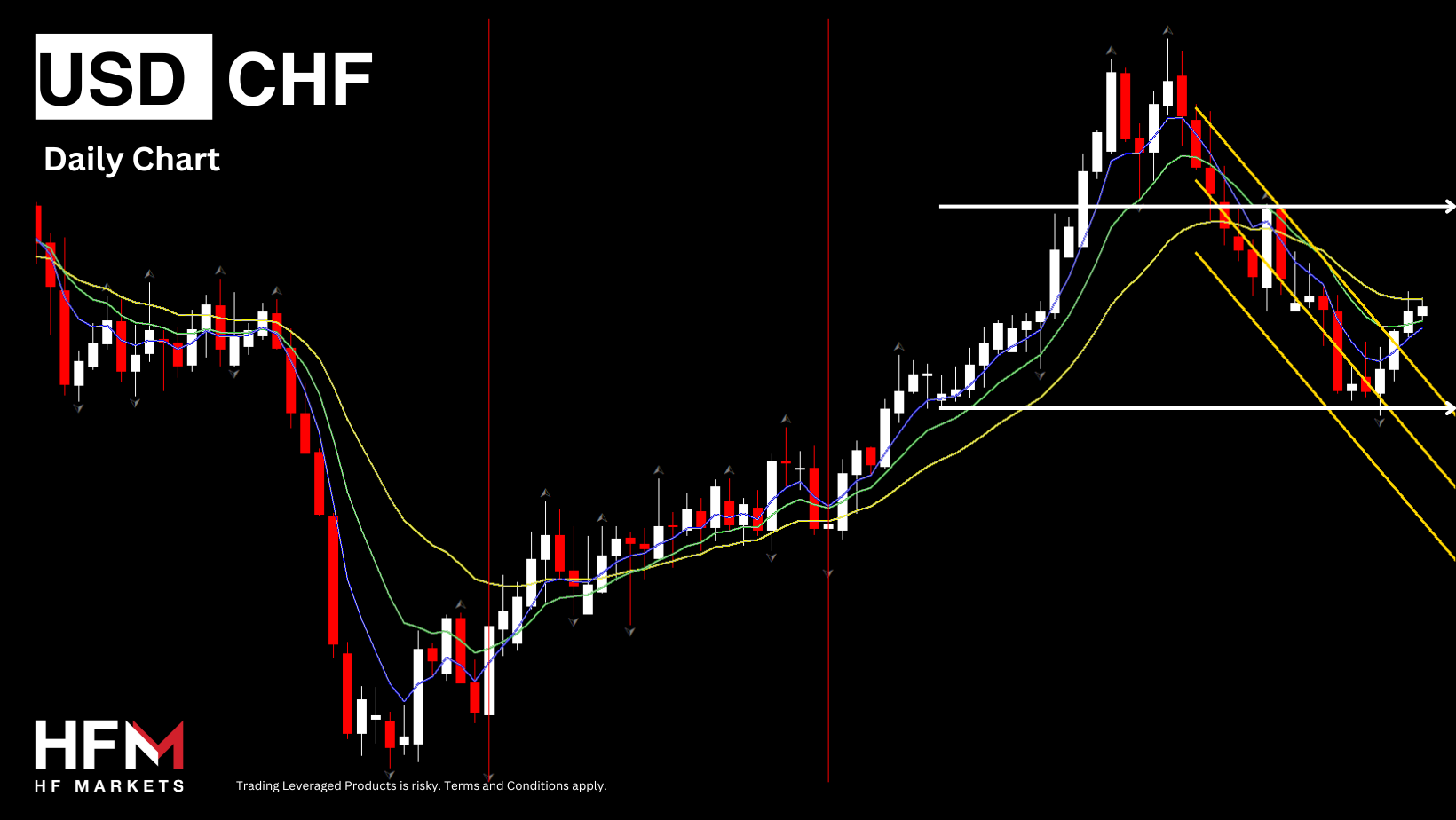

Interesting Mover: USDCHF broke descending channel and extends higher for a 4th day in a row.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Stock markets struggled overnight. Mainland China bourses found buyers, but JPN225 and ASX declined, as markets watched developments in the Middle East. Risk sentiment improved during the start of the week as Israel seemed to be moving with more caution than anticipated, which helped to dampen concern about a widening of the conflict. Stock futures are higher across Europe and the US and the 10-year treasury yield has lifted 2.6 bp to 4.86%, with oil and gold also declining as haven flows ease. Treasuries were boosted also after the slowing in the PCE deflators underpinned expectations the FOMC is on hold. Short covering and a flight to safety extended the more bullish tone as Israel began its ground assault on Gaza.

*Stock markets slightly higher today after Wall Street saw the US30 drop -1.12% with a hefty -6.7% plunge in the energy complex. The US500 declined another -0.48%, with the latter now in correction territory, -10.3% below the July 31 peak. The US100 bounced 0.38%. For the 5 days, the US30, US500, and US100 are down -2.14%, -2.53%, and -2.62%, respectively.

*Morgan Stanley’s Wilson: ‘‘Chances of a fourth-quarter rally have fallen considerably”,“Narrowing breadth, cautious factor leadership, falling earnings revisions and fading consumer and business confidence tell a different story than the consensus, which sees a rally into year-end.”

*Amazon’s pop by 6.8% and Intel’s jump by 9.3% helped soften the blows from big drops in Alphabet, Meta, and Tesla. Ford stumbled 12.2%.

*JGB yields climbed to fresh 10-year peaks today & USDJPY corrected to 149.22, as investors weighed the chances of a possible policy tweak in the BOJ’s monetary policy decision tomorrow. BOJ is widely expected to keep its short-term rate target at -0.1% and that target for long-term rates around 0% as set under its YCC policy.

*USDIndex is at 106.50, down on Friday’s close, but within the previous day’s range.

