Asian stock markets sold off, with Hang Seng and CSI 300 extending yesterday’s slide, as concern about China’s property sector deepened. Evergrande Group’s mainland unit said it failed to repay an onshore bond, which added to uncertainty over the future of the developer. Attempts to get restructuring plans back on track are ongoing, but investors are worrying about the risk of a potential liquidation.

European and US futures are also in the red, as Treasury yields continue to rise. The hawkish, higher for longer stance from the FOMC and most major central banks has put bears in control. Fears over sustained inflationary pressures, largely thanks to the resilient economy and higher oil prices weighed. The advent of supply is adding to the rise in rates too.

Moody’s also noted that a government shutdown, which is possible at the end of the month, would be a “negative” for ratings. Wall Street also reversed opening losses with the bump in risk appetite also hurting Treasuries.

*FX – USDIndex has cleared the 106 mark as risk aversion picks up. EURUSD and GBPUSD both broke below 1.06 and 1.22 support levels respectively. The USDJPY firmed to an intraday high of 149.18.

*Stocks – JPN225 slipped 1.0% to 32,054, ASX dipped 0.5% to 7,044.90, Hang Seng shed 0.9% to 17,576.83, while the Shanghai Composite fell 0.2% to 3,109.69. Amazon rose 1.7% and was the strongest single force pushing up the US500. US500 fell 0.4% as of London open, while US100 futures fell 0.6%.

*Commodities – Oil slipped below 88.00, with next support level at 86, due to US Dollar strength, which looks to outweigh supply tightness.

*Gold- retested 200-day SMA at 1909.

Today: BoE Governor Bailey’s meeting of the central bank’s Financial Policy Committee and US CB Consumer Confidence & New Home Sales.

Interesting Mover: VIX (+5.5%) extending to 1-month resistance at 18.20.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 27 – Temporary Optimism?

Chinese indexes stabilised after a 2-day decline amid fresh optimism that official measures will be able to boost the recovery. Industrial profits improved for the first time in a year and the People’s Bank of China said it would step up policy adjustment and implement monetary policy in a “precise and forceful” manner to support the economy. Confidence in China’s recovery has been going up and down for so long now, that investor confidence could take lasting damage.

The omnipresent fear of the FOMC’s higher-for-longer policy stance (and indeed that of the ECB, BoE, and BoC) remains a major worry and was exacerbated after JPMorgan’s Dimon noted the potential for a 7% rate as a worst case scenario. Additionally, the threat of a US government shutdown this weekend and Moody’s warning of the potential negative impact on ratings rattled too and left buyers sidelined. Technicals have played a part as well with key levels in stocks, bonds, and the USD having been broken. The drop in September consumer confidence, manifested the anxieties and added to the selloff.

*USDIndex continued to rally and firmed to its 2023 and 10-month high as it benefited from a haven bid, along with the relative outperformance of the US economy and rate differentials.

*EURUSD and GBPUSD posted fresh lows at 1.0554 and 1.2134. The USDJPY is steady at 149.15.

*Stocks – Hang Seng and CSI300 rose 0.7% and 0.4% respectively. Futures are mixed across Europe and slightly higher in the US, after Wall Street dragged down to the lowest levels since early June. The US100 tumbled -1.57% to 13,063.6. News that the FTC was suing Amazon helped knock big tech sharply lower. The US500 was down -1.47% to 4273 with 90% of the index and all sectors in the red. The US30 slid -1.14% to 33,618, slumping below its 200-day moving average.

*Commodities – Oil rebounded to 90.80 as API reported a fall in inventories in Oklahoma.

*Gold – broke 1900 and currently settled to 1895.50 as haven demand favors the Dollar rather than the precious metal. China jitters have flared up & expectations that central banks are sticking with the “higher for longer” messages have added to pressure on bullion.

Today: US Durable Goods.

Interesting Mover: Gold broke 1900, with next Support levels at 1885 & 1870.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 29 – Dollar off 10-months high; Yen regains ground.

Stock as well as bond market are moving higher at the end of the quarter. GER30 and UK100 are up 0.7% and 0.8% respectively, after the Hang Seng bounced 2.7%. US futures are also posting gains, and yields are coming down. The German 10-year rate has corrected -5.1 bp, the 10-year Gilt yield is down -3.9 bp and the US 10-year rate has dropped -2.4 bp.

The omnipresent fear of the FOMC’s higher-for-longer policy stance (and indeed that of the ECB, BoE, and BoC) remains a major worry and was exacerbated after JPMorgan’s Dimon noted the potential for a 7% rate as a worst case scenario. Additionally, the threat of a US government shutdown this weekend and Moody’s warning of the potential negative impact on ratings rattled too and left buyers sidelined. Technicals have played a part as well with key levels in stocks, bonds, and the USD having been broken. The drop in September consumer confidence, manifested the anxieties and added to the selloff.

*USDIndex reverted to 105.54 from 106.50 giving the Yen some breathing room amid intervention concerns. The USDJPY slide to 148.50 has put investors on high alert for the risk of intervention. But Japanese authorities could find propping up their currency both difficult to achieve and hard to justify. (Reuters)

*Stocks up on the last trading day of the Q3 amid optimism over spending during China’s Golden Week holiday and on talks of a possible meeting between US and China leaders.

*UK: Q2 GDP was confirmed at 0.2% q/q & German retail sales unexpectedly correct again coupled with weak consumer confidence readings.

*US: Tight reading on jobless claims, a mixed GDP report & US mortgage rates at the highest level since 2000, as elevated interest rates and climbing bond yields push up borrowing costs.

*Gold at $1858, braced for their biggest monthly fall since February.

Today: The key US PCE but a partial government shutdown is looming, which could affect the release of any economic data.

Interesting Mover: USDJPY (-0.40%) pulled back to 148.50, after a rally closed to the 150 level. However, key support remains at 148.00.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 2 – Shutdown postponed as Q4 kicks off.

