Oil Hits Lowest Levels Since June 2023, Moody Downward China.

Crude Oil – Oil Declines for a Seventh Consecutive Week

The price of Crude Oil has declined to its lowest level since June 2023, marking an almost six-month low. The price of Oil has now declined for a seventh consecutive week. Economists note the decline is also improving the prospects of the stock market. Stocks are taking advantage of the lower oil prices which may trigger lower inflation and a softer monetary policy. This week alone the price has declined by 6.5%, but what is driving the bearish trend?

The main two reasons the market is witnessing a lack of demand in the oil market is China’s latest poor economic data and the latest OPEC meeting. China’s manufacturing and services PMI read significantly lower than expectations and this week Japan also announced weaker data. China is the largest importer of Oil while Japan is the fourth largest. Therefore, poor economic data in these regions are likely to trigger downward pressure for Crude Oil.

To make matters worse for the Oil market, Moody, the credit rating industry, lowered the economic outlook for China from “stable” to “negative”. Since the downgrade, economists have advised the Chinese economy is not likely to witness a recession, but more likely stagnation. OPEC, on the other hand, were unable to come to an agreement on the production levels. Again, this had a negative effect on Crude Oil prices. Lastly, yesterday’s report from the American Petroleum Institute showed inventories rose by 9.594M barrels instead of a decline of 2.267M barrels. The inventories show higher than expected supply.

In terms of technical analysis, the price of Oil is trading within a downward trend and is currently hovering within a retracement. The retracement is currently measuring 1% in line with previous pullbacks and is currently showing no major upward momentum. Therefore, most indicators continue to signal a downward trend. If the price breaks below $69.69 and $69.59, sell signals will again potentially become active.

USA100 – Only 20% of Stocks Held onto Gains!

The USA100 fell by 0.57% during yesterday’s session and was the weakest of the top 3 most popular US indices. When looking at the NASADAQ’s top ten most influential stocks, only 1 stock stayed in the “green”, this was Tesla which only slightly rose by 0.27%. Out of the top 20 most influential stocks, only 20% retained their value. The stock which saw the largest decline was NVIDIA which dropped 2.28%.

However, fundamental factors continue to point towards a positive outlook for the US tech sector. This morning the US Dollar Index is declining, 52% of market participants believe the Fed will cut rates in March 2024 and most of the components witnessed positive earnings data. The only slight concern for investors is bond yields which have risen over the past 24 hours. However, bond yields continue to remain significantly lower than in the previous months, which is positive for the stock market.

Technical analysts have pointed out that the index is not within a short-term downward trend and each time the USA100 declines, buyers re-enter the following day to take advantage of the lower price. Investors will again be monitoring if the index rebounds today. The stronger performer in the pre-market hours is Alphabet which has risen 0.82%. Alphabet stocks make up almost 6% of the overall index. Investors are currently balancing the negative effect of a weaker Chinese economy and the positive effect of a rate cut as early as March 2024. If the price increases above $15,873, the USA100 will again experience buy signals. Buy signals can be seen from the regression channel and crossovers.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Central Banks’ Divergent Paths: ECB Signals Caution, BoE Stays the Course

Trading Leveraged Products is risky

As the European Central Bank (ECB) and the Bank of England (BoE) gear up for their upcoming meetings, market participants eagerly await signals that will shape the economic landscape in 2024. While both banks are expected to maintain interest rates, their perspectives on future policy directions diverge.

This article explores the nuanced positions of the ECB and BoE, shedding light on their contrasting views on inflation, rate hikes, and the path forward.

ECB’s Shifting Stance:

The ECB meeting is poised to capture attention not for an anticipated rate adjustment but for the nuanced signals regarding the outlook for 2024. In the aftermath of November’s meeting, where a tightening bias persisted, recent developments, notably the unexpected drop in inflation, have prompted a shift in tone.

Market Trends

Isabel Schnabel’s Reuters Interview:

Executive Board member Isabel Schnabel’s recent Reuters interview marked a departure from previous sentiments. While she emphasized the need for caution, Schnabel hinted that the ECB is prepared to confirm that interest rates have peaked. Contrary to market optimism anticipating rate cuts as early as March, Schnabel underscored the central bank’s patience, emphasizing the necessity of further progress in underlying inflation.

Monetary Policy Transmission Confidence:

Despite concerns about a potential credit crunch, Schnabel expressed confidence in the effectiveness of monetary policy transmission. While acknowledging signs of labor market softening, she dismissed fears of a severe and prolonged recession, aligning with the ECB’s cautious stance. The central bank seems poised to confirm the unlikelihood of further rate hikes but remains hesitant to entertain the idea of rate cuts in the near term.

Financial Markets Performance:

ECB’s Path to Rate Cuts:

The timing of potential rate cuts in 2024 remains a pivotal question. Market expectations for an easing bias in March, paving the way for a second-quarter cut, appear optimistic. ECB President Lagarde, expected to be more vague on the topic, may find it challenging to temper easing expectations.

PEPP Reinvestment Discussion: The discussion around the future of the Pandemic Emergency Purchase Program (PEPP) reinvestments adds complexity. While some suggest an early end to re-investments as a prerequisite for rate cuts, details may not emerge until early 2024. Lagarde’s confirmation of a gradual reduction could set the stage for rate cuts in the second quarter.

EURUSD has been under pressure since the lower than anticipated inflation report last week and is currently struggling to hold the 1.08 mark. The Fed may be leading the way on rate cuts next year, but markets expect that the ECB won’t be far behind. The US economy may be better equipped to deal with the marked tightening of financing conditions that is increasingly hitting the real economy.

BoE’s Steady Outlook: In contrast, the BoE’s upcoming announcement may lack the excitement of policy shifts. With no updated forecasts and data aligning with November’s assumptions, the focus turns to the hawks within the bank. Despite concerns voiced by some, including BoE’s Greene, about the risks of doing too little, Governor Bailey maintains a steadfast position against early rate cuts.

Bailey’s Commitment to Inflation Target: Bailey’s emphasis on completing the journey to the 2% inflation target and the potential sluggishness of that process reinforces the BoE’s commitment to a “higher for longer” approach. Deputy Governor Ramsden underscores the need for sustained restrictive policy to combat inflation effectively, signaling a likelihood of the BoE remaining on hold through the first half of 2024.

As the ECB signals caution and the BoE maintains a steady course, the central banks’ divergent paths reveal nuanced approaches to economic challenges.