*GOLD spiked to $2006.40 on the escalation of the war. Currently settled lower at $1990. It’s likely to continue benefiting should tensions increase, alongside the Swiss franc and short-dated US government bonds.

*USOIL lower at $83.70.

Today: Central bank meetings: FED, BOE and BOJ. Earnings: Apple, Airbnb, McDonald’s, Moderna and Eli Lilly & Co among the many reporting this week.

Interesting Mover: USDCHF broke descending channel and extends higher for a 4th day in a row.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 31 – Stocks Down & Yen plummets.

Trading Leveraged Products is risky

Asian stock markets traded mixed, with China bourses underperforming after weaker than expected PMI reports that signal ongoing weakness, especially in the manufacturing sector. Treasuries meanwhile found buyers and the US 10-year rate is down -5.7 bp at 4.84%, while the 10-year Bund yield has dropped -3.3 bp to 2.79%. Stock futures are higher across Europe, but down in the US.

*China October PMIs missed expectations as factory orders contracts – CSI300 at -0.31%.

*USDJPY jumped to 150.24, after the Yen fell to 2-month lows as the BOJ made only minor changes to its policy settings, disappointing some in the market who had expected more. The central bank is keeping its cap on long-term yields at 1%, leaving its negative interest rate untouched and adding flexibility to its yield curve control.

*Financial stocks were the biggest winners, insurance and banking indexes rallying more than 2% each to lead gains among the 33 industry sectors. Higher long-term yields and a steeper yield curve improve the outlook for returns from lending and investing.

*Earnings beats from McDonald’s and SoFi provided support ahead of Apple and other key earnings this week.

*USDIndex dipped to 105.85 from a peak of 106.704 after the Nikkei report. Currently settled at 106.10.

**Antipodeans, which are often used as a liquid proxy for the Yuan, were further pressured by Chinese data, i.e. AUDUSD dipped initially to 0.6340.

*GOLD & USOIL: Unwinding of some of Friday’s haven demand saw gold fall about -0.5% to $1990 per oz, with a USOIL slide to $81.50 (Trendline & 200-DMA).

Today: Canadian GDP, EU preliminary GDP and CPI and NZ labor data- Earnings: AMC, BP and Pfizer.

Interesting Mover: EURJPY (+1.05%) returns 5-day losses and keeps rising with attention turning to 162-162.40 (1998 highs & 2007-2008 highs).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – November 06 – The aftermaths of cooler jobs continue.

Trading Leveraged Products is risky

Last week’s market reactions underscore the risks associated with central banks discussing data dependence without clarifying their medium-term framework or how they expect policy to impact the real economy.

Both stocks and bonds experienced rallies, boosted by the Treasury’s smaller-than-anticipated increase in longer-term debt auctions. However, Treasury yields dove with an eye-popping speed. The move underpinned a massive rally. The spectacular drop in rates last week saw the 2- and 10-year maturities recover a lot of their losses in October. The catalysts for the reversal were the FOMC’s less than hawkish stance, the cooler jobs report, and the moderation in Treasury supply increases. Geopolitical risks added a haven bid too.

*FT reported: The markets are wrong to assume an economic slowdown and the peak of interest rates. “Higher for longer” for interest rates was always more of a media catchphrase than policy analysis. However, the Powell Federal Reserve may not start to reverse policy errors with rate cuts before the middle of next year, and reacting forcefully to every single data release between now and then is going to be exhausting.

*USDIndex tanked, however, falling to a low of 104.84 from the early high of 106.95.

*USDJPY at 149.50. BOJ Ueda indicated that policymakers might not have sufficient data by year-end to end negative interest rates, as they continue to monitor the possibility of a wage-inflation cycle.

*Stocks: Wall Street exploded higher on the drop in rates. For the week, the US100 was up 6.6%, with the US500 having its best week since November 2022. The US30 posted a 5.85%, gain, its best week since October 2022. The VIX was off -4.8% to 14.91. Asian equities rose today after weaker than expected US jobs data released last week eased concerns over rising interest rates.

*Ryanair sees record annual profit, first regular dividend as fares soar

*Shares in Chinese brokerages jumped after state media reported that the country’s securities regulator would support buyouts and mergers in the financial sector to help create investment banks.

*Gold and Oil were scuttled too. Gold fell to $ 1992.5 per oz, down from $2004.10, but was as soft as $1983.31. USOIL dropped to $80.10 per barrel, but finished with a -1.95% loss at $80.85 after trading as high as $83.6 overnight. Currently settled at $80.85.

Today: EU, France, Germany, Japan: S&P Global October services PMI, UK October construction PMI. Earnings: BioNTech Q3, Itochu H1, Ryanair H1.

Interesting Mover: ETHUSD (+3%) jumped this morning breaking 2-week range and extending to $1910 area.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

It was another mixed day in the markets as players awaited fresh directional signals, including comments from Chair Powell later today. However, a new narrative is starting to build, one of slowing growth, with a recessionary tilt in Europe. The ongoing chant from the FOMC and ECB and BoE officials that more tightening might be necessary is adding to the angst over economic growth, alongside an effort to push back against speculation of early rate cuts, although it is increasingly clear that in the central scenario rates have peaked.

Concurrently, investors have been encouraged by this week’s auctions, that they have found buyers. And demand for higher yields have helped underscore a curve flattening trade with longer dated Treasuries outperforming. Falling Treasury yields helped launch an explosive rebound in stocks and lifted US government bonds from 16-year lows!

*Asian stock markets lower on mixed signals of peak US rates and weak Chinese economy.

*China slipped back into consumer price index deflation in October, as data released showed persistently weak demand in the economy. The inflation data is likely to reinforce the weaker-than-expected PMI figures last week.

*10-year Treasury yield falls below 4.5%.

*USDIndex holds gains above 105. EURUSD under pressure as Eurozone retail sales declined.