Just a few hours before the Saturday midnight deadline, Democrats and Republicans passed a short term bill (45 days) to keep the government funded into November and avoid a shutdown which would have put the paychecks of some 3 million Americans in the public sector and the military at risk. This is certainly not an optimal and confidence-inducing solution in the long term: however, the markets are increasingly accustomed to such events, which have occurred over 20 times in the last 50 years, including 4 in the last decade. It may be this, it may be the start of the new quarter, it may be the good data from Asia, but this morning there is a slight risk on, with the US and European indices up by an average of +0.3% and oil also rising after two bad sessions that saw it pulling back from previous annual highs. The good news came from Asia, where manufacturing in China bounced back into the expansion zone for the first time since last April – as witnessed by the Caixin – and also in Japan, the Tankan Survey saw optimism grow in this side of the productive tissue. This morning we are also seeing very different calls from 2 major US investment banks, with GS seeing demand for both oil and copper booming in China while CITI is taking the opposite view and sees weakness in industrial metals – with possible falls in the range of 5-10% – and Crude falling to $70 in early 2024. However, after September proved to be a particularly negative month with falls of up to 5.8% in the case of the Nasdaq, investors want to start off on the right foot and celebrate the agreement reached in Washington at the same time as they anticipate Federal Reserve Chairman Jerome Powell’s remarks later today.

UKOil – USOil spread is narrowing

*FX – USDIndex just shy of 106, +0.15% @ 105.97; AUDUSD is the laggard among majors -0.30% @ 0.6414, *USDJPY is trading at 149.65 after having hit a new 2023 high at 149.82. EURUSD flat, GBPUSD @ 1.22.

*Stocks – US Futures are inching higher (US500 +0.40%, US100 +0.50%, US30 +0.39%%); EU futures are up as well (GER40 +0.35%, FRA40 +0.41%). September was a grim month: US30 -3.5%, US500 –4.9%, US100 -5.8%. Performances were negative for the whole Q3: -2.6%, -3.7%, -4.1% respectively.

*Commodities – USOil +0.64% at $91.32, UKOil is trading at $92.65 and their spread has narrowed to just $1.33, in the lower bound of this year’s range.

*GOLD – -0.19% @ $1845, XAGUSD adds another -1.44% to its recent prolonged drop, trading at $21.88.

Today: Highlights include Spanish, Italian, German, French, EZ, UK & US PMIs, US ISM Manufacturing, Fed’s Powell & Williams.

Interesting Mover: XAGUSD (-1.44% @ $21.88) had a wild session on Friday with a sharp reversal and an excursion of 6.16%. The trendline that originated in August 2022 has been broken, but there is another longer-term one currently passing through the $20.50 area, while $21.50 is a strong static support; the price is below its 50d and 200d MAs.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 3 – Risk off bites across asset classes.

Starting with APAC, the RBA has just unsurprisingly kept rates steady in Governor Bullock’s inaugural meeting with the statement largely a carbon copy from the Lowe era (”inflation is coming down, the labour market remains strong and the economy is operating at a high level of capacity utilisation”): AUD continues to decline this month and is -0.76% against the USD right now, followed by the KIWI which marks -0.63%. The JPY, which is one step away from 150, is surprisingly strong this morning, flat against the USD, as the rhetoric about the possibility of intervention continues, this morning from Japan’s Finance Minister Suzuki. The JPN225, for its part, is down -1.85% and back to last June’s levels, but the whole of APAC is suffering: Hong Kong and China are back to trading and the former is down -3.04%, weighed down by developers and the energy sector. Moreover, the IMF has lowered growth expectations for the area.

US Yield Curve

More broadly, we are seeing a series of risk-off movements, evident in the strength of the USD which, after +0.75% yesterday, is now within touching distance of 107. Yesterday afternoon’s decent US ISM data helped long end yields continue to rise (10-Year at 4.691%) while continued weakness in Eurozone manufacturing sank the EURUSD below 1.05. European stock markets suffered more than American ones, which showed more indecision and ended the day mixed. But while the mega-cap filled Nasdaq finished at +0.83%, the RUSSELL 2000 index of small to mid-cap companies is now negative YTD. Finally, the weakness in precious metals was significant, with Silver plummeting -5.81% below $21; energy also sold off, with OIL down for four consecutive sessions and UKOIL down 8% from last Thursday’s high.

*FX – USDIndex +0.24% @ 106.86 after +0.75% yesterday; AUDUSD -0.73% @ 0.6316, NZDUSD -0.56%. YEN strengthens 0.03%, 149.82, USDCNH steady at 7.32. EURUSD -0.08% @ 1.0469 and CABLE at 1.20 handle after yesterday’s heavy session.

*Stocks – US Futures fractionally negative (US500 -0.12%, US100 -0.17%, US30 -0.11%). RUSSELL 200 turned negative YTD. EU futures -0.2% on average after both GER40 and FRFA40 lost -0.9% yesterday. APAC heavy: HK -3%, CHINA50 -1.53%, JPN225 -1.90%.

*Commodities – USOil -0.28% at $88.35, UKOil -0.44%, Wheat -0.13%, Corn -0.61%.

*Metals – Gold -0.27% @ $1822, XAGUSD @ 21.03, Copper -1.03%, Palladium -0.35%.

Today: highlights include US IBD/TIPP & JOLTS, Swiss CPI, Australian PMI (Final), Fed’s Bostic, ECB’s Lane & Valimaki.

Interesting Mover: Copper -1.0% @ $3.6065, is clearly losing the $3.70 area and below the $3.62 support, has been rejected by its 50MA and lost 1yr long uptrend, $3.53 is its next relevant support.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 4 – On the way to old normal.

Yesterday at 08:30 am ET (New York Time), JOLTS job openings for August again showed an incredibly buoyant labour market with 9.61m new available vacancies versus the 8.8m analysts were expecting. Even though the main target is inflation, this is not what the Fed wants to see and the voice saying ”higher for longer” immediately resonated in traders’ minds. Bonds immediately sold off and the 10-year Treasury yield surged to its highest level since 2007, up 11 bps to 4.80%; Futures on 30y at the same time slid as much as 1.58% with the yield up to 4.924% and 30y mortgage rate approached. There are certainly deeper fundamental reasons, such as the continuing large US deficit at the same time that China and Japan have stopped being net buyers of US debt, with the former selling $40B a month since April and having already dumped $300B since 2021. However, it is not the current levels of rates that are abnormal, but rather those of the last 10 years. The current situation is actually back to the old normal.