Investors will closely monitor the upcoming meetings for insights into future policies, with the timing of potential rate cuts and the fate of PEPP reinvestments hanging in the balance. The evolving economic landscape will undoubtedly shape the trajectory of monetary policies in the months to come.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

US Economy Remains Strong, But All Eyes on Tomorrow’s Inflation!

Trading Leveraged Products is risky

December has not failed to surprise investors with the US employment sector outperforming expectations and sending stocks soaring. Additionally, across the Pacific the World’s second largest economy also made public interesting inflation data which is in the spotlight just as much as the US NFP. Both Chinese Consumer and Producer inflation fell below expectations. Consumer prices declined at their fastest pace in more than 3 years. China is now witnessing deflation measuring -0.5% which has not been seen since the banking crisis if we exclude COVID-19.

Last week, Moody’s downgraded China’s credit rating. Moody’s advises the costs of supporting failing local governments, state-owned companies and controlling the property crisis would pressure the economy. But the question is, what does this mean for the US and US Indices?

USA100 – Inflation To Be The Next Price Driver

The USA100 rose during the US trading session by 0.40% on Friday and by the close of day was almost 0.50% higher. The first reaction to the Non-Farm-Payroll data was negative and the instrument fell 0.38% before buyers re-entered the market. During this morning’s Asian session, the index is trading 0.10% lower but is so far forming nothing more than a retracement. Let’s discuss what the employment data means for the index as well as weak Chinese inflation.

The NFP confirms the US has 199,000 more employed individuals compared to the previous month, which is 15,000 higher than expected. However, the main shocks came from the Average Hourly Earnings and the Unemployment Rate. The Unemployment Rate declined from 3.9% to 3.7% which is considerably low considering the restrictive monetary policy. The Hourly Earnings doubled from 0.2% to 0.4%. The employment data has both positives and negatives for the stock market. However, in the past 2 years, higher employment data has meant a poorer stock market, which was not the case on Friday.

The better-than-expected employment data indicates an imbalance within the employment sector which triggered higher wages. These factors can contribute to higher consumer demand, higher investor demand, and a better performing economy. All these factors are positive for the stock market in general. However, there is a negative side also. The positive data has lowered the possibility of a nearer interest rate cut. Previously, market participants predicted a “cut” to come as early as March, but the employment data again points to “higher for longer”. The CME FedWatch Tool now has virtually no possibility of a cut in December, January and February, and now indicates a “pivot” in May 2024.

The question is, is the USA100 overpriced considering the new reality? This is something which will become clearer during Wednesday evening’s Federal Reserve Rate Decision and Press Conference. If the Fed President, Jerome Powell, suddenly becomes more hawkish and pushes a pivot further in the future, stocks can correct. Technical analysts also advise the stock market may fall into a wider price range until further clarity from the Fed.

Technical analysis shows the USA100 trading within a short-term bullish trend, but also at a significant psychological price. The asset has failed to break above this level on the past four attempts as investors fear the asset is trading above its intrinsic price. Therefore, the USA100 will require a stronger price driver. This potentially could come from tomorrow’s Consumer Price Index (inflation rate). If the CPI reads lower than 3.1%, ideally 2.9% or lower, the index could experience another surge in investor demand. However, if inflation reads 3.1% or remains at 3.2%, investors may be discouraged.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Global Stocks Rise Ahead of Today’s US Inflation Announcement!

Trading Leveraged Products is risky

The USA100 is increasing in value for a seventh consecutive week and continues to renew its highs for 2023! The USA100 is only 0.65% lower from fully regaining all of the “lost ground” from 2022. The asset saw a sharp decline after the Ukraine-Russia conflict and the largest rate hiking cycle seen since 2004. However, all eyes are on today’s US inflation and tomorrow’s Central Bank press conference. Therefore, analysts do not expect volatility to cool off any time soon!

USA100

From the 100 stocks in the USA100, only 11 ended the day lower, while 89 stocks were in the green throughout the day. Broadcom, which is the seventh most influential stock, witnessed the largest gain, increasing by 9.00%. Broadcom continues to be one of the best performing stocks due to the latest company earnings which beat expectations. Additionally, the stock is supported by the company advising revenue from AI would double to $8 billion in 2024. The board of directors also advised the growth in AI would counterbalance the current challenges in the semiconductor market.

However, even though the majority of stocks within the USA100 rose in value on Monday, the top five most influential stocks declined. This includes Apple, Microsoft, Alphabet, Amazon, and NVIDIA. Of these stocks, the stocks which saw the largest decline was NVIDIA, dropping 1.85%. However, investors should note that Asian and European stocks are higher this morning, which continues to point to positive investor sentiment towards the asset class.

Today’s price movement will largely depend on the US inflation data. On Monday, investors priced in a weaker than expected Consumer Price Index. This is most probably due to deflation in China and lower producer prices which can also influence global inflation. This is due to the nature of the Chinese economy. For the USA100 to potentially continue its upward trend to previous highs, the CPI will need to read 3.00%. However, to see a stronger trend, investors will need clarity that a rate cut is likely by March 2024. For such an outcome, market participants may need to see a sharper decline in inflation such as a decline from 3.2% to 2.9%.

USDCHF

The USDCHF is trading higher since the opening of the European session, but remains lower than the open price. The Dollar Index is trading 0.22% lower and bond yields are 0.044% lower, which indicates the USDCHF may also come under further pressure. However, the price of the Dollar will largely be determined by today’s consumer inflation. In addition to this, tomorrow’s producer inflation and the Fed’s press conference will also create volatility.

The US Federal Reserve meeting will take place on Wednesday, and now, analysts are almost confident that the current interest rate will remain at 5.50%. However, investors and market participants continue to price in an earlier “pivot”. The central bank may again point out the possibility of maintaining high borrowing costs for a long time. Experts have revised their forecasts regarding the timing of an interest rate cut and are predicting May 2024, although previously, most estimated easing would begin in the first quarter.

Representatives of the Swiss National Bank will be convening a meeting on Thursday, and traders expect interest rates to remain at 1.70%. The head of the SNB, Mr Jordan, may indicate abandoning further tightening of monetary conditions which may pressure the Swiss Franc.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The UK Economy Unexpectedly Contracts! US Inflation Remains Stubborn.