*Stocks: The US100 and US500 benefited further from the drop in yields. The US100 posted a marginal 0.08% gain, with the US500 up 0.10%. But those were sufficient to give the US100 a 9th straight winning session, and an 8th straight for the S&P. The Dow dipped -0.12%.

*SoftBank adds to shareholder pain with unexpected $6bn loss.

*UK chip designer Arm’s shares fall after disappointing revenue forecast.

*Disney tops profit estimates.

*AstraZeneca raises yearly guidance amid strong sales of oncology treatments.

*Oil slipped to $74.88, but is currently in correction mode. Further pressure was added after the EIA issued the new outlook after Saudi Arabia and Russia extended voluntary production cuts of 1.3 million barrels per day through December as demand concerns weigh. US total petroleum consumption is now expected to fall by 300,000 bpd to 20.1 million bpd this year, compared with an estimated gain of 100,000 bpd in the October forecast.

*Gold at $1949.

*Bitcoin trades past $36,500 on possible ETF investment approval.

*Today: BOE chief economist Huw Pill, Fed Chair Jerome Powell & Fed President Raphael Bostic and Richmond speeches & US initial jobless claims.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

It’s the day before a possible Government shutdown again, and a pretty pivotal week ahead for company reports and a round of significant inflation data. Asian stock markets traded mixed overnight. Wall Street closed with a strong rally last week, but with investors waiting for key US inflation numbers, sentiment was mixed.

Late Friday, Moody’s trimmed the outlook on the US credit rating to negative from stable. The factors behind the change included the view that downside risks to the country’s fiscal strength have increased and may no longer be fully offset by the sovereign’s unique credit strengths. It did not help that Congress is again battling to prevent a partial government shutdown. Meanwhile, Moody’s also affirmed the AAA rating, noting it expects the US to “retain its exceptional economic strength” and it suggested “further positive growth surprises over the medium term could at least slow the deterioration in debt affordability.”

*USDIndex held at 2-day bottom, at 105.60.

*USDJPY: Hit new 1 year high, at 151.80 amid wider weakness in the Yen.

*Japanese wholesale inflation slowed below 1% for the first time in just over 2-1/2-years in October, a sign that cost push pressures that had been driving up prices for a wide range of goods were starting to fade. The slowdown in commodity-led inflation is in line with the Bank of Japan’s projections, and puts the spotlight on whether wages and household spending would increase enough to generate a demand-driven rise in consumer prices.

*Stocks: The Hang Seng outperformed, and European futures are also making headway, while US futures are in the red. Bonds declined across Asia, but Treasuries have pared overnight losses, and the US 10-year rate is down -1.2 bp at 4.64%, while the German 10-year yield is up 0.4 bp, and the Gilt yield down -0.1 bp.

*Oil gapped down on the open, reversing partial gains from Friday’s rally, but holds above $76. Any further renewed concerns over waning demand in the United States and China could dent market sentiment.

*Gold remains below $1,950 an ounce but is seeing a positive start to the week as investors react to Moody’s negative outlook on US debt but also as focus turns on US inflation for more cues on the Fed outlook.

*Palladium hovering near 5-year lows.

Interesting Mover: CADJPY – Rising Wedge identified. This pattern is still in the process of forming. Possible bullish price movement towards the resistance 110.5324 within the next 3 days. Supported by Upward sloping Moving Average.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Stock markets are treading water in Europe, after a largely higher close across Asia. The ASX gained 0.8%, the Nikkei 0.3%, while China bourses traded mixed. In Europe GER40 and UK100 are up 0.1% and down -0.1% respectively, while US futures are posting slight gains, as markets wait for the key US inflation report later today.The DXY dollar index has traded in a relatively narrow range so far and is at 105.674.

Late Friday, Moody’s trimmed the outlook on the US credit rating to negative from stable. The factors behind the change included the view that downside risks to the country’s fiscal strength have increased and may no longer be fully offset by the sovereign’s unique credit strengths. It did not help that Congress is again battling to prevent a partial government shutdown. Meanwhile, Moody’s also affirmed the AAA rating, noting it expects the US to “retain its exceptional economic strength” and it suggested “further positive growth surprises over the medium term could at least slow the deterioration in debt affordability.”

*Yen’s quick recovery from 151.91 on Monday probably reflected positioning in the options market

*UK wage growth remains high. Hopes that an easing labour market will limit upward pressure on wages were one of the reasons the BoE has stopped the tightening cycle, but today’s round of data will give those who voted for another hike something to argue with.

*USDJPY – 151.60 – Yen traders brace for risk of deeper drop on US Inflation – 33-year high?

*Treasury Yellen ”Beijing’s heavy financial support for certain industries could pose a threat to other nations” – ” downside risk to the chinese economic outlook that could affect . . . many Apec economies”

*Stocks have recovered from opening losses, with small gains registered on the US500 and US30. The former broke 4-month down channel to the upside.

*Asian & EU equities crept higher – GER40 +0.14%, JPN225 +0.34%.

*Treasuries have found a bid with yields a couple of basis points

*USOIL pick to 78.35 post an OPEC report stating Demand is robust, and “overblown negative sentiment” – The American Automobile Association said the US Thanksgiving travel period will be the busiest since 2019.

*Gold steady at 1945 after yesterday’s rally

*TODAY: German ZEW, IEA report, US CPI. Earnings: Home Depot today, Cisco Systems, Target on Wednesday, then Alibaba Group Holding

BABA and Walmart report on Thursday.

*US CPI preview: Headline inflation fell to 3.3% in October, down from 3.7 % in September.

Biggest Mover: GBPUSD breached 1.2300 – GBP responded strongly post UK jobs data – impressive figures – employment rose (+54K), average weekly earnings up and revised higher.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update - November 15 - Technicals & FOMO adding to the moves.