10Y US Future

More than anything else, another thing caught the eye: after the data, USD immediately surged and broke 150 against the JPY, touching 150.16. And this is where the BOJ finally INTERVENED and caused the pair to fall 290 pips (or nearly 2%) in less than 5 mins. That doesn’t seem to be enough and now the USDJPY is trading back at 149.22: the Japanese currency’s structural weakness is still great at the moment, although the 1-year overnight swap is over 1% and the 3m-10y curve has never been steeper. The intervention has not been confirmed by the Ministry of Finance, and there is some rumour that it may actually have been just a Request For Quote that made primary dealers remove all bids and then triggered stop losses in minor players accounts.

Obviously this is not a good environment for equities and yesterday US equities underperformed their European peers with the US100 down 1.83% and the US30 ending in negative YTD territory (a day after the Russell). The US500 is now testing its 200 MA. The VIX flew above 20 and – some potentially good news – the inversion that can be seen between the spot and 3-month futures has indicated a market bottom in the past. But beware, history – when it repeats itself – almost never does so in exactly the same way.

At least commodities breathed easy and silver rebounded after the previous day’s sell-off.

*FX – USDIndex +0.18% @ 106.93; USDJPY hedging up +0.08% at 149.17, Aussie at 2023 lows (0.6307), Kiwi is today’s laggard, -0.44% at 0.5883.

*Stocks – US Futures negative again and heavy: US500 -0.57% and testing its 200 MA, US100 -0.78%, US30 -0.40% further into negative territory YTD. DAX future is testing 15k right before the cash open. Yesterday AMZN -3.66%, TSLA -2.02%, NVDA -2.82%, MSFT -2.61%.

*Commodities – USOil resumes its decline -0.76% at $88.72, UKOil -0.67%.

*Metals – Gold -0.17% @ $1819.64, XAGUSD @ 21.03, Palladium -1.21% below its ST floor.

Today: highlights include EZ, UK, US Services and Composite PMIs, EZ PPI, Retail Sales, US MBA, ADP, ISM, Durable Goods, OPEC+ JMMC, ECB’s Lagarde.

Interesting Mover: USDJPY -0.03% @ 149 after the shock of the intervention has recovered 2 handles and set 2 levels to be watched, 150 and 147.25 approx, while the trend is still clearly rising.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 5 – Markets try to take a breather, oil slumps.

Rebounding from some pivotal, psychological levels, the vast majority of world equity indices rose yesterday, helped by a decrease in yields. Buying in the US intensified in the last minutes of trading led by large-cap techs such as TSLA (+5.93%), MSFT & AMZN. US500 was up 0.8%, its largest rise in 3 weeks and US100 settled +1.5% at the end of the day. As mentioned above, after reaching a high of 4.88% during the Asian session, the 10Y benchmark was lower later in the day, ending the day almost 15 bps lower. Part of this was due to the rather worse-than-expected ADP jobs data, which helped consolidate expectations of a further Fed pause in November (now at 80%). One aspect that the financial media are somewhat glossing over as they are concentrating on the gigantic -46% drawdown on the long end of the US curve – is the great steepening of the 2y-10y, now at 32bps (it was -1% at the end of July). Also on the US side, while we anxiously await tomorrow’s NFP data, it should be noted that today marks the end of the suspension of student debt payments decreed after Covid which will probably weigh heavily on many households. In Europe and the UK, better-than-expected composite PMI data helped the respective currencies to do well, while the USDIndex is also near overbought levels.

The big mover of the day was Oil, with crude very heavy (-5.6%) on the day of the OPEC+ JMMC, characterised first by Russia and Saudi Arabia’s apparent willingness to continue with production cuts, then by Novak’s (Russia) statements that ”OPEC+ may tweak its decisions if needed… as we see a record-high global oil demand”.

*FX – USDIndex -0.09% @ 106.43; GBPUSD & EURUSD flat today (1.2137/1.0506) after rising +0.5% & +0.36% respectively yesterday, USDJPY 148.78, USDCAD is -0.06% @ 1.3736 after rising approx. 2.65% since 20/09. Swiss Franc is strengthening, USDCHF-0.08% @ 0.9165.

*Stocks – US and EU futures fractionally negative this morning, -0.1% and -0.2% on average respectively. Yesterday TSLA +5.93%, MSFT +1.78%, GOOGL +2.23% AMZN +1.83%.

*Commodities – USOil rebounded this morning +0.44% at $84.79, UKOil +0.52% @ $86.40.

*Metals – Gold flat @ $1821.47, XAGUSD +0.57% @ 21.12.

Today: highlights include GE Trade Balance, US Jobless Claims, Fed’s Mester, Barkin, Daly, ECB’s Lane & de Guindos.

Interesting Mover: USOil ($83.50) has lost its 3m long uptrend, is below its 50MA and testing a strong support level at the $83.50 area, with RSI (14) at 39.72.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 6- Wait and see: NFP ahead.

It has been a quiet day in the markets with subdued volumes and small changes: in America US30 ticked down 0.03% while both US500 & US100 lost around 0.1% and volumes have been 15% lower than the 30-day average. But European indices and other asset calls such as metals also showed a lot of indecision, drawing what in candlestick analysis is called a Doji. The situation was somewhat different for the USD and Oil, which fell, in the case of the latter strongly.

The market awaits the September NFP data today after the picture that has emerged so far this week from the labour data has been mixed: we had a strong JOLTS report while ADP payrolls disappointed; yesterday’s Claims varied very little leaving room for indecision. Investors are worried about the possibility of a very positive NFP which could put new pressure on bonds and equities: yesterday the 10Y weakened to 4.73% but there are some market watchers – including bond king Bill Gross and Jamie Dimon – who see the possibility of quite higher levels in the future. Anyway, back to NFP, the average expectations are for +170k new jobs created, down from +187k in August and estimates range from +145k to +240k with the big US banks (Citi, BOFA) skewed to the upside.