Trading Leveraged Products is risky

The USA100 continues to be the best performing index, increasing by 0.90% and more than 50% in 2023 in total. The main price driver was the US inflation data which more or less read as per expectations. The US inflation rate has declined from 3.2% to 3.1% but the core inflation rate remains stubbornly high. Core Inflation has remained at 4.00% for a second consecutive month. According to analysts, inflation is not low enough to prompt a pivot in the first quarter of 2024. However, investors are increasing exposure to the stock market as a “soft landing” becomes more likely.

US30 Remains in the “Trend Zone” of Technical Analysis!

Even though the best-performing asset by far is the USA100, the asset experiencing the best performance in terms of components is the US30. The USA100 saw 68% of its stocks increase in value whereas 73% of the US30 appreciated. Investors should also note that of the top 20 influential assets within the US30, only 1 stock declined. Chevron fell by 1.28%, and the best performing stock was Salesforce, rising 1.73%. In comparison, of the top 20 influential stocks within the USA100, 5 stocks declined.

As mentioned above, inflation read as most analysts were expecting, however it did not show any real signs of easing significantly over the next 2-3 months. The Federal Reserve policy makers will be able to discuss monetary policy issues tonight at 18:00 GMT. Journalists will without doubt ask Chairman Jerome Powell if he believes interest rates will be cut in the first half of the year. Without a dovish tone or a clear indication of a cut, the stock market may struggle to maintain momentum. However, most buyers are now investing, not due to a dovish policy, but due to the resilient economy and the likelihood of a soft landing.

One of the few stocks within the Dow Jones which have struggled is Procter and Gamble (holds a weight of 2.64%). Analysts expect the company’s revenue and earnings per share to remain stable, but shareholders have taken badly to the company decision to withdraw from certain countries where the Dollar is now too expensive. For example, the products will be withdrawn from Nigeria and Argentina. Furthermore, Berkshire Hathaway has also advised they have recently sold their shares in the company. Warren Buffet explained that the consumer goods market is recovering too slowly after the pandemic.

In terms of Technical Analysis, the price of the US30 is forming a downward facing retracement but is not showing any signs of strong momentum. Due to the weak momentum, and also bullish impulse waves forming, the instrument continues to remain in bullish territory. The price also continues to trade within the upper side of the Bollinger Bands and Regression Channels, again indicating bullish price movement. However, some traders may be concerned about the high price. These individuals may wait for a lower price or a larger retracement before speculating an increase.

The price throughout the day will be influenced by the Producer Price Index, which looks at inflation at the producer level. If the PPI reads lower than expected (0.2%), the Dow Jones could obtain short-term support. However, the main event will be tonight’s Federal Reserve Press Conference.

GBPUSD – The UK Economy Unexpectedly Contracts!

The price of the GBPUSD came under pressure this morning from the UK’s latest Gross Domestic Product. The UK’s GDP was expected to decline from 0.2% to -0.1%. However, the figure fell to -0.3%, the lowest since September 2023, sparking some doubt as to whether the BoE can hold rates “higher for longer”.

November’s poor GDP figures will not be enough to worry the Bank of England, however, December and January’s GDP figure will now become more vital! If next month’s data also disappoints, investors may start to price in a weaker monetary policy.

The US Dollar Index this morning is slightly higher but has not crossed above yesterday’s highs. However, the Pound is declining against all its main competitors. If the US Producer Price Index reads higher than expected, the Dollar could receive some much-needed support. In this case, the GBPUSD may decline further and break below the support level at 1.25130. In terms of technical analysis, the GBPUSD is trading below the 75-bar exponential moving average and at 42.00% on the RSI. Both indicate sellers are controlling the price movement and a downward trend remains a possibility.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Fed Expect Interest Rates to Fall to 4.60% in 2024, Buyers Pounce!

*Fed Expects Interest Rates to Fall to 4.60% in 2024, Buyers Pounce!

*The Federal Reserve gives its first clear signal that rates will be cut in 2024!

*Analysts expect the Federal Fund Rate to decline to 4.50%.

*The USA100 is close to breaking its all-time highs after rising a further 1.65% since the Fed’s rate decision.

*The Dollar declined to a 19-week low against the Japanese Yen.

USA100 Close to Reaching All-Time Highs!

The USA100 rose in value for a sixth consecutive day and if the volatility levels continue, the asset will be on track to complete its strongest week of the year. Investors heavily exposed their portfolios to the US stock market and particularly the tech sector. Investors show a clear “risk-on” appetite which can also be seen in bond yields which again collapsed. In addition to this, other safe haven assets, such as the Dollar, fell a whole 1%. The cheaper Dollar and lower bond yields are likely to support the US stock market if they follow the market’s traditional “domino effect”.

The Fed President speech made it clear that the monetary policy will be set to ensure employment remains high and that prices remain stable. The president stressed the importance of keeping inflation stable and not necessarily applying further downward pressure. The press conference reassured many investors and improved investor sentiment. The Federal Open Market Committee’s new forecast points to interest rates declining to 4.60% in 2024, 3.60% in 2025 and 2.90% in 2026. As a result, the cost of debt will decline and consumer demand may rise, supporting companies within the USA100.

In addition to the Fed’s forward guidance, the latest Producer Price Index is also supporting stocks. Producer inflation read 0.00%, which is lower than the previous 0.2% expectation. As a result, investors continue to predict that inflation will remain controlled and potentially decline further in the next 2 months. For inflation to remain stable, investors will also be monitoring oil prices aiming for crude oil to mainly trade below $70 per barrel.

In terms of technical analysis, the price of the USA100 remains within the bullish trend zone of the regression channel. In addition to this, the price trades above the price sentiment line and the trend-based moving average. For this reason, technical analysis indicates an upward trend going forward similar to fundamental analysis. However, most Oscillators indicate the price is “overbought”. Therefore, it is important to consider the appropriate price to speculate the upward price movement.

Lastly, the monetary policy of the Swiss National Bank, European Central Bank and Bank of England will influence the USA100. Buyers and bulls will ideally be hoping for a similar dovish tone. In addition to this, investors will be hoping for higher-than-expected US Retail Sales.