Trading Leveraged Products is risky

A strong close on Wall Street was followed by a broad rally across Asian markets. An unexpected slowdown in US inflation boosted bets that the Fed’s tightening cycle is over, which brought down yields and benefited equity markets. UK inflation numbers this morning also came in a tad below market consensus, which put pressure on the Pound as investors upped bets that the BoE is also done hiking rates. The markets also brought forward the timing of rate cuts with an 88% probability of a 25 bp easing in May, and 50 bps priced in by July with 100 bps in cuts in 2024. Short covering, FOMO, and the break of technicals added to the gains. The belly of the Treasury curve outperformed on the Fed implications.

*US House voted for a short term funding bill, probably averting a partial government shutdown on Saturday (336 to 95).

*UK: CPI fell to 4.6% y/y from 6.7% y/y in the previous month. It was the lowest since October 2021 and less than half the recent peak of 11.1% y/y in October 2022. Output as well as input prices are already creeping up again and headline numbers for consumer prices remain far too high for the BoE’s liking.

*China: Data was mixed but mostly disappointing, reflecting ongoing sluggish to weak activity heading into the end of the year. Fixed property investment dropped to a -9.3% y/y rate, extending the -9.1% pace of contraction in September. It is disappointing but not surprising given the deepening troubles in that sector. It is the fastest pace of contraction since the -10.0% y/y in December. Residential property sales fell, new property construction & fixed asset investment were down.

*PBoC left its 1-year median lending rate unchanged at 2.50% for a fourth consecutive meeting. The Bank offered 1.45 tln yuan ($200 bln) in cash, the largest net injection since December 2016 as officials try to counter the weakness from the beleaguered property sector.

*EURUSD has soared 2 figures to 1.088, the best since August. It was helped earlier by a better than expected German ZEW investor confidence report.

*USDJPY slumped to 150.25 from the day’s peak of 151.78. It’s been above 150.00 since November 6 and may be able to hold the line there as the BoJ still shows little inclination of normalizing policy this year.

*Stocks surged with the US100 jumping 2.37%, while the US500 climbed 1.9 and the US30 surged 1.43%. Strength was broad based with every S&P sector closing in the green.

*USoil steadied and Gold edged higher to $1971.

*TODAY: US Retail Sales & PPI.

Interesting Mover: USDIndex plunged the most in a year, dropping 2 big figures intraday to a low of 103.81 before closing at 104.05. Next support is at 102.7-103. area.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Stock markets struggled, and the Hang Seng in particular remained under pressure amid lingering concern over China’s growth outlook and a slump in Alibaba Group Hlds. as the company scrapped a spinoff of its cloud business due to US chip export restrictions.

European futures as well as most US futures are also finding buyers amid growing conviction that central bank rates have peaked in the US as well as Europe, which leaves markets looking for the timing of the first rate cut. Bonds are benefiting and yields continue to trend lower. European futures as well as most US futures are also finding buyers amid growing conviction that central bank rates have peaked in the US as well as Europe, which leaves markets looking for the timing of the first rate cut.

*US data once again, helped treasuries and add to the bullish sentiment that has prevailed most of the month.

*US Dollar slid higher to 104.36, up from recent lows, but still heading for a weekly loss, while Yields down as markets price in that Fed done with hiking.

*Euro strengthens after Tuesday’s significant 1.69% surge. Sterling (-0.23%) dive to 1.2375 post an unexpected decline in UK retail sales.

*AUDUSD & NZDUSD down for a 2nd consecutive day.

*Stocks: The JPN225 managed to dodge the trend and the wider MSCI Asia Pacific Index is still heading for a solid weekly gain. The US500 up +0.15%, US30 slipped -0.13% and the US100 0.07% higher.

*Alibaba Group Holding Ltd.’s (-9%) market value has slumped to only about half that of rival Tencent Holdings Ltd , as company had cancelled plans to spin off its cloud computing unit and paused a push to list its grocery chain.

*Walmart (-8% ) plunging, even after in-line earnings, as more cautionary outlook with D-word (deflation) rattling investors.

*Energy: USOil drop nearly 5% s below key $73 support level, leaving oil on course for a fourth weekly correction.

*Metals: XAUUSD spiked to 1988, set for a strong weekly close.

Interesting Mover: USDIndex plunged the most in a year, dropping 2 big figures intraday to a low of 103.81 before closing at 104.05. Next support is at 102.7-103. area.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The US100 declined during this morning’s futures market and also ended Friday’s session lower. However, the instrument is not witnessing any significant downward pressure or momentum, but continues to honor the established price range. According to the Chicago Exchange the possibilities of another rate hike over the next year are virtually zero and 30% of experts believe the Federal Reserve will cut the Federal Fund Rate by 25 basis points in the first quarter of 2024. With the hiking cycle at an end, the market could experience ideal market conditions for a bullish market.

Another positive factor for the US100 and the stocks market in general is the decline in the Dollar and Bond yields. The US Dollar Index has declined by 3.20% this month and continued to decline further this morning. In addition to this, the US 10-Year Bond yield has dropped to its lowest since September 2023. If the Dollar and Bond yields continue to decline throughout the day, the possibility of investor sentiment increasing grows. As a result, the US100 could potentially rise and break the $15,871 resistance level.

Both Asian and European stocks traded higher at the futures market open. Again, if European and Asian investors show a high-risk appetite, something similar may be witnessed in the US.

Over the next two days, the price of the US100 is likely to be influenced by two major events: the Federal Reserve Meeting Minutes and NVIDIA’s third quarterly earnings report of 2023. NVIDIA is the 5th most influential stock within the US100 and holds a weight of 4.58%. The company is again expected to make higher earnings and revenue compared to the previous quarters. The US100 will find significant support, if the earnings per share and revenue is higher than expected.

NVIDIA stocks have increased by 19% over the past month and 2% in the past week. The price movement indicates shareholders are confident ahead of the quarterly earnings release.