NFP Readings

A note on the various speeches the central bankers are giving these days: yesterday both NY Fed’s Davy and ECB’s Villeroy empathized that the current monetary levels are appropriate, and expectations are correctly pricing future 2023 moves (no more hikes). Finally, Oil keeps falling and that is good news: Russia is lifting its Diesel exports ban but Curve is still in backwardation.

*FX – USDIndex +0.17% @ 106.26; USDJPY < 149, EURUSD -0.11% @ 1.0542, Cable -0.15% @ 1.2174. The once mighty MXN peso is falling hard vs USD, this morning +0.20% and +7.49% from 20/09. USDZAR flat not far from 2023 highs 19.51.

*Stocks – Equity futures are slightly negative this morning, US500 -0.1%, Europe is mostly flat with FRA40 outperforming +0.05% at 7020.

*Commodities – USOil +0.05% at 82.58$ pauses its drop close to a mild support level.

*Metals – Gold flat @ $1820.78, XAGUSD -0.20 @ $20.92, Palladium -0.67% and Copper $3.56 are still weak and below their recent floors.

Today: highlights include German Industrial Orders, US NFP, Labor Force Participation and Unemployment rate, Canadian Employment, Fed’s Waller.

Interesting Mover: USDMXN is up 7.49% since 20/09 lows, shows higher highs and trades above 50-200 MAs. 18.40 – 18.55 is a mild resistance area, RSI14 marks 72.24.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 09 – “Long and Difficult war”.

Rising geopolitical tensions fueled a rise in risk aversion at the start of the week. Oil prices spiked amid escalating tensions in the Middle East and the Dollar picked up haven demand. The surprise Hamas attack on Israel boosted Gold and US currency. The USDIndex is trading at 106.12. USOil prices rose in early Asian trading on Monday amid concerns that Hamas’s attack on Israel will increase tensions across the Middle East and affect output from leading producers. The White House confirmed deaths of ‘several’ US citizens in Hamas attacks.

Germany: The industrial production corrected -0.2% m/m in August. If oil prices rise further, the risks to growth will pick up, also because a fresh pick-up in inflation will weigh on consumer demand and complicate the situation for the ECB.

Japan and Hong Kong were closed for holidays. In the US only equity markets are open today, with bond markets and Fed closed for Columbus Day. Chinese stocks declined on Monday morning, as markets returned from a week-long holiday that prompted disappointing levels of spending and travel.

US NFP: Nonfarm payrolls blew past estimates, surging 336k in September, with a net 119k upward revision to the prior two months. That put a November Fed rate hike back on the table and the markets responded as would be expected with Treasury rates surging, the USDIndex popping, and stocks sagging. But other parts of the report were more mixed which helped alleviate Fed fears while dip buyers, short covering, and technical buying ahead of the long weekend helped trim bond losses.

*USDIndex edged up to 106.13 from 105.82 while the Yen steadied at 149 lows. The EURUSD slide back to 1.0540 lows indicating a potential resumption of the long term downtrend while Cable settled at 1.2190. The Australian Dollar, seen as a proxy for risk appetite, slid to 0.6347, while the Kiwi edged lower to 0.5968.

*Stocks: The CSI300 corrected -0.2% as mainland China markets returned from the Golden Week holiday. The ASX managed to nudge 0.2% higher. GER40 and UK100 are in the red, as are US futures.

*Oil: USOil and UKOil gapped up to 85.95 and 87.81 respectively a day after Israel’s PM, Benjamin Netanyahu, warned of a “long and difficult war”.

*Gold at $1855.50, as traders flocked to safer assets.

Interesting Mover: USOil and UKOil both retest 38.2% Fib. from September’s downleg, with USOil posting a death cross in the 4-hour chart.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Stock markets have stabilised and mostly moved higher overnight, after a largely stronger close on Wall Street. Markets continue to assess the impact of the Israel-Hamas war, but the JPN225 rallied 2.4% on its return from the extended holiday weekend. General uncertainties and fears of an escalation of the conflict weighed on sentiment but strength in defensive shares helped support. European futures are higher, with indexes set to pare yesterday’s losses. US futures are narrowly mixed. Treasuries rallied in catch up trade and the US 10-year rate has corrected -14.6 bp to 4.66%. Treasuries jumped and shares advanced after comments by Federal Reserve officials fueled speculation the US central bank may stand pat until year-end.

Oil prices as well as Gold benefited from a spike in risk aversion prompted by the escalating conflict in the Middle East. Gas prices also spiked as investors weigh the risk of widening geopolitical tensions.

*USDIndex has lifted to 105.95, after correcting on dovish leaning Fed comments yesterday. The USDJPY recovered to 148.92 from 148.16 lows.

*China: The largest private real estate developer, Country Garden, said it might not be able to meet all of its offshore payment obligations when due or within the relevant grace periods. Meanwhile, Kaisa Group said creditors would get less than 5% of their money back if it is forced into liquidation

*Stocks: JPN225 rallied 2.4%, while Hang Seng and ASX also moved higher.

*Oil: USOil have come down and it is currently trading at $84.17 per barrel.

*Gold ended at $1861, the highest since late September, from a low of $1844.25.

Today: BOE releases minutes of financial policy meeting & ECB President Christine Lagarde participates in session at IMF/World Bank meeting.

Interesting Mover: AUDUSD has breached the 61.8% fib. resistance line, indicating a potential move to 0.6471 if there is a confirmation of a breakout. Currently it`s in a correction mode.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – Asia stocks hit 2-week high as Fed talk turns dovish.

Stock markets moved higher overnight, as jitters over the Israel-Hamas war continued to ease and traders trimmed expectations for further rate hikes in the US. There were also reports of further and more comprehensive stimulus measures for China, although while the Hang Seng rallied, the CSI 300 managed only fractional gains. European futures are in the red, after a broad rally yesterday. US futures are narrowly mixed.

Germany: HICP is still nowhere near the 2% target and with oil prices already backing up again, and wage growth still high, inflation is likely to continue to overshoot target for the foreseeable future.

*USDIndex: At 105.95, after correcting on dovish leaning Fed comments yesterday. The USDJPY recovered to 148.92 from 148.16 lows.