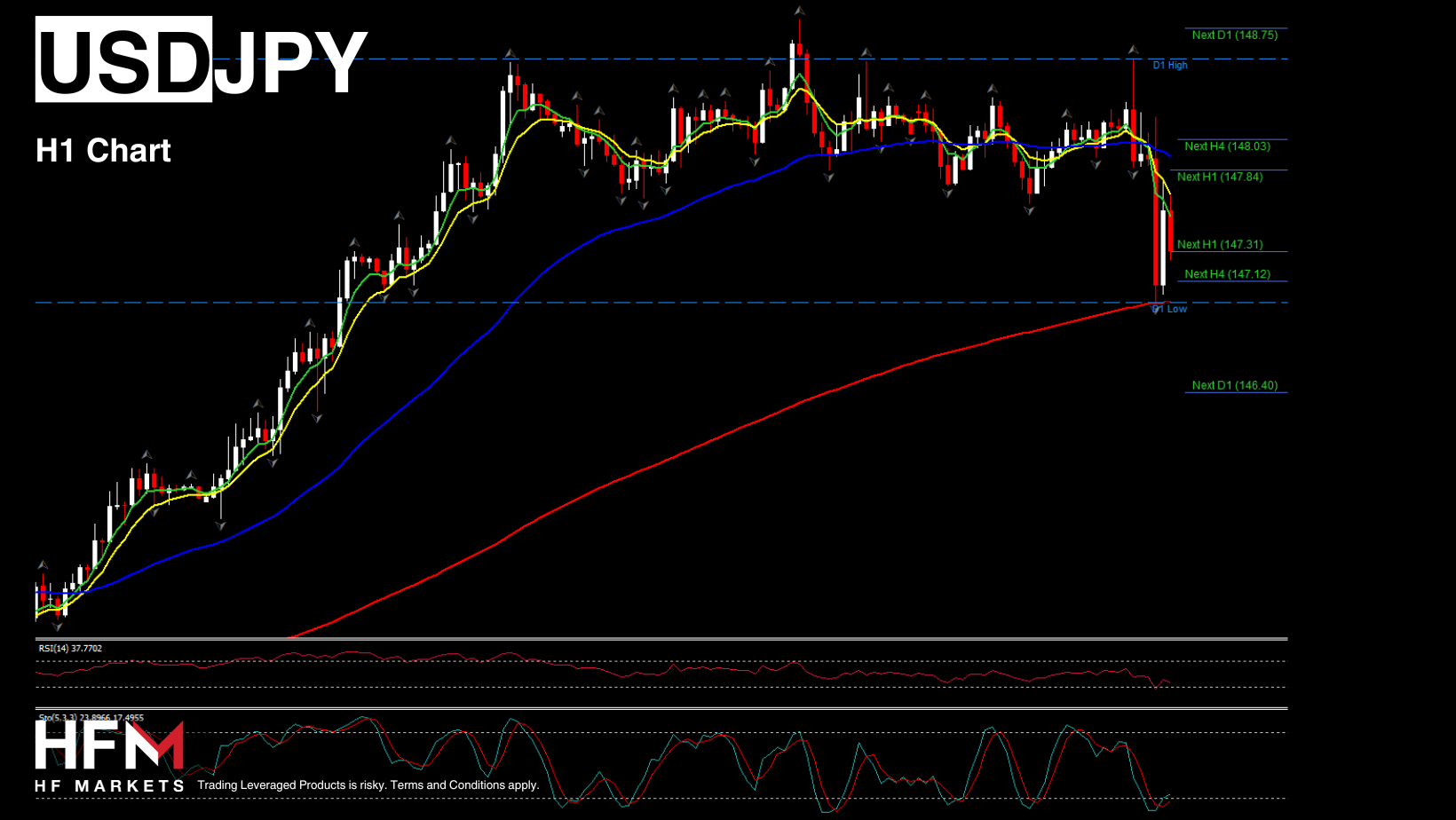

USDJPY – Japanese Yen Takes Advantage of Dollar Weakness

Investors looking to avoid “news risk” may look to the Japanese Yen which is not expecting any major news during this morning’s European and Asian session. The Japanese Yen is increasing in value against all major currencies including the US Dollar, Euro and Pound during this morning’s session. The exchange rate has also declined for three consecutive days and the Dollar Index is trading 0.19% lower this morning.

This week, Japan has released various data regarding the economy and confidence which have read stronger than expected. Thus, the confidence of national business has almost reached two-year highs, which, according to experts, confirms the stability of the country’s economy in the context of the global crisis and gives the regulator grounds to reduce incentives and move to a tighter monetary policy.

The USDJPY is not oversold, similar to other currency pairs, which still gives an opportunity for traders to speculate. Sell signals are likely to arise from technical analysis if the price declines below 141.285.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Recap: Focal BoJ ahead & the very last key US data

Markets are starting to wind down for the year. The four major central bank, the FOMC, ECB, BoE, and SNB all left policy rates unchanged, and most dialed back their hawkish biases. But while officials tried to jawbone and push back that early rate cuts are not on the table, the markets quickly equated the steady stance and shift in bias to pricing in rate cuts sooner than later. Indeed the markets ran with expectations for easing as soon as the first half of the year, if not March for the FOMC.

Economic Indicators & Central Banks:

*FED: Fed’s Bostic sees two 25 bp cuts in 2024, but said it’s not an “imminent thing,” in a Reuters interview. New York Fed President Williams said its too early to begin thinking about cuts. Still, U.S. futures are already finding buyers again after a mixed close on Wall Street Friday.

*Japan: The BoJ is the focal point this week as it’s the last major bank to meet. Risks for no action have picked up as data have failed to give Governor Ueda the confidence needed to exit negative rates or YCC at this point.

*China’s PBOC resumes 14-day cash injections. The move likely designed to smooth liquidity conditions over the year-end. Borrowing costs were held unchanged at 1.8% and 1.95% respectively.

Market Trends:

*Treasury yields slightly higher however the 2-year still closed the week with 28 bp drop, marking the lowest closing since mid-May. The 10-year notes stood at 3.91%.

*Asian stock markets declined, and European futures are also in the red, after Fed comments on Friday tried to push back against excessive rate cut speculation.

*Stocks: The JPN225 slumped 0.7% on weakness in Yen. The US500 futures inched up 0.3%, while US100 added 0.2%, EU50 futures slipped 0.3% and UK100 at 0.1%.

Financial Markets Performance:

*The USDIndex at 102.00 after drifting to 101.43.

*EURUSD corrected to 1.0920 after a solid weekly gain If Eurozone activity fails to stabilize, Lagarde will be under pressure to change her tune and prepare for rate cuts earlier rather than later.

*GBPUSD moves sideways today and is at 1.2685, while USDJPY corrected again and is trading at 142.55 (38.2% Fib from 2023 upleg).