Currently the US100 remains above major trend lines and the Volume-Weighted Average Price. However, the instrument is trading within a retracement. Therefore, investors will be keen to see it reach $15,831 which will be enough momentum to obtain a potential buy signal on short-term charts.

GBPUSD

The Bank of England Deputy Governor Dave Ramsden advised markets that the central bank will keep interest rates high for at least 6 months to bring inflation back to its 2.0% target over the medium term. Analysts predict that the central bank will begin reducing borrowing costs in May or June 2024, with three 25 basis point adjustments planned by the end of next year, but for now its pressure on mortgage holders will continue. Currently, it is believed the Fed will cut before the BOE, which could support the Cable. According to a survey by consulting company Savanta, 58% of respondents have late payments now versus 49% the same month last year.

The latest wave on the GBPUSD is a correcting wave aiming for the previous high at 1.24638. However, investors will be monitoring if the exchange rate finds support at this level similar to previous price action patterns.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The US100 broke through a major resistance level, rising to the highest level since January 2022. The instrument rose by 1.20% on Monday forming its fourth consecutive bullish candlestick on a weekly chart. The technology sector in particular witnessed a surge in demand due to its exposure to “growth stocks” which are benefiting from the end to the hiking cycle. In addition to this, the US100 is already pricing in a rate cut as early as March.

The 10 top stocks holding the highest “weight” within the index all rose in value on Monday and from the top 20 stocks only PepsiCo saw a slight decline (-0.14%). From the US100’s components 90% of the stocks ended the day higher. NVIDIA was the best-performing component, rising 2.26% as investors await the release of the third quarter earnings report scheduled for this evening. Analysts expect NVIDIA’s earnings per share to rise 20% compared to the previous quarter. Additionally, the company quarterly revenue is believed to have risen 16%. During this morning’s pre-market hours, the stocks have risen a further 0.30%.

The 10-year bond yields are trading 0.027% lower during this morning’s Asian session and the US Dollar Index is down 0.15%. Both bond yields and the weaker Dollar could potentially prompt investors to increase exposure in the stock market. However, traders should keep in mind investors may look to buy at the discounted price. This could potentially pressure the NASDAQ in the short-term.

Nonetheless, a key influential factor will be tonight’s Federal Reserve Meeting Minutes. The event is still likely to trigger volatility regardless of the fact that the Meeting Minutes is a “lagging” indicator. If the market senses a tone of dovishness or caution, traders will deem the meeting as indicating a potential cut. This is because inflation has declined by 0.5% since the meeting. Indication of a rate cut in the first quarter of 2024 could indicate the continuation of the bullish trend.

A concern for investors was the mini-crisis related to Sam Altman’s sacking as CEO of OpenAI on November 17th. However, Microsoft seems to be emerging as the victor as Mr Altman potentially may join as a Chief Executive of the new research lab. Microsoft stocks, which hold more than 10% of the NASDAQ, rose by 2.05% on Monday and a further 0.28% in pre-market open hours.

GBPUSD

The Bank of England’s Governor yesterday evening advised markets that the regulator may again consider another interest rate hike. According to Bloomberg, almost all analysts are not taking the comment seriously, but see it as an indication that a rate cut in the UK may be further away than originally thought.

The Cable rose by 0.43% on Monday and is trading 0.30% higher during this morning’s Asian session. Early this afternoon the Governor of the Bank of England will again speak, but this time testifying in parliament. Investors will be closely scrutinizing comments looking for confirmation of yesterday’s point of view. The US Dollar Index is again declining this morning; however, investors will also be monitoring the Dollar’s reaction after this evening’s meeting minutes. The Pound on the other hand is experiencing “mixed” price movement against other currencies.

Gold

The price of Gold ended the day slightly lower on Monday but saw a surge in buyers towards the end of the day’s sessions. This morning the price of Gold has risen a whopping 0.81% but has risen to a previous resistance level and price range. Therefore, investors will be monitoring if the asset forms a breakout and continues its bullish trend or if the asset moves into a strong price range which remains intact in the medium term.

According to the report of the US CFTC, last week the number of net speculative positions dropped to 155.4 thousand from 166.2 thousand a week earlier. Sellers are actively exiting the asset. Last week, buyers increased the number of contracts by 2.338 thousand, while the sellers closed 6.150 thousand contracts. This is signaling an increase in the upward dynamics but traders question whether Gold can maintain its momentum above $2,000.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The EURUSD ended the day lower for the first time after climbing for 3 consecutive days. The minutes of the November meeting of the US Federal Reserve supported the Dollar but also had factors which concerned Dollar buyers. Certain members of the Fed’s Committee stated they expect the rate to remain at a high level for “quite a long time”, while others would not give a clear indication of a cut and that rates would remain higher for longer. However, some economists view this as dovish considering inflation has now declined. In addition, the regulator does not exclude the possibility of further tightening of monetary conditions if the rate of decline in inflation continues to slow down. This is where the Dollar can potentially benefit. The question is whether the Fed will consider one last 0.25% hike if inflation refuses to drop below 3%.

Economists’ views have already slightly shifted since the Fed’s Meeting Minutes. According to the Chicago exchange there is now a 5% possibility of a hike in the next 3 months. Previously, the only possibility was a pause for the near-term future.

The US Dollar Index is trading 0.17% higher this morning and is increasing in value against all major currencies. However, the Euro is also increasing in value against all major competitors. Therefore, investors should be cautious about an attempted correction back to 1.09225 and 1.09607. The Euro is being supported by the European Central Bank’s stance on keeping interest rates high for “several more quarters”. The Governor of the Bank of France, François Villeroy de Galhau, said that interest rates in the eurozone had reached a plateau, where they were likely to remain. However, if the possibilities of another hike from the Fed rise, the Euro may struggle to hold onto gains.