*Stocks: Treasury yields continued to drop and Wall Street extended recent gains amid rising expectations the FOMC is done. A haven bid has helped support Treasuries too. Wall Street climbed with the US100 rising 0.58% while the US500 advanced 0.52%. The US30 improved 0.4%. Gains were broad-based.

*Oil prices have continued to nudge down from the high of $87.24 per barrel seen early on Monday as markets continue to weigh the impact of Hamas’ attack on Israel over the weekend. USOIL is currently at $84.50, UKOIL at $87 per barrel. The direct impact may be limited, but there remains concern of a widening of the conflict and escalating tensions across the Middle East. If evidence of direct involvement from Iran is found, US sanctions on Teheran could also be tightened. Iran has raised production to a five-year high, but most oil is being shipped to China. Meanwhile, Reuters reported that Venezuela and the US have made progress in talks that could provide sanctions relief to Caracas by allowing at least one additional foreign oil firm to take Venezuelan crude oil – under certain restrictions.

*Gold gained more than 2% yesterday and another 0.39% so far today, at $1868 as haven flows spiked.

Today: US PPI & FOMC Minutes.

Interesting Mover: COCOA up by 1.25% to 3473 retesting the upper line of 12-day channel.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 12 – The key US Inflation.

Stock markets moved higher across Asia, with the Hang Seng outperforming again as tech stocks strengthen. China stimulus hopes are also helping, and the CSI300 lifted 0.9%. The JPN225 bounced 1.8% after a stronger close on Wall Street yesterday. Last night, FOMC minutes were largely in line with expectations and what came out of the September policy meeting and dot plot. Expectations the FOMC and likely the ECB and BoE were at peak rates continued to keep a bid in bonds. Most Treasury yields richened for a fourth day out of the last five as haven demand and dovish Fed expectations underpinned. The long end outperformed in a curve flattener after a hotter than expected PPI report weighed on the front end. Bunds are outperforming in early trade and Eurozone spreads are narrowing. The short end continues to underperform, but 2-year rates are also down in Germany and the US.

US CPI Forecast: It is expected to show gains of 0.2% for the headline and 0.3% for the core after respective increases of 0.6% and 0.3%. CPI gasoline prices look poised to pop 1.4% in September. However, we expect dissipating upward pressure on core prices into 2024 as disruptions from global supply chain bottlenecks and the war in Ukraine subside. As-expected September CPI figures would see the y/y headline decelerate to 3.5% from 3.7% in August, and down from a 40-year high of 9.1% in June ’22. We expect the core y/y gain to slow to 4.1% from 4.3%, and versus a 40-year high of 6.6% in September. Though still well above the 2% target, the further signs of slowing could be sufficient for all but the most hawkish on the Committee, to favor no change in rates next month, especially given the tightening in financial conditions through early October.

*USDIndex eased further on the softer Fed view, but ranged narrowly between 105.80 and 105.20.

*UK: GDP rose 0.2% m/m in August, while the July reading was revised down to -0.6% m/m from -0.5% m/m reported initially. The visible trade deficit widened and apart from the rebound in services, the report still signals a weakening economy. If latest surveys are anything to go by, September will look worse, as the bounce in services doesn’t seem to have lasted long. The September Services PMI was firmly in contraction territory, with no sign of a quick recovery. The outlook then is not great.

*Stocks: Wall Street caught a bid into the close and finished in the green after a choppy session as investors gauged the potential spread of hostilities from the Israel-Hamas war. The US100 advanced 0.71%, while the US500 and US30 were up 0.43% and 0.19%, respectively. Defensive-related sectors in the US500 outperformed.

*USOil prices down for the third day in a row, with key resistance at $83.

Today: US Inflation & Jobless claims.

Interesting Mover: Gold broke $1880 (20 DMA & 50% Fib.) as markets scale back US rate hike expectations and the USD corrects. Haven demand amid raised geopolitical risk in the Middle East also continues to underpin demand for the precious metal.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Stock markets sold off across Asia, after a weaker close on Wall Street. Rate hike concerns picked up again in the wake of the hotter than expected US inflation print yesterday and still tight jobless claims numbers and put stocks on the back foot. The reports saw the market price back in risk of another Fed rate hike this year of about 38%, though the probability was briefly as high as 50-50. The data, the threat of another Fed hike, and geopolitical risks soured investor sentiment.

European futures are also in the red, while US futures show signs of stabilisation. The 10-year Treasury yield is down -3.3 bp at 4.664%, as the curve shifts lower. In the Eurozone, the short end is outperforming, but the 10-year Bund yield is also down -1.0 bp at 2.71%, while spreads are coming in.

*USDIndex has moved off the highs seen in the wake of yesterday’s data and is at 106.20. USDJPY is hovering below 150 as the yield gap with the US widened on hotter-than-expected inflation data.

*Yields: Yields cheapened further on the back of the poorly subscribed bond auction. The bearish action in Treasuries has given an excuse to take profits. Treasury yields rose to their highest levels of the week.

*Stocks: Wall Street slipped and closed with a -0.63% drop on the US100, -0.62% on the US500, and -0.51% on the US30.

*UKOIL is set for a weekly gain of over 2%, while USOIL is set to climb about 1% for the week as investors keep an eye on the Middle Eastern exports due to the Gaza crisis. USOIL up to $83.70.

Today: ECB President Lagarde, FOMC Member Harker & BOE Gov Bailey speak.

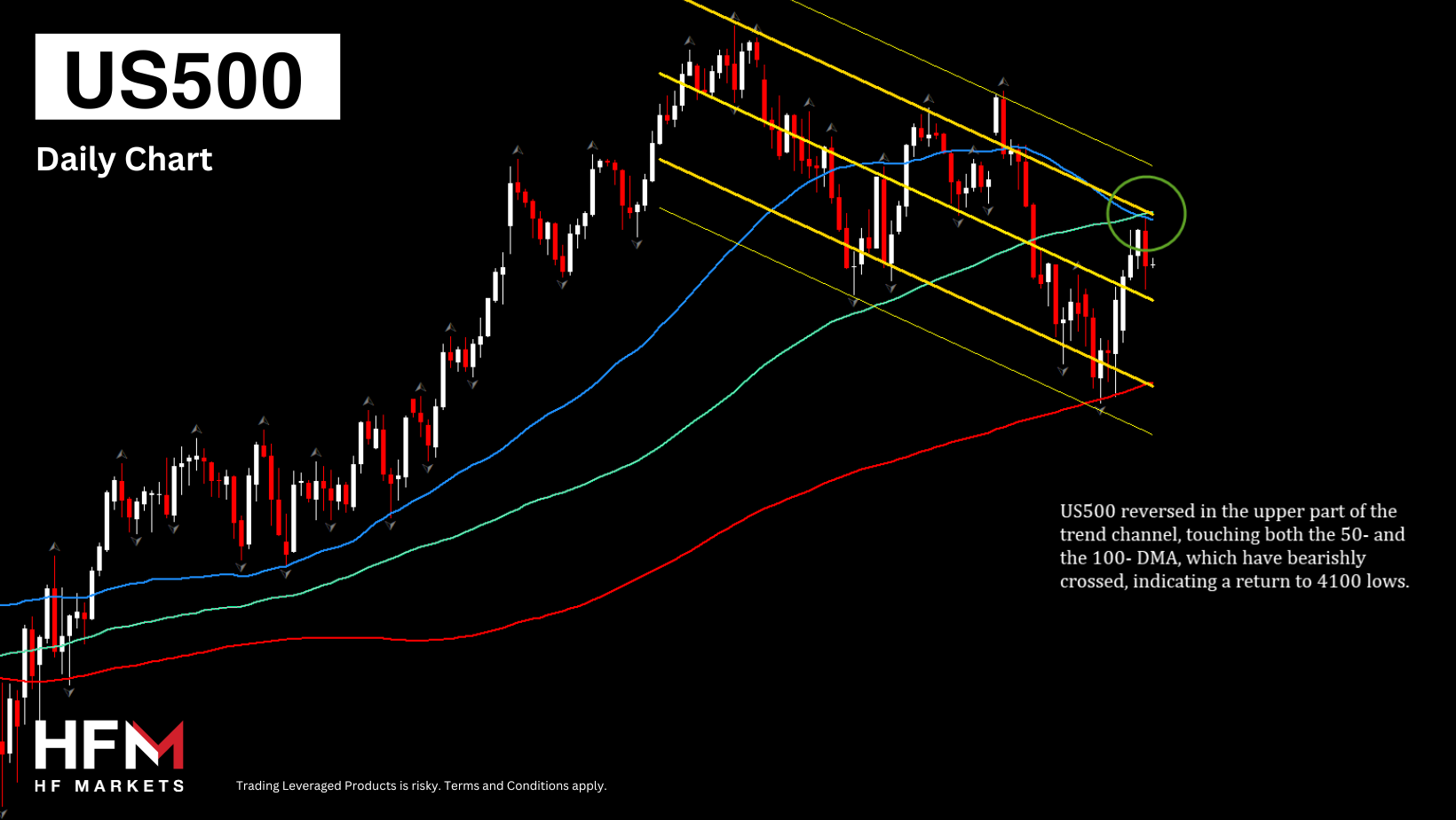

Interesting Mover: US500 (-0.62%) reversed in the upper part of the trend channel, touching both the 50- and the 100- DMA, which have bearishly crossed, indicating a return to 4100 lows.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 16 – Stocks Sideways, Bonds Drift & Middle East in Focus.

Trading Leveraged Products is risky

Stock markets sold off across Asia, with the JPN225 underperforming and losing more than -2%. US futures are higher, as are European futures, as markets watch efforts to prevent a further escalation and widening of the Israel-Hamas conflict. Asian markets were still weighed down by heightened risk aversion, but European and US markets show signs of stabilisation. Treasury yields have backed up 5.8 bp to 4.67% and the 10-year Bund yield jumped 2.6 bp, after JGB rates climbed 1.2 bp as haven flows receded. Eurozone spreads are narrowing.

*USDIndex has declined to 106.54 but is currently on a pull back to 106.20. The Kiwi rose 0.71% to 0.5926.

*The ECB is expected to keep rates steady through the first half of 2024. According to the latest Bloomberg survey, the central bank won’t start cutting rates until the second half of next year, with the first cut seen in September, followed by another in October. Compared to the previous survey respondents have pushed out rate cut expectations, which ties in with recent ECB comments suggesting that the outlook may not become clearer until March.

*Stocks: The UK100 added 0.1%, FRA40 and GER40 both lost 0.1%. US500 and those tracking the tech-heavy US100 both advanced 0.2% ahead of the New York open. Tech stocks led declines in Europe’s Stoxx 600 index after Bloomberg reported that the US is considering further restrictions to curb China’s access to advanced semiconductors. Polish stocks jumped the most since May 2022 and the zloty rallied as a bloc of pro-European opposition parties appeared on track to unseat the nationalist government.

*USOIL steadied within $85.60- $86.75, as the US ratchets up efforts to prevent the crisis from becoming a full-blown, regional conflagration.

*Gold corrected to 1908 (PP), after it climbed 3.17% to $1990, the highest since mid-September as implied Fed funds futures repriced for about a 30% risk of another hike, after spiking briefly to 50/50 after hotter CPI.

Interesting Mover: BTCUSD (+2.11%) jumped to 27957, on USD pullback. Next resistance is at October’s upper swings, 28100 and 28500.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 17 – Could Conflict be Contained?

Trading Leveraged Products is risky

The focus remained on the Middle East and the Israel-Hamas war. Attempts to contain the hostilities and prevent the conflict from escalating throughout the region provided some support for risk appetite to start the week. The VIX slipped to 17.45 after surging to 19.45 to end last week. Fed’s Harker says Fed should not be considering more rate increases. Expectations for more good earnings results also boosted Wall Street, as did some softening in the US Dollar, even as Treasury yields climbed.

New Zealand inflation slowed more than economists expected in Q3, adding to signs that the RBNZ has come to the end of its tightening cycle. The annual inflation rate fell to 5.6%, a 2-year low, from 6% in the second quarter, Statistics New Zealand said Tuesday in Wellington.