*Gold turned above $2000 as drop in the US dollar, yields and the Fed’s dovish pivot have helped to boost demand for the precious metal.

*Oil steadied above $72 after 5-month low last week amid worries supply will continue to outstrip demand. The weaker USD and dovish Fed comments helped to boost sentiment. The IEA said in its monthly report that it expects global oil consumption to rise by 1.1 million barrels a day in 2024, which means it has revised its demand forecast higher. That added further support and helped oil prices to at least stabilize over the second half of this week. Lower exports from Russia and attacks by the Houthis on ships in the Red Sea offered some support as well.

*Bitcoin holds above 40K for 11 day’s in a row, with increasing bullish bias.

*Key Mover: Goldman has raised year-end 2024 S&P 500 index target from 4700 to 5100, representing 8% upside from the current level. Decelerating inflation and Fed easing will keep real yields low and support a P/E multiple >19x.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Редактировалось: 1 раз (Последний: 18 декабря 2023 в 12:32)

*Data in the US included stronger than expected construction spending and weaker than forecast S&P Global manufacturing PMI.

*Fed funds futures have slipped to kick off 2024 as some of the aggressive rate cut bets are trimmed. However, the market is still pricing in close to 6 quarter point cuts. No action is expected for the first FOMC meeting on January 31.

Market Trends:

*Treasuries and Wall Street opened 2024 in the red and it basically went downhill from there. Treasury yields climbed 5- to 8- bps, led by the front end.

*A heavy corporate calendar exacerbated the losses from spillover from losses in European bonds, profit taking on the late 2023 rally, and from trimming of Fed rate cut bets.

*Stocks: The US100 dropped -1.63% paring some losses as the indexes finished off their lows. The US500 was -0.57% in the red, while the US30 was fractionally higher.

*Moderna shares surged 15.5% after investment bank Oppenheimer upgraded its stock.

*Apple lost 3.6%, its worst day in 5 months after Barclays downgraded its shares, Nvidia and Meta Platforms both fell more than 2%. Lack of new features and Iphone upgrades affected Apple stocks.

Financial Markets Performance:

*The USDIndexretested 102. The buck is on course for a 3rd straight daily rise, with technical factors as well as risk aversion likely to add support.

*EURUSD has dropped sharply to 1.0937 and GBPUSD dropped to 1.2610. USDJPY nudged up to 142.43 in thin trade, as Japanese markets remain closed.

*Gold declined to $2058 from the $2062.98 close on December 29. Global risks and the weaker US Dollar supported gold prices into year-end and an all-time closing high of $2077.49 on December 27.

*Bitcoin extended above 45K supported by statements that Blackrock & JPMorgan anticipate an imminent spot Bitcoin ETF approval and Goldman Sachs issuing huge 2024 Crypto Prediction.

*Today: Germany unemployment, US FOMC minutes, ISM Manufacturing and US Job openings.

*Key Mover: Oil prices slumped to $70.30 after an intraday peak of $73.64 amid concerns over events on the Red Sea. The escalating tensions in the Middle East are fueling concern that supply may be disrupted.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*The Fed’s minutes to the December 12-13 meeting showed some pushback against imminent easing, while still acknowledging the rate cuts penciled in with the dots. The report showed “all” participants said clear progress had been made toward the inflation goal. Rates had likely peaked.

*“Several” thought the policy rate could remain restrictive for some time and peak rates could last longer than expected. Fed’s Barkin said there is still potential for additional rate hikes.

*China services index posted fastest expansion in 5 months amid optimism. Chinese wages in major cities declined by the most on record.

*Japanese manufacturing activity shrank by the most in 10 months in December, as demand ebbed in Asia’s largest advanced economy.

Market Trends:

*Wall Street extended its 2024 declines with weakness in tech shares weighing. The US100 (NASDAQ) slumped -1.18%, dropping for a 4th straight session, with the US500 (S&P500) falling -0.80%, while the US30 (DOW) was off -0.76%.

*JPN225 (Nikkei) dropped the most in two weeks, after the Fed minutes, also due to the powerful earthquake in the northwest on New Year’s Day and the runway collision between turboprop aircraft and Japan Airlines jet, which dragged down some companies.

*ASX fell 0.53% to trade near 7,495. Hopes that the RBA will no longer be raising rates have been partly driven by the Fed’s dovish shift.

*Chinese stocks remained the biggest drag in Asia following the jobs report – CSI 300 down by 0.9% after having slid as much as 1.6%.

Financial Markets Performance:

*The USDIndex rallied from a session low of 102.07 to a peak of 102.40 before dipping to 102. Markets reassessed their expectations of the scale of rate cuts by the Fed this year.

*USDJPY regained ground up to 143.89 as the Japan market reopened.

*Gold slid to $2030 per ounce, in part hurt by the FOMC minutes, with the firmer US Dollar weighing too.

*Bitcoin steadied above 42500 after diving to 40K territory as $400M was liquidated in 2 hours, as Matrixport rebuffed optimistic reports!

*Key Mover: Crude oil perked up and climbed 3.65% to $72.95 per barrel as a shutdown at a Libyan oil field added to the concerns over Mid East tensions and supply. Currently traded above $73. Libya’s major Sharara oilfield, with a capacity of 300,000 bpd, completely shuts down due to protests.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*The focus now shifts to the jobs report. Recent data, including jobless claims and the employment components of the ISMs, continue to reflect a decent labor market even as conditions cool. We expect a 140k increase in nonfarm payrolls following gains of 199k in November, 150k in October, and 262k in September.

*Yields remain elevated and near session highs after firmer than expected employment data. The claims and ADP numbers added to the losses along with the rethink of Fed easing bets and spillover from European bonds after a stronger than expected inflation report.

*A heavy corporate issuance calendar exacerbated the selloff too.

Market Trends:

*Treasuries continued to stumble in the new year. A rethink of aggressive rate hike bets, better than expected data, profit taking, and supply have all conspired to cheapen yields across the board in the first week of 2024 trading.

*Wall Street finished mixed with the US100 falling -0.56%. The US500 was -0.34% lower, posting a 4th straight decline. The US30 inched up 0.03%.

Financial Markets Performance:

*The USDIndex was choppy but ended marginally lower at 102.41, though inside the 102.15 to 102.52 range. It has held over 102 for a 3rd consecutive session.

*USDJPY rallied above 145. Yen has weakened amid speculation that the BOJ might go slowly on changing its lax policy stance as it assesses the impact of Monday’s major earthquake in central Japan.

*USOIL prices have increased 1.13% to $73.52 per barrel.

*Gold is fractionally lower at $2041 per ounce.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Bond Yields Rise Triggering Fear of Further Stock Weakness.

The US Non-Farm Payroll figures for December rose from 199,000 to 216,000 and beat expectations of 168,000. The Unemployment Rate unexpectedly remained low at 3.7% instead of rising to 3.8%. However, the real shock came from the Average Hourly Earnings rising for a second consecutive month. So, how did the trading markets react and how are they reacting this morning?

XAUUSD – Technical Analysis Points to Potential Sell Signals

The price of Gold along with other Dollar-correlated assets at first benefited from the stronger than expected employment data. The price of Gold rose 1.31% and also formed a 0.34% bullish price gap. However, the asset struggled at the previous price range and quickly gave up gains. This morning the price of Gold is declining 0.70% which is considerably high for the Asian session and continues to maintain a sell signal on the 2-Hour Chart. The price is trading below the 75-bar average price and below the neutral on the Relative Strength Index. In addition to this, on the 5-Minute Chart the price is also forming a bearish crossover. All the above indicate a potential downward price movement and are likely to strengthen if the price declines below $2,029.00.

The US Dollar Index this during this morning’s Asian session is trading at the day’s open price, however, volatility is likely to strongly influence Gold. However, US Bond Yields are considerably higher this morning which potentially could support the Dollar throughout the day. If the Dollar Index and Bond Yields rise, the price of Gold has a higher possibility of witnessing bearish price movement.

USA100 – Bond Yields Rise Ahead of US CPI

*Treasuries continued to stumble in the new year. A rethink of aggressive rate hike bets, better than expected data, profit taking, and supply have all conspired to cheapen yields across the board in the first week of 2024 trading.

*Wall Street finished mixed with the US100 falling -0.56%. The US500 was -0.34% lower, posting a 4th straight decline. The US30 inched up 0.03%.

Financial Markets Performance:

The USA100 rose by 1.20% after the release of the US employment data and bullish volatility rose with strong momentum. According to order flow analysts, the upward price movement was partially triggered by the quick decline in entering pending orders. Investors were clearly looking to take advantage of the lower entry point. However, in addition to this, the employment data clearly indicates the strength of the employment sector, the economy and the ability to cope with higher interest rates. As a result, investor sentiment rose and was less concerned about the restrictive monetary policy.

However, the positive data also means the Federal Reserve is unlikely to feel the need to lower the Federal Fund Rate to support the economy. According to JPMorgan, the possibilities of an interest rate cut in March are now relatively low. Though the CM FedWatch Tool continues to indicate a strong possibility of a small cut in March. Therefore, investors are evaluating whether the assets and stock market may be overpriced considering the Fed is now likely to cut within the first 6 months of 2024.

According to Bloomberg, investors are less worried about when rate cuts will start as long as further hikes are unlikely. This is largely due to positive data and expectations of a “soft landing”. This shows the economy can deal with higher interest rates. The main concern for investors is that inflation does not rise. Thursday’s Consumer Price Index is likely to be particularly influential and inflation is expected to rise for the first time since September. If the Consumer Price Index reads higher than 0.2%, the USA100 potentially could witness a significant decline. Buyers will be hoping inflation reads no higher than 3.1%, or even better slightly declines.

The price movement this morning is trading lower, and investors’ main concern is the US market’s bond yields which are significantly higher. Higher bond yields can pressure the stock market and if yields continue to rise, stocks will become less attractive. Currently, the price of the USA100 is trading below the 75-Bar trend line, below the VWAP and below the neutral on the Relative Strength Oscillator. All three indicators point towards a potential decline. However, investors should note this is likely to change if the price rises above $16,435.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The USA100 Climbs 2% and Chip-Makers Shine Ahead of Earnings.

*The USA100 climbs more than 2% as sentiment changes ahead of this week’s US consumer and producer inflation data.

*The US Dollar Index trades sideways as investor sentiment improves but participants are not yet fully disposing of the Dollar.

*Analysts advise the performance of the Dollar will largely depend on Thursday’s inflation data.

*Semiconductor companies such as NVIDIA and AMD outshine the rest of the stock market and particularly support the USA100 and SNP500.

USA100 – Can Stocks Hold onto Gains and Avoid Investor’s “Cashing In” Monday’s Profits?

The USA100 on Monday witnessed its strongest price increase since mid-November 2023 as investors take advantage of the lower entry price to position themselves ahead of US consumer inflation on Thursday. However, the lower price also provides an advantage for buyers to enter prior to the start of the earnings season.

The asset’s volatility will be considerably higher than normal and did not form a retracement for the whole of the US trading session. This clearly shows the session was dominated by buyers and that the market believes inflation will not rise above expectations. The strong bullish momentum is also a result of strong demand for stocks in the “Semiconductor” segment. This is most likely due to their strong earnings and growth over the past five quarterly earnings releases. NVIDIA stocks rose 6.43% and AMD rose 5.45%. Both are influential stocks for the USA100 and USA500.

When looking at the performance of the USA100’s components we can see all the top 20 most influential stocks holding the highest weight rose in value. In addition to this, 93% of the index ended the day higher and only 7% recorded a decline.

Bond yields this morning are higher again adding a further 0.040%, but the US Dollar sees little change. The higher bond yields are negative for the stock market if they remain high. For example, yesterday bond yields started higher but could not hold onto gains allowing stocks to rise. If bond yields and the Dollar both rise, traders may consider the possibility of investors cashing in yesterday’s profits. Though in the medium-term the price will depend on Thursday’s inflation data which will determine how rates may change.

In terms of technical analysis, the asset is witnessing clear buy signals due to the quick and strong upward price movement. However, investors will need to monitor crossovers, breakouts, and indicators throughout the day to determine how the price may develop in the short-term.

USDJPY – Japanese Inflation Data Declines as Expected!

The US Dollar is decreasing in value this morning for a third consecutive day, but not at a momentum to yet spark major sell signals. Investors in the Dollar are treading cautiously until the release of the US inflation data. If US inflation does indeed climb from 3.1% to 3.2%, a rate cut would indeed become unlikely for several months. According to some analysts, if inflation remains sticky for more than 2 months, rate cuts will not be likely until the last few months of the year.

However, if inflation declines and remains at 3.1%, the Dollar potentially can trade weaker. Up to now the strong employment sector and weakening inflation rate over the past 6 months has made a “soft landing” more likely. As a result, investors have been less interested in the Dollar and other safe haven assets such as bonds. However, this will only continue if a soft landing remains the most likely outcome and inflation remains low.

If the price rises above 144.305, buy signals are likely to materialize as bullish crossovers form and the price breaks the bearish wave pattern. However, if the price breaks below 143.65, the short-term crossover will point downwards.

The price movement this morning is trading lower, and investors’ main concern is the US market’s bond yields which are significantly higher. Higher bond yields can pressure the stock market and if yields continue to rise, stocks will become less attractive. Currently, the price of the USA100 is trading below the 75-Bar trend line, below the VWAP and below the neutral on the Relative Strength Oscillator. All three indicators point towards a potential decline. However, investors should note this is likely to change if the price rises above $16,435.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

JPN225 Again Renews its All-Time Highs, Yen Down Against All Currencies!

*China keeps interest rates on hold at 2.5%, whereas investors were previously expecting another rate cut. Asian stocks mainly rise after the Bank of China announcement and Taiwan election results.

*The World Economic Forum kicks off in Davos. Economists, brokers and bankers will be discussing the global economy, interest rates and inflation throughout the day. Traders will be listening keenly to how bankers view inflation after US and EU inflation rose.

*No US trading on Monday 15th, for Martin Luther King Day, meaning limited volatility for the Dollar. Friday’s earnings data “mixed” and provides no particular support for stocks.

*The Pound sees “mixed” price movement on Monday before the release of major economic data for the UK.

GBPJPY – Investors Await UK Employment Data and Inflation!

Investors turn their attention to the GBPJPY ahead of major economic releases for the UK. Additionally, the Yen struggles against all currencies on Monday providing FX traders with further opportunities. The GBPJPY has risen 0.40% in this morning’s Asian session and continues to obtain buy signals from indicators. The Pound has been supported by the UK’s Gross Domestic Product which rose 0.3%. As a result, the UK economy continues to avoid a recession and the Bank of England is less likely to consider interest rate cuts.

The growth in the UK’s Gross Domestic Product was primarily due to the acceleration of the services sector by 0.4%. From the G7, the Bank of England is the regulator which is expected to cut interest rates the least. Investors expect the Federal Reserve to cut rates in March or May, whereas the Bank is England is not likely to do so until the Summer. If this transpires, the Pound can potentially gain, particularly if the Bank of Japan remains ultra dovish.

The Pound is likely to experience a lot of volatility over the next two days due to four upcoming announcements. These include the change in Unemployment Claims, Average Earnings Index, the Bank of England Governor Speech, and the UK Consumer Price Index. If the UK’s employment sector remains resilient and inflation remains above expectations, the Pound is likely to again rise. Analysts expect inflation to decline from 3.9% to 3.8%. However, the Pound potentially can increase if inflation does not decline. Anything below 3.8% will be considered positive for the Pound.

In terms of technical analysis and indicators, the exchange rate has been obtaining buy signals since January 3rd. Since then, the price continues to trade above the price sentiment line, above 50.00 on the RSI and continues to form higher lows. If the price increases above 185.495, further buy signals will be seen as the asset crosses the 61.8 mark (Fibonacci). However, investors should note that this will also depend on tomorrow’s UK employment data and Bank of England Speech.

Nikkei225 Continues to Renew its All-Time Highs

Earnings season started on Friday, with mixed results from the banking sector. However, the global stock market performed generally well as US Producer Inflation unexpectedly fell. The JPN225 is increasing in value for a ninth consecutive day and is trading more than 6% higher than its previous all-time highs. The bullish price movement is a result of an ultra-supportive monetary policy and a weakening Japanese Yen.

Economists expect that the Bank of Japan in its quarterly outlook report will cut its initial estimate of inflation. This is considered a key indicator of the broader price trend, believed to weaken from the current 2.8% to 1.9% for both fiscal year 2024 and 2025. As consumer price growth has beaten the 2% threshold for more than 12 months, investors believe that the central bank will abandon its ultra-loose policy and increase the interest rate. The Bank of Japan’s interest rate has been at -0.10% since 2016. If rates rise, the JPN225 may struggle to hold onto gains unless earnings remain strong, and the global economy experiences higher growth.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Dollar Demand Rises and Global Stocks Tumble, Find Out Why!

*Investors price in 6 rate cuts in 2024, but all Fed members remain hawkish. Economists advise investors are getting ahead of themselves and the Fed is only likely to cut 3 times.

*Finance giants gather in Davos and advise markets rate cuts are premature and the risk of inflation still remains.

*Trump beats Ron DeSantis in Iowa and is on track to represent the Republicans in the 2024 US elections.

*The UK’s employment sector remains resilient, but salaries again see a considerable slow-down. The salary slowdown pushes the Pound lower.

GBPUSD – UK Salaries Decline And Dollar Demand Rises

The GBPUSD is trading at its lowest level since January 5th after being pushed lower by Dollar strength and UK data. The US Dollar Index has been increasing in value for 3 consecutive days due to higher inflation data and hawkish comments from global banking leaders. Another indication that interest rates are likely to remain high is this week’s bond yields. During this morning’s Asian session, the US 10-Year Bond Yields rose 0.055% and again rose above 4.00%. Higher bond yields are known to be Dollar bullish, but investors will monitor if bond yields can hold onto gains. This is something yields were not able to achieve last week.

The Pound this morning is declining against all currencies which provides traders with clear opportunities within the GBPUSD. However, the data from the UK is not “all bad” for the Pound. The UK’s Claimant Count Change read 11,700, lower than previous expectations and lower than the previous 3 months. Strong employment means higher consumer demand and means a trickier fight against inflation. However, the lower earnings do help regulators fight against inflation. As a result, investors are ditching the Pound in favor of the Dollar.

According to analysts, investors today have preferred the Dollar where there is already confirmation that inflation rose. Nonetheless, the Pound may correct if tomorrow’s UK inflation data is higher than the 3.8% expectations. Though, if inflation does read 3.8% or lower, the Pound may witness further downward momentum.

When evaluating indicators and technical analysis, the GBPUSD exchange rate is currently witnessing potential sell signals. The price is trading below trend-lines, average price movements and below the neutral on most oscillators. The price is also trading below the regression channel and the regression channel is also widening while declining. All the above indicates downward price movement, however, if the price rises above 1.27127, these signals can potentially change.

US30 – Global Sentiment Towards Stocks Declines. Eyes on Goldman Sachs Earnings!

The US30 is experiencing a decline during this morning’s Asian session, similar to all other US indices. The US30 was pressured by negative earnings data from the banking sector on Friday as well as the possibility of less rate cuts this year. However, technical analysts remind investors that the price has declined to a previous support level which the asset has not been able to break on the past 3 occasions. Traders monitor the price action as the asset tests this support level.

The next vital announcement for the asset will be Goldman Sach’s earnings report which will be made public before the US Session opens. Analysts expect the banking giant to see a 23% drop in earnings per share and a slight decline in revenue. Though, if the data is lower than expected, the stock price can decline. Goldman Sachs is the third most influential stock within the Dow Jones and holds 6.63% of the index.

Lastly, another negative for the USA30 is the stock market performance today globally; UK, EU and Asian indices are trading lower. The poor sentiment within the stock market is largely due to hawkish comments from the Fed and finance ministers in Davos. Analysts advise investors are pricing in up to 6-7 rate cuts in 2024, but banks are predicting 3-4.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Eurozone Economic Trends: Inflation, Growth, and Central Bank Outlook.

In the ever-evolving landscape of the Eurozone economy, key indicators suggest a complex scenario of lower inflation and weakened growth. While central bank officials express optimism about a potential soft landing, the ongoing improvement in German ZEW investor confidence supports this outlook. As we delve into the intricacies of economic data, it becomes evident that the European Central Bank (ECB) is contemplating rate cuts later this year, despite maintaining a cautious wait-and-see stance, while investors are onec again buying into hopes of early trade cuts.

Eurozone data so far was mixed, with German HICP ticking up at the end of 2023 and German ZEW investor confidence coming in stronger than anticipated. At the same time, consumer inflation expectations declined, according to the latest ECB survey. ECB officials meanwhile continued to signal that it is too early to talk about rate cuts, even if ECB’s Villeroy repeated that rates are set to decline this year.

German Inflation Landscape: German HICP inflation, confirmed at 3.8% y/y for December, reflects a nuanced picture. The rise in national CPI to 3.7% y/y is partly attributed to base effects from a one-off energy support payment in December 2022. Notably, food price inflation eased to 4.6% y/y, contributing to an overall inflation rate of 3.5% y/y when excluding energy and food. The challenge lies in the impact of these rising prices on disposable income, weighing on demand and overall growth.

Economic Contractions and Optimism: The German GDP contracted -0.3% last year, with adjusted figures showing a flash estimate of -0.1%, potentially indicating a technical recession in the latter half of 2023. Factors such as high inflation, increased debt financing costs, and weakened domestic and external demand have posed challenges to the recovery from the pandemic. Despite these setbacks, German ZEW investor expectations unexpectedly improved, suggesting a cautious optimism driven by hopes of major central bank rate cuts.

Eurozone Industrial Production and Trade Dynamics: Eurozone industrial production contracted -0.3% m/m in November, aligning with expectations and signaling a potential decline in GDP for the last quarter of 2023. Concurrently, the Eurozone seasonally adjusted trade surplus widened to EUR 14.8 billion in November, driven by a rise in exports and a decline in imports. However, the subdued improvement in real terms indicates that the widening surplus may not necessarily signify an overall economic upturn.

Central Bank Insights and Currency Movements

ECB officials remain vigilant, emphasizing that it is premature to declare victory over inflation. Despite differing opinions within the central bank, the latest ECB survey shows a drop in consumer inflation expectations. Geopolitical risks further complicate the outlook, with potential impacts on inflation. Austrian central bank head Holzmann cautions against expecting a rate cut in 2024 amid increasing geopolitical threats.

In the current WEF Annual Meeting, ECB’s Lagarde flagged rate cuts in the summer. When asked about a possible rate cut in the summer the central bank head told Bloomberg she suggested that there is likely to be a majority in favor of such a move by then, but cautioned that the ECB has to be “data dependent”. Lagarde stressed “that there is still a level of uncertainty and some indicators that are not anchored at the level where we would like to see them”. Meanwhile, ECB’s Knot stated it’s unlikely that rates will go up again, but he warned that the ECB needs to see a turnaround in wages before making a decision and that any easing, if it happens, will be very gradual. Knot also stressed that the more easing markets are pricing in, the less likely it is that the ECB will indeed cut rates. More push back against excessive rate cut expectations has put bonds under pressure this morning, amid the large number of central bankers stressing that rate cuts are not on the agenda for now.

US30 – Global Sentiment Towards Stocks Declines. Eyes on Goldman Sachs Earnings!

EURO: Central Bank and Growth Outlooks Influence Exchange Rates

In the currency markets, EURUSD has undergone correction in response to central bank and growth outlook uncertainties. With the USDIndex surpassing the 103 mark and Treasury yields fluctuating, EURUSD corrected to 1.0883, reflecting the dynamic interplay of market forces.

EURJPY has been oscillating within the 158.50-160.00 range after experiencing a robust rebound to a one-month peak of 160.17 last week.

From a technical perspective, the short-term range is delineated by the 50% and 61.8% Fibonacci retracement levels from the previous decline. Notably, the sequence of higher highs and higher lows, initiated from December’s low point, remains encouraging.

Furthermore, the Relative Strength Index (RSI) is still hovering above its neutral mark of 50, and the Moving Average Convergence Divergence (MACD) is showing marginal strengthening, positioned slightly above its zero and signal lines. This maintains a positive bias in the market sentiment.

Practically, for the bullish momentum to persist, a decisive close above the 160.00-160.50 zone is essential. This breakthrough could pave the way for an advance towards the 78.6% Fibonacci level at 162.00 and the previously breached ascending trendline from March 2023, located at 162.70. Further upward movement may retest the ceiling observed in November at 163.70-164.28.

Conversely, if the price dips below the 158.50 support, a period of consolidation might occur around the 38.2% Fibonacci level at 157.40 before sellers target the lower boundary of the bullish channel at 156.45. A bearish breakout from this point could extend towards the 200-day Exponential Moving Average (EMA) positioned at 155.20.

In summary, while EURJPY retains bullish momentum, a sustained breach above the 160.00-160.50 region is crucial for a more significant upside potential.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.