If the price declines below 1.08995, sell signals are likely to materialize. Whereas, if the price increases above 1.09225, buy signals will gain momentum again. If the exchange rate had fallen a further 0.25%, the instrument would have broken recent support barriers.

This afternoon investors will be monitoring 3 economic events: The US Unemployment Claims, Durable Goods Orders and Revised Consumer Sentiment. If the Unemployment claims remain stable or lower than expected, while the Goods Orders and UoM Sentiment remain higher, the Dollar could potentially gain momentum.

US100 – NASDAQ Continues Bullish Trend Pattern

The US100 declined 0.75% during yesterday’s trading session but continues to follow the traditional upward trend pattern. Currently the asset is trading above the 60-candlestick trend line and is hovering above neutral on Oscillators. Therefore, a further impulse wave is still possible. However, of the top 5 stocks holding the highest weight within the index, only 1 stock is trading higher during this morning’s pre-market hours (Microsoft +0.12%). Though investors will monitor if this changes when the US open nears.

According to market analysts, there is now a slightly higher possibility of one last interest rate hike, however, the possibility is very slim. According to Bloomberg, if inflation does not rise in December and unemployment remains around the 4% mark, a pause will remain almost a certain outcome. The bond market this morning is significantly declining, dropping 0.022%, which is positive for the US100. Both German and French indices are trading higher in the European market open which is also another positive indication for the US100.

NVIDIA’s Quarterly Earnings Report was significantly higher than expected which is positive “fundamentally”, but so far has not pushed the stock higher. The company’s Earnings Per Share were 19% higher and Revenue rose 25% from the previous quarter. However, the stock has dropped 1.74% in after hours trading. Investors will monitor if demand grows once today’s session opens.

Interesting Mover: USDIndex plunged the most in a year, dropping 2 big figures intraday to a low of 103.81 before closing at 104.05. Next support is at 102.7-103. area.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

McDonald’s Looks to Double Chinese Presence Boosting the US30!

Trading Leveraged Products is risky

US30

The best performing index on Wednesday was the US30 which rose to its highest price since August but is not yet at its peak like the US100. Due to it not breaking previous resistance points and trading at an all-time high, investors may be more comfortable investing in the US30 which is at a lower risk of being overbought.

The US30 was particularly supported by Goldman Sachs and McDonald’s stocks. Goldman Sachs rose 1.26% with investors continuing to purchase the discounted price as the investment banks recover from the 2021-2022 mini-crisis. Investors are also heavily purchasing McDonald’s stocks for similar reasons. McDonald’s stocks dropped 14% in August-October giving investors the opportunity to invest at a more competitive price.

Investors are particularly investing in McDonald’s as the company attempts to enter and control the Chinese Market, similar to Apple in the past. This week the company bought the shares in Chinese company Carlyle Group, bringing its total ownership to 48.0%. The Fund is a joint venture with CITIC Group Corporation Ltd., which owns 52.0% of the shares. The deal is a continuation of the plan to actively capture the Chinese market and increase the number of restaurants in the country. Over the past 5 years, the number of McDonald’s restaurants in China has doubled to 5,500 and it has become its second-largest market. The Board of Directors advises the company to aim to have more than 10,000 restaurants over the next 5 years.

McDonalds is the fifth most influential stock within the US30 and at times has been known as a defensive stock. The company has proven to thrive even during adverse market conditions and recessions.

Bond Yields and the US Dollar Index are trading lower this morning which is also deemed as a positive factor for the US30 and US equities. Investors will be monitoring the price performance of European indices once the European market opens in order to gauge global investor sentiment. However, investors should note that volumes and volatility remain low due to the US bank holiday.

The US30 is trading within the “trend-zone” of regression channels and continues to form higher highs and higher lows. Therefore, the assets continue to formally trade within a bullish trend. If the instrument breaks above $35,333, buy signals are likely to materialize again.

EURGBP

The Euro has increased in value against all major currencies since the second half of yesterday. However, the price will be largely dependent on today’s Purchasing Managers Index, which is one of the most popular and one of the few “leading indicators”. Leading indicators are based on future conditions rather than previous data such as CPI, NFP and other government statistics.

Both French and German PMIs are expected to increase in value compared to the previous month but still remain within the “economic contraction” zone. However, should the two leading EU economies fail to surpass expectations, the Euro may be unable to hold onto gains. The UK will also release its Services and Manufacturing sector PMI 1 hour after their European partners. The UK’s data will similarly influence the price movement of the EURGBP.

Medium-term technical analysis leans more towards a decline in the Euro against the Pound. However, the price will need to decline below 0.87167, for short-term signals to point towards an imminent decline.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

A wait-and-see stance is all but assured at the last policy meetings of 2023 for the key central banks, the FOMC, ECB, BoE, BoC, and BoJ. Disinflationary trends in the West have afforded central bankers the opportunity to move to the sidelines to observe. But we and they will have to monitor the data into the new year to assess the length of the “higher” stance, or to determine whether the next action will be up or down.

The US30 is trading within the “trend-zone” of regression channels and continues to form higher highs and higher lows. Therefore, the assets continue to formally trade within a bullish trend. If the instrument breaks above $35,333, buy signals are likely to materialize again.

Meanwhile this week, the month’s end and the anticipation of key data releases, have generated some caution, with futures markets slightly lower globally.

Key Events of the Week: US and EU inflation data, Powell event, official China PMI & delayed Opec+ meeting. Meanwhile, ECB President Lagarde speaks at the EU Parliament later today.

*PBOC announced it would encourage financial institutions to support private companies, including tolerance for non-performing loans.

*Global stocks on 4-week rally: US500 futures eased 0.2% & US100 lost 0.4%. The US500 rallied for 4 weeks straight and is up 8.7% on the month so far, which would be its best performance since mid-2022.

*Approximately 55% of the S&P 500’s component shares are trading above their 200-DMA the highest share in nearly two months, according to LPL Financial.