*Reduced demand for haven assets – Oil & Treasuries fall as efforts to ease conflict intensify with Biden’s visit in Israel. President Joe Biden will travel to Israel tomorrow, in a visit designed to signal US solidarity with its closest Middle East ally and help prevent the conflict from engulfing the region.

*Final Hours for Country Garden as it is on the brink of a possible offshore default. This could highlight the depth of the confidence crisis gripping the sector.

*USDIndex dipped to 105.95 and GBPUSD failed to cross 1.2200.

*Morgan Stanley’s Michael Wilson: A rally in the USA500 in the fourth quarter of 2023 “is more likely than not”.

*Stocks: Boosted by Fed Harker dovish comments, the AI euphoria and expectations that the FED will not raise interest rates further and speculation of a good earnings season.

*USOIL reversed to $85 and Gold dropped back to $1912 on the back of heightened risk aversion against the background of escalating tensions in the Middle East.

*vBTCUSD settled at 28200. A brief 10% surge in Bitcoin yesterday gave traders a glimpse into the possible impact of a looming the US SEC decision on whether to allow exchange-traded funds investing directly in the token.

*Today: Earnings reports from Goldman Sachs & Bank of America. US Retail Sales and Canadian CPI.

Interesting Mover: GBPAUD (-0.56%) broke 1.9150, which coincides with breakout of ascending triangle and May-June Resistance. This could be a possible Head and Shoulder formation.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.v

Market Update – October 18 – Data Fuels Higher-for-Longer Bets.

Trading Leveraged Products is risky

Asian equities followed US stocks lower after strong retail data. Treasury yields continued to shoot higher, reaching new cycle peaks. Data revived fear of an even higher Fed rate stance for an even longer period of time. Implied Fed funds futures climbed and priced in a 53% chance for a hike by the end of January. However, the market still shows only a small, less than 20% chance, for a move on November 1 since many policymakers have advocated a wait-and-see stance for now. China’s economy grew 4.9% in the third quarter. A largely positive report that confirms that China’s economy has bottomed out, even if the recovery may not be quite as strong as some had hoped.

UK inflation was higher than anticipated, against expectations for a slight deceleration in the annual rate. Core inflation decelerated to 6.1% y/y, the lowest rate since January, but still a tad higher than markets had expected.

*USDIndex has nudged down to 105.75 from a session high of 106.32.

*Stocks: NVIDIA closed at -4.68%, as the US is restricting the sale of chips that Nvidia designed specifically for the Chinese market, part of sweeping new updates to export curbs. Asian semiconductor stocks declined.

*USOIL broke $87 on renewed concerns in Middle East conflict.

*Gold rises to 4-week high, at 1942.70, as Israel-Hamas conflict drives demand for safe-haven assets. Israel’s military has bombarded Gaza with air strikes in anticipation of a widely expected ground invasion against Hamas.

*Today: US Building Permits & FOMC Waller & Harker Speeches.

Interesting Mover: UK100 retests the neckline of a possible inverse head and shoulder formation, at 7715-7740. A breakout could turn attention to the 7800 area.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 19 – Stock markets pressured, as bond yields rise.

Trading Leveraged Products is risky

Stock markets have remained underwater through the Asian part of the session, and European as well as US futures are in the red, as markets eye developments in the Middle East. The Israel-Hamas war continued to shake the markets. The explosion at a Gaza hospital on Tuesday, and the failure of diplomatic efforts to bring all sides together for negotiations, added to the increasingly tense tone and the threat of a widening in the conflict.

Treasury yields have backed up to 4.958% and the 10-year Bund yield is eyeing the 3% mark, as oil prices remain at high levels. The Fed’s Williams said interest rates will have to stay at restrictive levels “for some time” and the higher for longer message, not just from the Fed, but the BoE and ECB as well, is adding to pressure on stocks and bonds.

*USDIndex has lifted to 106.6, the VIX jumped 8.4% to 19.38.

*Stocks: Wall Street was in decline from the open and tumbled sharply into the close. Poor earnings and/or guidance added to the selling. The US100 closed with a -1.62% loss, while the US500 was -1.34% lower, and the US30 off -0.98%. In spite of the risk-off flows, Treasuries failed to benefit due to worries over the strength in the economy keeping inflation elevated. There are also fiscal policy concerns with the massive, and increasing, deficit and debt.

*USOIL prices are off highs, after the US suspended some sanctions on Venezuelan output, but the front end WTI contract is still at $86.80 per barrel, Brent over $91 per barrel.

*Gold rose 1.38% to $1963, as escalating tensions in the Middle East have boosted haven flows today and the precious metal benefited, while Treasuries and EGBs pared losses.

*Today: Fed Powell speech, US Jobless Claims and Philly Fed.

Interesting Mover: EURAUD (+0.60%) breaking downchannel and inverse head and shoulder formation at 1.6650, indicating a potential return to 1.69 highs.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 23 – A suspiciously calm day.

Trading Leveraged Products is risky

Asian markets sold off after a weaker close on Wall Street on Friday. Mainland China bourses underperformed as investors remain dissatisfied with official support measures and the lack of further rate cuts. Futures are under pressure across Europe and the US, amid signs that war jitters are easing as investors watch diplomatic efforts to contain the Israel-Hamas conflict. The 10-year Treasury yield has backed up 5.1 bp to 4.97%, the German 10-year rate is up 2.9 bp and the 10-year JGB yield jumped 2.6 bp. Oil and gold declined this morning driven by concerns regarding the sustained period of elevated interest rates and tensions in the Middle East.

*USDIndex turns below 106, EURUSD extends to 1.0593. The VIX climbed to the highest since March and the banking stresses.

*Stocks: China’s tech gauge drifts to record lows since its inception more than three years ago, worn down by concerns over higher US rates’ impact on global liquidity and a weak export outlook. The US100 plunged -1.53% to 12,983, below 13k for the first time since May. The US30 was off -0.86%. A flight to quality boosted demand for Treasuries, especially after the dovish reading on Chair Powell’s comments.

*Earnings season ramps up this week, with a slew of big tech titans slated to report, i.e. Alphabet, Amazon, Meta and Microsoft.

*USOIL corrected to $86.80 per barrel and Gold recovered to $1981 as risk aversion recedes for now.

*BTCUSD saw its biggest weekly gain since June. Currently at 30540.

Interesting Mover: US500 (-1.53%) to 4236, breaking below the 200-day moving average to add to the sour tone, with immediate support levels at 4200 and 4130.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The sell off in Treasuries abated in the later part of Monday as low prices attracted buyers. Stock markets are also looking somewhat more stable and most Chinese stock gauges improved after the country’s sovereign wealth fund bought exchange traded funds to boost prices. Stock futures are higher across Europe and the US, although the UK100 is struggling. Early data releases in Europe were far from stellar, with German consumer confidence falling again, Eurozone Composite PMI falling to a 35 month low and jobless claims rising in the UK. Bonds have continued to find buyers and the 10-year Treasury yield has corrected a further -5.0 bp to 4.80%, while the 10-year Bund yield is down -5.3 bp at 2.82%, after the 10-year JGB corrected -2.5 bp.

*USDIndex found some ground at 105.46, GBPUSD extended to 1.2287 well above PP and 1.22 lows.

*RBA Governor Michele Bullock: risks inflation would prove more stubborn than expected and that interest rates might have to rise further to bring it to heel.

*Stocks: Chinese stock gauges improved after the country’s sovereign wealth fund bought exchange traded funds to boost prices. Stock futures are slightly higher across Europe and the US, although the UK100 is struggling. The US500 remains though below the 200-day moving average.

*Oil & Gold face some near term selling pressure, as the subsequent drop in rates provide some support for Equities while the USDIndex slumped. The 5% yield level on the 10-year, the first time with that handle since 2007, helped stop the bleeding in the bond market.

Interesting Mover: BTCUSD 12% higher breaching April 2022 highs and 35K. Crypto linked stocks followed as well, as speculation about the possibility of a bitcoin ETF approval drove enthusiasm.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 25 – Stocks in Red; Dollar recovers.

Trading Leveraged Products is risky

Investors cheered the approval of a trillion-yuan sovereign issue as a harbinger of stimulus, while the Chinese government unveiled new support plans that include issuing additional sovereign debt and lifting the budget deficit ratio to finance fresh measures. Hong Kong reversed a pandemic-increase in stock trade levies and Chief Executive John Lee also announced a plan to halve taxes on home purchases for residents as well as non-residents. That helped to boost property stocks, even as troubled Chinese developer Country Garden Holdings Co. was deemed to be in default on a dollar bond for the first time.

*Stock markets got a boost from fresh stimulus measures for China. The Hang Seng has pared some of its early gains, but is still up 1.0%, while the CSI300 has lifted 0.6% and the JPN225 0.7%.

*European stocks: In the red today weighed by a flurry of bank results and a mixed batch of US Big Tech earnings ahead of the ECB decision tomorrow.

*Microsoft, Alphabet, and Visa reported their earnings, which indicated strong performance with revenue and net income growth in their respective quarters.

*Alphabet (-6% in after-hours) sales beat damped by cloud computing miss.

*Microsoft’s (+4% in after-hours) unexpected rebound in Azure cloud growth lifted shares.

*Snap Inc. also reported revenue growth but experienced operating and net losses in the same period.

*Santander net profit rose 20% on record-high interest rates.

FED: PMIs kept a Fed rate hike through the January 31 FOMC decision on the table with a 40% probability.

*USDIndex: returned above 106, but held sideways.

*AUDUSD: Aussie Dollar jumped after hotter-than-expected inflation lifted rate hike forecasts for the RBA next month, which would come after four rate pauses.

*USOIL steadied today at key 4-month support trendline after a 3-day sharp decline, amid signs that the Israel-Hamas war will remain contained for the time being at least. $83 is a key hurdle, which could indicate a move to $80.

*Gold holds gains above $1970.

*Bitcoin is up 15% this week amid speculation that ETF applications from BlackRock and others will succeed and drive capital into the asset class.

*Today: Germany IFO business climate, BOC rate decision, US new home sales and IBM, Meta earnings.

Interesting Mover: USDCAD broken the descending trendline from the draw tops of 1.3977 and 1.3861.

Stocks and bonds were routed midweek. Tech shares were slammed after poor earnings news from Alphabet knocked its shares down nearly -10%, spreading gloom across the sector. A surge in Treasury yields added to the selloff. Meanwhile, ongoing signs of the strength in the economy after a pop in new home sales did not help. Instead, it added to expectations that a big jump in GDP on Thursday will keep a Fed rate hike in the picture later in the year or early 2024. That and fears over other big headwinds ahead added to a negative feedback loop that growth will slow sharply next year, further hurting investor sentiment.

*Stock markets: The US100 crashed -2.43%, its worst slide since February. The US500 lost -1.43%, falling below the key 4200 level. The US30 slid -0.32%. The JPN225 underperformed and corrected -2.1, amid disappointing big tech earnings.

*Futures are lower across Europe and the US as markets wait for key central bank decisions, with the ECB kicking things off today.

*Alphabet shares logged their worst session since March 2020 overnight, dropping 9.5% as investors were disappointed with stalling growth in its cloud division.

*META fell 4% on Wednesday and another 3% in after-hours trade after publishing results showing better-than-expected revenue but a cloudy outlook, with expenses seen topping Wall Street estimates.

*USDJPY has broken back above the 150.00 mark, hitting 150.80 (highest since October) after finding courage to test the MoF again. The combination of expectations for more evidence of the strong US economy, including GDP, and the potential for another rate hike from the FOMC, are boosting the buck versus JPY, especially with still-fragile Japanese growth, along with rising expectations the BoJ will maintain its uber accommodative stance at its policy meeting next week.

*USDCAD rose to a high of 1.381 after the BOC’s announcement, the highest since early March and the SVB bank failure.

*USOIL recovered to $85 after a fall due to a rise in US crude stockpiles and a climb in US Dollar.

*Gold retests week’s resistance at $1988.

*Today: ECB meeting, US Durable Goods and Advanced GDP.

Interesting Mover: USDIndex got legs after the BoC left policy unchanged and downgraded its GDP forecasts.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!