*Asian shares slipped today, ahead of potentially market-moving inflation data from the US & EU and the OPEC+ meeting,prompting them to sell stocks to lock in profits. JPN225 fell 0.53% to close at 33,447.67. CSI300 fell another 0.8% and have missed out on all the global cheer with the market down 1.8% in November so far.

*Reuters: Morgan Stanley bought $300 million worth of protection against losses on some of its loans from Blackstone Group and other investors. The deal is one of several such credit risk transfer transactions that US banks are considering in the aftermath of a March crisis in the sector and as regulators look to increase capital they have to hold, bankers, lawyers and investors said.

*Treasury yields are slightly higher, but that hasn’t helped the US Dollar.

*USDIndex is at 2-month low, i.e. 103.30, EURUSD is up at 1.0952, not far from 4-month high of 1.0965 – Markets priced in 80 basis points of US easing next year, and around 82 basis points for the ECB.

*USDJPY pulled back to 148.77 due to the soft Dollar against a broadly firmer Yen.

*USOIL under pressure at $75 area & UKOIL fell to $80 ahead of Thursday’s meeting, as uncertainty regarding Opec outlook and failure to easy market worries of a deeper supply weighs on the energy markets.

*Reports suggest African oil producers are seeking higher caps for 2024, while Saudi Arabia may extend its additional 1 million bpd voluntary production cut, which is due to expire at the end of December.

*Key Mover: Gold climbs to 6-month high in choppy trade, hit $2,017.82. Spot gold may extend gains into $2,027-$2,030.

Medium-term technical analysis leans more towards a decline in the Euro against the Pound. However, the price will need to decline below 0.87167, for short-term signals to point towards an imminent decline.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap: Bonds up; Stocks weaker; DXY set for the worst month in a year.

Trading Leveraged Products is risky

Market Trends:

*Asian stocks fell in response to declines in US and European markets, triggered by hawkish signals from central banks on interest rates.

*Bonds extended gains amid growing conviction that central banks in Europe and the US have concluded rate hikes, with expectations of potential rate cuts next year.

*The US Dollar hovered near three-month lows as investors believed the Federal Reserve had completed its rate-hike cycle, with attention focused on an upcoming crucial inflation report.

Central Bank Developments:

*ECB President Lagarde noted that the central bank’s efforts to control price growth are ongoing, citing strong wage growth and an uncertain outlook despite easing inflation pressures in the eurozone.

*CME’s FedWatch indicated a 95% likelihood that the US central bank will maintain unchanged interest rates next month, but there is a growing possibility of a rate cut gaining traction in mid-2024.

Global Economic Indicators:

*Australia experienced an unexpected decline in retail sales for October, with consumers cutting spending on everything except food.

*Germany saw a slight improvement in consumer sentiment as the Christmas month approached, but it remained at a very low level, attributed to high inflation, indicating no signs of a sustainable recovery in Europe’s largest economy.

Financial Markets Performance:

*Weaker-than-expected home sales and the Dallas Fed manufacturing index weighed on Treasury yields, with the 10-year yield at 4.396%.

*JPN225 closed 0.12% lower at 33,408.39, despite being up 8% for the month, failing to surpass its highest closing level in three decades reached on July 3 in recent attempts.

*JPY gained momentum as the USDIndex hit a three-month low on weaker-than-expected data, while EURUSD dipped to 1.0937, breaching the bottom of a one-week channel with the next support at 1.0925.

*AUD rose to 0.6630, reaching a four-month high, while NZD touched a seven-week high of 0.6114.

*USOIL eased 0.13% to $74.74, and UKOIL dropped below $80 as oil prices fluctuated ahead of an OPEC+ meeting later in the week.

*Gold reached $2,013.80, hitting a fresh six-month peak of $2,017.89 earlier in the session.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap: Dollar slumped; Gold & Oil supported on rising Fed rate cut bets.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

*US consumer confidence improved better than expected, but it follows big downward revisions to October. The consumer confidence rise joins a Michigan sentiment decline to a 6-month low. All the surveys face headwinds from elevated mortgage rates, tight credit conditions, and fears about developments in the Middle East.

*Fed’s Waller (the most hawkish Fed) & Goolsbee are “increasingly confident” that policy is well positioned to slow the economy and get inflation back to 2%. BUT Fed Governor Bowman reiterated she favors more rate hikes if the progress on inflation stalls.

*The RBNZ warned this morning that further policy tightening might be needed if price pressures did not ease.

*German import prices unexpectedly rose 0.3% m/m in October. However, annual import price inflation seems to have bottomed out in August and the trend of ever deeper deflation has been reversed now.

Market Trends

*Fed funds futures rallied on the dovish read. Implied rates popped to suggest about a 70% chance for a rate cut as soon as the May 1 policy meeting, versus about a 55% risk a week ago. However, a significant downturn in growth could spark the more aggressive easing posture as the market is reflecting.

*Treasury bulls took less than hawkish Fedspeak and ran with it. Short term bond yields dropped sharply, to the lowest since July and August.

*Stocks in Asia and US are fractionally higher after a mixed trade most of the session, as Treasury yields and USD hit multi-month lows. JPN225 fell at 33,321 as investors continue their pause in buying.

Financial Markets Performance:

*The US Dollar bears chased the Buck lower. USDIndex fell to 102.36, the weakest since August. – Its worst monthly performance in a year!

*EURUSD broke 61.8% Fib level on July-September downleg, breaching 1.1016. Cable is at 1.2730.

*USDZAR extended to 18.51 lows, JPY jumped to its strongest point since mid-September at 146.66. The NZD surged more than 1% to July’s high of 0.6207.

*USOIL & Gold climbed to $77 from $74 lows, and to $2051.93 per ounce, the highest since May, respectively. The weaker US Dollar, global uncertainties, and rising Fed rate cut bets supported Gold and Oil.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap: Stocks loosing their steam; Oil rallies ahead of OPEC+.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

*The US GDP report implied a Q3 productivity growth boost to a robust 5.1% from 4.7%, after an unrevised 3.6% Q2 clip. There was a Q3 growth rate trimming for the hours-worked index to 1.0% from 1.1% due to weakness in the hours-worked data in the last employment report.

*Fed rate cut bets deepened thanks to the lack of pushback from most Fed officials, and expectations for this pivot continued to drive the markets. There was no impact from the 5.2% GDP print.

*China’s manufacturing sector contracting for a 2nd consecutive month in November and performing worse than forecast indicates weakening momentum despite increasing government efforts to boost growth.

*EU: French inflation dropped sharply & German retail sales bounced in October. It was the first real improvement since May, which is likely also related to the moderation in inflation.

Market Trends

*Treasury yields richened further, and especially at the front end. Fed funds futures brought forward an easing in the policy rate to May from June. The curve dis-inverted to -38 bps on the bull steepener.

*Bonds are set to post the best month ever. Concurrently, the rate cut frenzy has boosted EGBs too, sending the global index to its best since 2008 the financial crisis.

*Stocks traded cautiously and lost steam into the close, as several Big Tech companies offset gains. The US30 gained 0.04%, while the US100 dropped -0.16%, with the US500 off -0.09%. Asian stocks were mixed as well, with CSI300 adding 0.5%.

*Meta fell 2%, Alphabet gave up 1.6% and Microsoft dropped 1%. General Motors surged 9.4% after the company announced a big stock buyback.

*The VIX was up 2.2% to 12.97, recovering from the 12.46 low from last week that had not been challenged since January 2020.

Financial Markets Performance:

*The US Dollar steadied at 102.80, with a 102 handle for a 3rd straight day. It’s slumped from the October 3 peak of 107.00.

*EURUSD reversed below 61.8% Fib level on July-September downleg, at 1.0945. It remains well above 1.09.

*USDJPY retests a potential break of its 146.70 low for a 2nd day in a row, USDCAD extends below 1.36 confirming an ascending head and shoulders formation in the daily chart.

*Gold edged up 0.16% to $2044.18 per ounce.

*USOIL climbed 2% to $78.79 per barrel ahead of the OPEC+ meeting. The delayed meeting of the expanded OPEC+ group will be held online.

*Bitcoin still hovering near the $38,000-mark.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

A November to remember. The markets were all over the place to end the month. While the FOMC is still the focal point, repositioning after some big moves on the month and positioning into year-end were the main drivers. The FOMC has reached peak rates, according to Fed funds futures, and rate cuts are the next action, now fully priced for May.

Economic Indicators & Central Banks:

*PCE: Data has been mixed but generally reflect progress on the FOMC’s inflation goal and has convinced markets that rate cuts are underway — core PCE fell to 3.5% y/y from 3.7% y/y previously, but is still well above the 2% target. US pending home sales declined.

*OPEC+ announced an additional 1 mln barrels in cuts. The cuts will be announced individually by members, according to delegates. The Saudi Arabia is expected to extend its down voluntary cut of 1 million barrels.

Market Trends

*Best month in 40 years! Treasuries rallied on FOMC expectations. But profit taking ahead of comments from Chair Powell today unwound some of the froth. The curve steepened to -36 bps versus -50 bps Monday.

*Stocks: Wall Street befittingly finished mixed. The US30 rallied 8.9% with the US100 up 10.7%. For the month the US30 was up 8.8%, its second best November since 1980, according to Bloomberg.

*For the S&P, 10 of the 11 sectors are higher on the month.

*Asia Stock markets were under pressure overnight, with the Hang Seng underperforming, despite a better than expected China Caixin manufacturing PMI that managed to lift above the 50 point no change mark again.

Financial Markets Performance:

*The USDIndex finished at 103.40 recovering from the slide to the 102.36 the prior two days after weaker than expected European and Chinese data.

*EURUSD broke below 1.09, indicating a possible reversal of the 2-month rally, however 1.0830-1.0860 remains the key support area.

*USDJPY rebounds to 148.30, USDCAD dips further into 1-year triangle with immediate support at 1.35, while GBPUSD settles above 1.26 despite US Dollar appreciation.

*Gold slipped about -0.4% to the $2036 area on the rise in yields and some fading of haven trades.

*USOIL slumped 2.9% to $75.59 after spiking 2.2% to $79.60 after OPEC+ announced a further production cut.

*Key Mover: EURCHF down by 1.26%. Next Support levels: 0.95, 0.9440 and 0.9375.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The holidays got a little cheerier amid signs that the major central banks have come to the end of their aggressive tightening postures. Despite protestations from policymakers to the contrary, the markets are now building in the start of rate cuts in 1H 2024. Those hopes underpinned one of the best November’s on record for bonds and stocks, and helped boost gold to a new record high!

Economic Indicators & Central Banks:

*The market sentiment remains uncertain, as Chair Powell did not offer much pushback to expectations that rate cuts are the next move on the agenda or that there was a massive easing in financial conditions in November.

*The US November payrolls report on Friday is crucial for market expectations of rate cuts.

*Analysts anticipate a soft landing for the US economy, with positive but below-potential growth in the next six quarters.

*BofA notes a positive outlook for emerging markets, which are experiencing historically positive returns after the last Fed hike.

Market Trends

*Fed Chair Powell reminded investors the bank is not in a hurry to cut rates and yields are off Friday’s lows.

*Treasuries and Gold declined from session highs. Yields rose across various tenors in Treasuries, with the 10-year trading around 4.23%.

*Asian shares showed mixed results, with gains in Australian and Korean stocks, while Japanese equities fell. JPN225 closed down 0.6% at 33,231.27 after earlier sliding as much as 1.22%. European and US stock futures remained stable.

Financial Markets Performance: