Strong Chinese Economic Data Prompts Demand for US Stocks!

Trading Leveraged Products is Risky

* The Chinese economy and sentiment improve for the first time since September 2023. Chinese Manufacturing PMI rose to 50.8, beating expectations. Higher Chinese data improves the global risk appetite towards stocks.

* Stocks trade higher, what is more, the SNP500, and Dow Jones again renew their all-time highs. The latest Chinese data and a PCE Price Index in line with expectations support price growth.

* The price of Gold and the US Dollar Index are both on the rise, which is a concern for investors. The market’s price movement gives no clear indication of investor’s risk appetite.

* Apple is expected to confirm the Vision Pro Headset will be made available to global consumers in the summer months.

USA500 – Inflation, Earnings and Company News!

The USA500 starts the day with a moderate bullish price gap measuring 0.21% and continues trading 0.52% higher ever since. The price of the index is now trading at an all-time high and has risen more than 10.50% in 2024. The SNP500 has also been the best performing index in 2024 and has outperformed both the NASDAQ and Dow Jones? The question for traders is, will this continue?

A positive factor for the USA500 is the Federal Reserve and most global central banks are likely to start cutting interest rates at some point this year. The main factor which investors needed to see is that central banks were able to do so without triggering a significant economic contraction, which was achieved. Another positive factor is the Core PCE Price Index did not beat expectations, which was vital considering inflation over the past 2 months kept reading higher than previously thought.

However, some risks do remain which can make the path difficult for buyers. The price of Gold as well as the price of the US Dollar continue to rise. This occurrence indicates the market’s risk appetite and sentiment is lower than priced in the stock market. Another concern is whether the Federal Reserve will be able to indeed cut interest rates in July 2024 if inflation does not decline over the next 2 months.

Investors are closely watching the price of oil which is trading 13.50% higher in 2024 and at a 6-month high. If the price of Oil continues to rise and fails to fall back below $80.00 per barrel in the next two months, inflation will be difficult to reduce. As a result, the Fed may again push back a rate cut to July or September. Otherwise, the Fed may continue with a cut in June, but will advise less than 3 cuts for the remainder of the year.

So, what can save the SNP500 and stock market if the Fed chose not to cut and if inflation rises. The answer is the quarterly earnings reports scheduled for later this month and in May. Investors will mainly be focusing their attention on the following stocks:

1. Microsoft 2. Apple 3. NVIDIA 4. Alphabet 5. Amazon 6. Meta

The stock which is a concern for investors is Apple Stocks. Apple has received a large penalty from the EU and is now facing a lawsuit from the US. Shareholders will be keen to see what the board of directors have to say regarding this and how it will affect the earnings per share. Investors will also be keen to see the performance of the Apple Vision Pro Headset which was released in February. If the sales figure reads as expected or beats expectations, the demand for the stocks can rise regardless of the upcoming fines. Apple is also expected to announce that the product will be made available to global consumers later in the summer. Apple quarterly earnings will be released on May 2nd and Microsoft on April 23rd.

USA500 – Technical Analysis After Strong Chinese Economic Data

Over the past 3 trading days, the price of the USA500 has successfully been forming higher highs and higher lows. The price this morning saw strong momentum, which was also due to positive economic data from China. The Chinese Manufacturing and Non-Manufacturing PMI beat expectations. Furthermore, technical indicators continue to indicate a higher price. The price remains above the 75-Bar EMA and above the 50.00 level on the RSI. In addition to this, delta statistics also indicate buyers are controlling the market. If the price again rises above $5,273.31, the breakout will further indicate upward price movement.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

* Treasuries were hit by stronger than expected ISM data and yields climbed sharply in a bear steepener. – US manufacturing unexpectedly expanded for the first time since September 2022 & input costs climbed.

* The latest ISM data indicates that the US economy continues to display strength despite elevated interest rates. This bodes well for the stock market, as it has the potential to fuel profit growth for businesses. However, it also raises concerns about inflationary pressures.

* Wall Street took its lumps to start Q2 amid the eroding Fed view and the pop in interest rates. The broader indexes closed with losses, though from fresh record highs last Thursday.

* FED: Expectations are moving toward fewer cuts this year as well, from the 3 that have been in for priced in much of 2024 to date, consistent with the FOMC’s dots, to 2, 1, or even none. A couple of key Fed officials, Waller and Bostic, have indicated their preferences for fewer than 3 cuts this year. Now there is a 61% chance of the Fed cutting rates in June.

* UK Nationwide house prices unexpectedly dropped -0.2% m/m in March, after rising 0.7% m/m in the previous month.

Market Trends:

* The Dow dropped -0.6% and the S&P 500 slid -0.2%. The NASDAQ managed a 0.11% rally.

* European stock futures are slightly higher in early trade, with the FTSE 100 outperforming. The Hang Seng rallied overnight, as Hong Kong’s markets re-opened after the extended holiday weekend and investors reacted to the better than expected Chinese PMI reports.

Financial Markets Performance:

* The USDIndex climbed back over the 105 level thanks to the strength in the data, closing at 105.019 and hitting the highest closing level since mid-November. Underpinning * the move has been the hotter inflation data and resilient growth that have been shifting outlooks on the FOMC’s rate cutting trajectory, pushing back the timing of the first move toward July rather than June.

* The Yen was steady higher at 151.70. Focus is now fixed squarely on the BOJ’s bond-buying operation scheduled for Wednesday.

* Gold managed to hit a fresh peak at $2251.44 per ounce and a second close over $2200.

* USOIL breached 61.8% Fib. level since the September downleg, at $84.14. (Rising geopolitical risks in the ME & tighter supply from Mexico helping to buoy prices.)

* Bitcoin drifted back to $67k amid cooling demand for dedicated US ETFs and ebbing bets on looser Fed policy. – 10% down since $73,798 highs in mid-March.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

* Rate cut hopes for the US are fading, which is weighing on stock markets. Bonds have found a footing, at least outside of the US, and the 10-year Bund yield is down -1.4 bp, after the 10-year JGB corrected -1.3 bp.

* A rise in February JOLTS, albeit after a downward revision to January, and a better than expected factory report, exacerbated the sell off in longer dated Treasuries.

* Disappointing delivery news from Tesla, along with weakness in the health and retail sectors, weighed on sentiment.

* Rising geopolitical risks boosted Gold and Oil.

* Fed’s Mester(Voter) & Daly (Voter): They still see 3 cuts this year, which helped trim losses. Mester stated that she will not vote for a cut at the May meeting given the lack of sufficient data but said she would not rule out action in June.

* China’s manufacturing activity expanded at the fastest pace in 13 months in March. Yuan declined despite data.

* Today: EU Inflation & Core, US ADP, US ISM Services and Fed Powell speech. OPEC ministerial meeting is also on tap and it is expected to confirm current output cut targets.

Market Trends:

* Wall Street slumped as well on JOLTS and hence the Fed outlook and the rise in yields with the major indexes falling over -1.0% before paring losses. The Dow finished with a -1.0% drop, while the S&P500 was down -0.72% and the NASDAQ -0.95% lower.

* Stocks have sold off across Asia, with Hang Seng and ASX underperforming and losing more than -1%. US futures are also in the red, while European futures are narrowly mixed.

Financial Markets Performance:

* The USDIndex climbed to hit 105.10, but it lost traction and slid to close at 104.52 with a pick up in downside momentum after the Fedspeak. Monday’s 105.019 close was the first with a 105 handle since mid-November.

* The AUD & NZD (often used as liquid proxies for the CNH), are under pressure as a result of a stronger USD and a weaker CNH.

* Gold (+11% this year) surged to a new all-time peak at $2288 even as Fed rate cut bets were pared. Silver hit a 2-year high.

* USOIL was up 1.9% at $85.30 per barrel with additional support from expectations for rising demand.

* Bitcoin at $66.3K, under pressure for a 3rd day in a row.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – USD continues to decline; stock markets mixed.

Trading Leveraged Products is Risky

Economic Indicators & Central Banks:

* Powell wants to keep inflation expectations anchored at 2%. – Recent data have not “materially” changed the overall picture.

* Nothing new is added to the outlook, keeping the door open for several rate cuts this year, though Bostic continues to favor just one easing.

* The ISM services index slowed and prices paid softened, but the ADP solidly beat.

* JGB and Treasury yields have moved up overnight, with the US 10-year 1.8 bp higher on the day.

* Bunds are finding buyers though, with Eurozone spreads narrowing as peripherals outperform.

* Fed funds futures: implied rates are now about 50-50 for a June cut, with July showing about a 95% probability for the first cut. A 25 bp easing is not fully priced until September.

* Swiss inflation drops to just 1.0% y/y. Expectations had been for a slight uptick in the headline and the lower than expected number will justify the SNB’s decision to cut rates at the previous meeting, especially as the growth outlook remains subdued.

* The ECB asserts it won’t rely on the Federal Reserve’s actions to determine when to start reducing interest rates. However, economic trends in the US often swiftly affect other regions, impacting financing conditions, exchange rates, and various metrics such as inflation and trade.

Long Shadow of the Fed Shows Limits of ECB Talk of Independence

Market Trends:

* Wall Street closed with a 0.23% advance in the NASDAQ, a 0.11% gain on the S&P500, and a -0.11% dip on the Dow.

* Stock markets traded mixed across Asia. Nikkei and ASX benefited while China bourses corrected though and the Hang Seng underperformed once again.

* European bourses are slightly in the red, US futures are higher, as markets continue to evaluate rate outlooks and growth prospects against the background of geopolitical risks.

Financial Markets Performance:

* The USDIndex is below 104, in the wake of Powell’s comments along with the stronger than projected ADP which weighed on the markets, and Bostic’s comments.

* The Yen continues to consolidate as investors awaited cues from the BOJ. BOJ board member Sakurai said that the central bank is likely to wait until around October before mulling another interest rate hike.

* Gold remained stable after reaching a new all-time high, surpassing $2,300 per ounce. This surge was supported mainly by Powell.

* USOIL appeared ready for its 5th consecutive day of increases.

* Copper rose to its highest level since January 2023, driven by increasing supply risks and indications of heightened demand

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – NFP day; Geopolitics triggering a flight to safety!

Trading Leveraged Products is Risky

Economic Indicators & Central Banks:

* Global Stocks fell ahead of today’s jobs report, which coupled with the rising geopolitical risks and the angst over the FOMC’s rate trajectory triggered a flight to safety, hence boosting the haven demand.

* Treasuries climbed, the US Dollar ended near session highs and Oil rallied.

* Israeli Prime Minister Benjamin Netanyahu said at a security cabinet meeting his country will operate against Iran and its proxies and will hurt those who seek to harm it. President Joe Biden told Netanyahu on a call that US support for his war would depend on new steps to protect civilians.

* Note: A direct conflict between Israel & Iran could restrict further Oil supply and hence could boost Oil above $100.

* Japan: BOJ Governor Ueda stoked bets about an additional interest rate hike later in the year, if the yen’s weakness affected the economy. FM Shunichi Suzuki repeated warnings that the government would take appropriate measures to support the currency. Meanwhile, former top currency diplomat Hiroshi Watanabe said earlier this week that the government likely won’t make a move unless the Yen plunges below 155 per dollar.

Financial Markets Performance:

* The USDIndex has rallied into the close from the session low of 103.92, finishing back at 104.12. But it was over 105 on Monday, the highest since November.

* The Yen extended a rally to hit a 2-week high. The currency experienced its most significant surge against the USD in nearly a month, prompting a retreat from levels that traders had anticipated might trigger intervention.

* Gold: The rising concerns over the situation in the Middle East have boosted haven demand for gold which climbed to another record peak over $2304 per ounce.

* USOIL jumped to $86.70 and UKOIL rose above $91 near its highest since October. Israel has increased preparations for potential retaliation by Tehran after Monday’s strike on an Iranian diplomatic compound in Syria, stoking fears of a wider regional conflict. OPEC kept global markets tight.

* Copper holds at 14-month highs.

Market Trends:

* Wall Street had a tough session and closed with steep losses of over -1%. The recent record peak on stocks have left the market ripe for profit taking too ahead of jobs.

* The NASDAQ dropped -1.4% and the Dow tumbled -1.36% with the S&P500 slumping -1.23%. Every S&P sector closed with a loss, with only energy preventing a complete rout in the Dow.

* Nikkei drifted more than 2% putting it on course for its worst week since December 2022 as tech shares slid on Wall Street’s lead. – The biggest driver for the Nikkei’s dip is technical.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Treasury Yields Climb and Investors Anxiously Await March’s Inflation Reading!

* Economists expect inflation to rise from 3.2% to 3.4%, but the monthly incline to be lower than the previous month.

* The Dow Jones sees its worst week of 2024, but stocks rebound on positive employment data.

* The US economy added a further 303,000 more employed individuals and the unemployment rate fell to 3.8%.

* The US Dollar witnesses “mixed” price movement as investors wait for inflation confirmation and clarity on interest rates.

USA500 – Bond Yields Rise 50 Points Potentially Pressuring US Stocks!

The SNP500 is the index which is likely to be most influenced by this week’s earnings data. This is due to the index’s exposure to banking stocks. The price of the USA500 is technically still forming lower lows and lower highs which indicates a downward trend. However, corrective waves remain strong which indicate demand remains. Currently, the price is trading below momentum indications and below the “neutral” on oscillators. Therefore, the price is currently witnessing a weak “sell” signal. However, if the price drops below $5,197.16, indicators are likely to signal a stronger bearish signal.

To obtain further indication of the possible future price movement, investors will also be monitoring the global investor sentiment. Asian stocks are currently trading slightly lower, but the European Cash Open is yet to take place. If both Asian and European stocks decline, this could potentially back a low-risk appetite, which is negative for the USA500.

The employment data on Friday, reassured investors that the US economy remains strong and resilient to the current monetary policy. The NFP data read 43% higher than market expectations and average salaries rose more than the previous month. On the one hand, the data is positive as it indicates demand will remain high as will company earnings. However, on the other hand, if inflation also rises, the Fed will be unlikely to adjust interest rates.

Therefore, Wednesday’s Consumer Price Index will be key. If inflation reads higher than 3.4%, the stock market can come under immense pressure as the Fed are likely to become more hawkish. This is something which can already be seen from today’s rise in bond yields. The US 10-Year Treasury yields added 0.050% which is known to apply pressure to the stock market. If inflation reads in line with expectations, the release will be neutral. Furthermore, analysts expect the Core Inflation rate to fall from 3.8% to 3.7%.

EURUSD – ECB To Indicate Next Cut!

The Euro is witnessing “mixed” price movement depending on the currency pair. Against the US Dollar the exchange rate is moving sideways, and the key price can be seen at 1.08426. Both the Euro and the US Dollar are likely to witness volatility throughout the week. The Euro due to the European Central Bank’s rate decision and press conference. The US Dollar due to Consumer and Producer Inflation.

Some economists believe the ECB may deem it too early to cut interest rates, but the general opinion is that the time to cut is very near for the ECB. Therefore, investors will closely be monitoring the President’s comments in the press conference on Thursday. The EU’s inflation rate has fallen to 2.4% and is the lowest amongst the G7. In addition to this, many EU economies have been witnessing prolonged stagnation and therefore will be keen to stimulate economic growth. The US Dollar on the other hand will primarily be determined by the CPI and PPI (producer inflation).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Gold Renews Its All-Time Highs, But Oscillators Point to Caution!

Trading Leveraged Products is Risky

* US indices underperform compared to global stocks as investors await the latest US inflation data.

* Oil is trading almost 22% higher in 2024 applying upward pressure on inflation and triggering a more cautious approach to tomorrow’s Consumer Price Index.

* The US Dollar declines and Gold rises in value despite the possibility of a more hawkish Federal Reserve.

* The head of the Federal Reserve Bank (FRB) of Dallas, Mrs Logan, advises it’s too early to think about lowering interest rates since the danger of inflation stabilizing above the target level remains.

XAUUSD – Buyers Maintain Control but Oscillators Point To The Assets Being Overpriced

The price of Gold trades steadily higher during this morning’s Asian session and is attempting to break yesterday’s all-time high. Gold has risen more than 15% since February 2024 as investors look at an alternative hedge against inflation. In addition to this, many countries including China and India look to lower exposure to the Dollar ahead of US elections. However, investors should note that if US inflation reads higher than expectation, demand for the Dollar may return.

Investors also should note that the inverse correlation between Gold and the US Dollar is slightly weaker than traditionally seen. Therefore, even with a more expensive Dollar, the price of Gold may simply retrace or correct, but retain the longer-term gains. According to Friday’s report from the US Commodity Futures Commission, the number of speculative positions for “sellers” remains weak. The latest report confirmed that only 0.719k more contracts were added for sellers and more than 21.200k added for buyers.

Technical analysis for Gold is two sided. Momentum-based indicators point towards an upward price movement as does price action. However, oscillators indicate the asset may be trading above its intrinsic value and may correct. A short-term correction may decline between 2,292.29 and 2,318.78. For another bullish impulse wave, technical analysts point at a target of 2,376 based on Fibonacci levels and the size of previous impulse waves.

EURUSD – ECB Rate Cut Upcoming According to Analysts

The Euro is gaining momentum since the start of the European Trading session. However, the price is trading slightly lower than the day’s open price. In addition to this, in the short-term the price is forming lower lows and lower highs. When monitoring each currency individually, the US Dollar is trading slightly higher while the Euro is unchanged.

No major economic data has been released in the past 24 hours or is due today. However, volatility is likely to significantly rise from tomorrow onwards. If US consumer inflation reads 3.5% or more, the price of the Dollar is likely to gain. If the monthly producer inflation on Thursday also reads higher than 0.3%, this will further fuel a potential bearish impulse wave.

However, another key factor will be the European Central Bank’s Rate Decision and Forward Guidance. If the ECB suddenly become more dovish, as analysts believe, the Euro may again struggle to hold onto its value, if the Fed are unlikely to adjust. Currently there is more pressure on the ECB to cut interest rates considering inflation has returned to normal levels amongst most state members and most countries are witnessing stagnation. Analysts currently expect the European regulator to be the first to cut interest rates and believe this will take place in June.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The Fed Is Willing To Lower Expectations To Only 1 Cut In 2024!

* European defence stocks tumble and see the largest decline in 18 months as Goldman Sachs analyst warns the category is trading above its true value.

* US Treasuries Yields and the US Dollar Index remain unchanged as investors hold their breath ahead of today’s inflation release.

* Analysts expect US inflation to increase from 3.2% to 3.4%, but for Core inflation to decline to 3.7%.

* Federal Reserve President of the Atlanta bank, Mr Bostic, advises he is willing to adjust the outlook to only 1 rate cut in 2024. Keep reading to find out why and what the requirements will be.

GER40– Defence Stocks Overvalued According to Goldman Sachs

The DAX as well as general European Indices came under pressure from comments from a market respected analyst. According to the Goldman Sachs Analyst, Victor Allard, shares in European defensive stocks were trading above their true value and have little potential for further gains. As a result, stocks such as Rheinmetall AG, BAE Systems and Saab AB witnessed sharp declines. Saab AB stocks fell almost 10% within a single session.

However, the sentiment towards European stocks were dampened as a result of this. The main reason for Mr Allard’s view is the stock ratios do not back the growth. A good example of this is the price to earnings which is extremely high. Furthermore, Allard pointed out that defence stocks trade now at nearly 20 times forward earnings.

When monitoring the top 7 stocks which hold the highest weight within the index, the market can see a clear sign of profit taking. Five of these stocks have risen more than 10% in 2024 so far, which is higher than traditional gains, but over the past five days a large portion of that has been lost. The only stock which has seen strong gains and has maintained its momentum is Mercedes Benz which has risen almost 22% in 2024 so far. The most important stocks for the index during this earnings data will remain SAP SE, Siemens AG and Allianz.

The price of the index will now largely depend on tomorrow’s European Central Bank press conference and statement. Investors are keen to see when the ECB and Federal Reserve are likely to cut interest rates. If the regulator takes a more dovish approach, the economy is likely to witness much needed stimulation and investor sentiment towards the region is likely to rise. In addition to this, the Euro can potentially make indices cheaper to buy. As a result, this can support the DAX as well as other European indices. In the meanwhile, this afternoon’s US inflation data will be the key price driver for all assets.

USA100 – Price Performance Dependent on Fed Rate Adjustments and Today’s CPI!

The performance of the USA100 will primarily be dependent on this afternoon’s inflation data. However, technical analysts have been keen to point out that the US stocks have been unwilling to form strong longer-term declines. Nonetheless, higher inflation potentially can trigger a lower risk appetite and lower demand for equities. Particularly investors will be looking to see if inflation reads higher than the 0.3% expectations, including the Core CPI.

Later within the evening, investors will also be closely monitoring the FOMC Meeting Minutes for clues as to where the committee stand on possible interest rate cuts. This week Mr Bostic has already advised he would be willing to lower expectations for future cuts if inflation does not allow the Fed to act. According to Mr Bostic, he could consider lowering possible future adjustments from 3 cuts to only 1 for 2024. However, Mr Bostic said this was only possible if inflation stabilized above the target and the employment sector remains resilient. So far, jobs growth remains and it’s all dependent on inflation.

Technical analysis for the USA100 is signalling neither a sell or buy. The price is trading slightly higher than the 75-Bar EMA and at the 55.00 mark on the RSI. However, the price is forming a horizontal price range this morning. Therefore, for a buy signal to be confirmed, the price will need to form a bullish breakout and ideally inflation will not beat expectations.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Producer Inflation On The Rise, But Will Earnings Hold Demand Steady?

Trading Leveraged Products is Risky

* Producer inflation rose slightly less than previous expectations, but the annual figure continues to rise. The annual PPI rose to 2.1% and the Core PPI rose to 2.4%.

* The NASDAQ and SNP500 end the day higher, but the Dow Jones continues to struggle.

* This morning earnings kick off with the banking sector including JP Morgan, BlackRock and Wells Fargo. All 3 stocks trade higher during pre-trading hours.

* The Euro trades lower against all currencies despite the ECB’s attempt to establish a hawkish tone.

USA100 – The NASDAQ Climbs Higher, But Is the Growth Sustainable?

The NASDAQ was the only index which did not witness a significant decline at the opening of the US session. In addition to this, the USA100 is the only index which is witnessing indications of a bullish market.

The price has crossed onto a higher high breaking the resistance level at $18,269. The index is also trading above the 75-Bar EMA and at the 65.00 level on the RSI which signals buyers are controlling the market. However, a similar large bullish impulse wave was also formed on the 3rd and 5th of the month and was followed by a correction. Therefore, investors need to be cautious of a bearish breakout which may signal a correction back to the 75-bar EMA (18,165). The medium-term growth and its sustainability will depend on the upcoming earnings data.

Bond yields declined during this morning’s Asian session by 18 points, which is positive for the stock market. However, even with the decline, bond yields remain significantly higher than Monday’s opening yield. This week the 10-year bond yield rose from 4.424 to 4.558, which is a concern. If bond yields again start to rise, the stock market potentially can again become pressured.

25% of the NASDAQ ended the day lower and 75% higher. This gives a clear indication of the sentiment towards the technology sector and reassures traders about the price movement. Another positive was all of the top 12 influential stocks rose in value. Apple, NVIDIA and Broadcom saw the strongest gains, all rising more than 4%.

Producer inflation read slightly lower than expectations, however, the index continues to rise. The Producer Price Index rose from 1.6% to 2.1% and the Core PPI from 2.1% to 2.4%. Therefore, it is not indicating inflation will become easier to tackle in the upcoming months. For this reason, investors should note that inflation and the monetary policy is still a risk and can trigger strong bearish impulse waves.

EURUSD – The Euro Declines Against Major Currencies

The European Central Bank is attempting to concentrate on the positive factors and give no indications of when the committee may opt to cut rates. For example, President Lagarde advises “sales figures” remain stable, but the issue remains they are stably low.

Officials said the decline in prices generally confirms medium-term forecasts and is ensured by a decrease in the cost of food and goods. Most experts continue to believe that the first reduction in interest rates will happen in June, and there may be three or four in total during the year.

Due to this, the Euro is declining against all currencies including the Pound, Yen and Swiss Franc. The US Dollar Index on the other hand trades 0.39% higher and is almost trading at a 23-week high. Due to this momentum, the price of the exchange continues to indicate a decline in favor of the US Dollar.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

* Markets weigh risk of retaliation cycle in Middle East. Initially the retaliatory strike from Iran on Israel fostered a haven bid, into bonds, gold and other haven assets, as it threatens a wider regional conflict.

* However, this morning, Oil and Asian equity markets were muted as traders shrugged off fears of a war escalation in the Middle East. Iran said “the matter can be deemed concluded”, and President Joe Biden has called on Israel to exercise restraint following Iran’s drone and missile strike, as part of Washington’s efforts to ease tensions in the Middle East and minimize the likelihood of a widespread regional conflict.

* New US and UK sanctions banned deliveries of Russian supplies, i.e. key industrial metals, produced after midnight on Friday. Aluminum jumped 9.4%, nickel rose 8.8%, suggesting brokers are bracing for major supply chain disruption.

Financial Markets Performance:

* The USDIndex fell back from highs over 106 to currently 105.70.

* The Yen dip against USD to 153.85.

* USOIL settled lower at 84.50 per barrel and Gold is trading below session highs at currently $2357.92 per ounce.

* Copper, more liquid and driven by the global economy over recent weeks, was more subdued this morning. Currently at $4.3180.

Market Trends:

* Asian stock markets traded mixed, but European and US futures are slightly higher after a tough session on Friday and yields have picked up.

* Mainland China bourses outperformed overnight, after Beijing offered renewed regulatory support. The PBOC meanwhile left the 1-year MLF rate unchanged, while once again draining funds from the system.

* Nikkei slipped 1% to 39,114.19.

* On Friday, NASDAQ slumped -1.62% to 16,175, unwinding most of Thursday’s 1.68% jump to a new all-time high at 16,442. The S&P500 fell -1.46% and the Dow dropped 1.24%. Declines were broadbased with all 11 sectors of the S&P finishing in the red.

* JPMorgan Chase sank 6.5% despite reporting stronger profit in Q1. The nation’s largest bank gave a forecast for a key source of income this year that fell below Wall Street’s estimate, calling for only modest growth.

* Apple shipments drop by 10% in Q1.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stocks and currencies sell off; USD up.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* Stocks and currencies sell off, while the US Dollar picks up haven flows.

* Treasuries yields spiked again to fresh 2024 peaks before paring losses into the close, post, the stronger than expected retail sales eliciting a broad sell off in the markets.

* Rates surged as the data pushed rate cut bets further into the future with July now less than a 50-50 chance.

* Wall Street finished with steep declines led by tech. Stocks opened in the green on a relief trade after Israel repulsed the well advertised attack from Iran on Sunday. But equities turned sharply lower and extended last week’s declines amid the rise in yields.

* Investor concerns were intensified as Israel threatened retaliation.

* There’s growing anxiety over earnings even after a big beat from Goldman Sachs.

* UK labor market data was mixed, as the ILO unemployment rate unexpectedly lifted, while wage growth came in higher than anticipated – The data suggests that the labor market is catching up with the recession. Mixed messages then for the BoE.

* China grew by 5.3% in Q1 however the numbers are causing a lot of doubts over sustainability of this growth. The bounce came in the first 2 months of the year. In March, growth in retail sales slumped and industrial output decelerated below forecasts, suggesting challenges on the horizon.

* Today: Germany ZEW, US housing starts & industrial production, Fed Vice Chair Philip Jefferson speech, BOE Bailey speech & IMF outlook.

* Earnings releases: Morgan Stanley and Bank of America.

Financial Markets Performance:

* The US Dollar rallied to 106.19 after testing 106.25, gaining against JPY and rising to 154.23, despite intervention risk. Yen traders started to see the 160 mark as the next Resistance level.

* Gold surged 1.76% to $2386 per ounce amid geopolitical risks and Chinese buying, even as the USD firmed and yields climbed.

* USOIL is flat at $85 per barrel.

Market Trends:

* Breaks of key technical levels exacerbated the sell off. Tech was the big loser with the NASDAQ plunging -1.79% to 15,885 while the S&P500 dropped -1.20% to 5061, with the Dow sliding -0.65% to 37,735. The S&P had the biggest 2-day sell off since March 2023.

* Nikkei and ASX lost -1.9% and -1.8% respectively, and the Hang Seng is down -2.1%.

* European bourses are down more than -1% and US futures are also in the red.

* CTA selling tsunami: “Just a few points lower CTAs will for the first time this year start selling in size, to add insult to injury, we are breaking major trend-lines in equities and the gamma stabilizer is totally gone.” Short term CTA threshold levels are kicking in big time according to GS. Medium term is 4873 (most important) while the long term level is at 4605.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Appetite for risk-taking remains weak.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* Stocks, Treasury yields and US Dollar stay firmed.

* Fed Chair Powell added to the recent sell off. His slightly more hawkish tone further priced out chances for any imminent action and the timing of a cut was pushed out further. He suggested if higher inflation does persist, the Fed will hold rates steady “for as long as needed.”

* Implied Fed Fund: There remains no real chance for a move on May 1 and at their intraday highs the June implied funds rate future showed only 5 bps, while July reflected only 10 bps. And a full 25 bps was not priced in until November, with 38 bps in cuts seen for 2024.

* US & EU Economies Diverging: Lagarde says ECB is moving toward rate cuts – if there are no major shocks.

* UK March CPI inflation falls less than expected. Output price inflation has started to nudge higher, despite another decline in input prices. Together with yesterday’s higher than expected wage numbers, the data will add to the arguments of the hawks at the BoE, which remain very reluctant to contemplate rate cuts.

* Canada CPI rose 0.6% in March, double the 0.3% February increase BUT core eased. The doors are still open for a possible cut at the next BoC meeting on June 5.

* IMF revised up its global growth forecast for 2024 with inflation easing, in its new World Economic Outlook. This is consistent with a global soft landing, according to the report.

Financial Markets Performance:

* USDJPY also inched up to 154.67 on expectations the BoJ will remain accommodative and as the market challenges a perceived 155 red line for MoF intervention.

* USOIL prices slipped -0.15% to $84.20 per barrel.

* Gold rose 0.24% to $2389.11 per ounce, a new record closing high as geopolitical risks overshadowed the impacts of rising rates and the stronger dollar.

Market Trends:

* Wall Street waffled either side of unchanged on the day amid dimming rate cut potential, rising yields, and earnings. The major indexes closed mixed with the Dow up 0.17%, while the S&P500 and NASDAQ lost -0.21% and -0.12%, respectively.

* Asian stock markets mostly corrected again, with Japanese bourses underperforming and the Nikkei down -1.3%. Mainland China bourses were a notable exception and the CSI 300 rallied 1.4%, but the MSCI Asia Pacific index came close to erasing the gains for this year.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stock markets benefit from Dollar correction.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* Technical buying, bargain hunting, and risk aversion helped Treasuries rally and unwind recent losses. Yields dropped from the recent 2024 highs.

* Asian stock markets strengthened, as the US Dollar corrected in the wake of comments from Japan’s currency chief Masato Kanda, who said G7 countries continue to stress that excessive swings and disorderly moves in the foreign exchange market were harmful for economies.

* US Stockpiles expanded to 10-month high. The data overshadowed the impact of geopolitical tensions in the Middle East as traders await Israel’s response to Iran’s unprecedented recent attack.

* President Joe Biden called for higher tariffs on imports of Chinese steel and aluminum.

Financial Markets Performance:

* The USDIndex stumbled, falling to 105.66 at the end of the day from the intraday high of 106.48. It lost ground against most of its G10 peers. There wasn’t much on the calendar to provide new direction.

* USDJPY lows retesting the 154 bottom! NOT an intervention yet. BoJ/MoF USDJPY intervention happens when there is more than 100+ pip move in seconds, not 50 pips.

* USOIL slumped by 3% near $82, as US crude inventories rose by 2.7 million barrels last week, hitting the highest level since last June, while gauges of fuel demand declined.

* Gold strengthened as the dollar weakened and bullion is trading at $2378.44 per ounce.

Market Trends:

* Wall Street closed in the red after opening with small corrective gains. The NASDAQ underperformed, slumping -1.15%, with the S&P500 -0.58% lower, while the Dow lost -0.12.

* The Nikkei closed 0.2% higher, the Hang Seng gained more than 1.

* European and US futures are finding buyers.

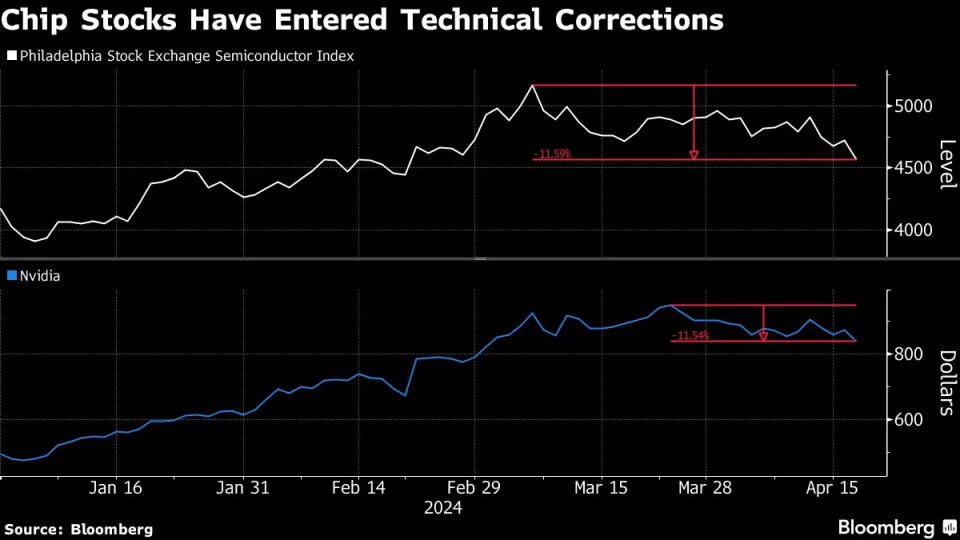

* A gauge of global chip stocks and AI bellwether Nvidia Corp. have both fallen into a technical correction.

* The TMSC reported its first profit rise in a year, after strong AI demand revived growth at the world’s biggest contract chipmaker. The main chipmaker to Apple Inc. and Nvidia Corp. recorded a 9% rise in net income, beating estimates.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The ongoing developments in the Middle East sparked a wave of risk aversion and fueled supply concerns and investors headed for safety. Hopes for imminent rate cuts from the Federal Reserve diminish while attention is now turning towards the demand outlook.

The Gold price hit a high of $2417.89 per ounce overnight. Sentiment has already calmed down again and bullion is trading at $2376.50 per ounce as haven flows ease. Oil prices initially moved higher as concern over escalating tensions with the WTI contract hit a session high of $85.508 per barrel overnight, before correcting to currently $81.45 per barrel.

Oil Prices Under Pressure Amid Middle East Tensions

Last week, commodity indexes showed little movement, with Oil prices undergoing a slight correction. Meanwhile, Gold reached yet another record high, mirroring the upward trend in cocoa prices.

Once again today, USOil prices experienced a correction and has remained under pressure, retesting the 50-day EMA at $81.00 as we moving into the weekend. Hence, despite the Israel’s retaliatory strike on Iran, sentiments stabilized following reports suggesting a measured response aimed at avoiding further escalation. Brent crude futures witnessed a more than 4% leap, driven by concerns over potential disruptions to oil supplies in the Middle East, only to subsequently erase all gains. Similarly with USOIL, UKOIL hovers just below $87 per barrel, marginally below Thursday’s closing figures.

Nevertheless, volatility is expected to continue in the market as several potential risks loom:

* Disruption to the Strait of Hormuz: The possibility of Iran disrupting navigation through the vital shipping lane, is still in play. The Strait of Hormuz serves as the Persian Gulf’s primary route to international waters, with approximately 21 million barrels of oil passing through daily. Recent events, including Iran’s seizure of an Israel-linked container ship, underscore the geopolitical sensitivity of the region.

* Tougher Sanctions on Iran: Analysts speculate that the US may impose stricter sanctions on Iranian oil exports or intensify enforcement of existing restrictions. With global oil consumption reaching 102 million barrels per day, Iran’s production of 3.3 million barrels remains significant. Recent actions targeting Venezuelan oil highlight the potential for increased pressure on Iranian exports.

* OPEC Output Increases: Despite the desire for higher prices, OPEC members such as Saudi Arabia and Russia have constrained output in recent years. However, sustained crude prices above $100 per barrel could prompt concerns about demand and incentivize increased production. The OPEC may opt to boost oil output should tensions escalate further and prices surge.

* Ukraine Conflict: Amidst the focus on the Middle East, markets overlooking Russia’s actions in Ukraine. Potential retaliatory strikes by Kyiv on Russian oil infrastructure could impact exports, adding further complexity to global oil markets.

Technical Analysis

USOIL is marking one of the steepest weekly declines witnessed this year after a brief period of consolidation. The breach below the pivotal support level of 84.00, coupled with the descent below the mid of the 4-month upchannel, signals a possible shift in market sentiment towards a bearish trend reversal.

Adding to the bearish outlook are indications such as the downward slope in the RSI. However, the asset still hold above the 50-day EMA which coincides also with the mid of last year’s downleg, with key support zone at $80.00-$81.00. If it breaks this support zone, the focus may shift towards the 200-day EMA and 38.2% Fib. level at $77.60-$79.00.

Conversely, a rejection of the $81 level and an upside potential could see the price returning back to $84.00. A break of the latter could trigger the attention back to the December’s resistance, situated around $86.60. A breakthrough above this level could ignite a stronger rally towards the $89.20-$90.00 zone.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The NASDAQ Gains As Earnings Gain Momentum, But More Bad News For Tesla.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* Investors turn their attention to the “magnificent seven” and earnings reports as the countdown begins.

* The NASDAQ and most global indices trade higher on Monday with the NASDAQ leading gains. Investors concentrating on earnings from Meta, Microsoft, Alphabet and Tesla.

* Tesla announces it will slash its prices once again as sales decline. The stock trades almost 41% lower in 2024.

* The Euro gains momentum as the European Cash Open nears and is the best performing G7 currency of the day so far.

USA100 – Earnings Season Gains Momentum, More Bad News for Tesla

Last week the NASDAQ’s decline marked the worst week since November 2022, but the price trades higher on Monday. Currently the NASDAQ is the best performing global index, but its performance will largely be dependent on earnings.

So far, technical analysis is still indicating a downward trend and continues to form higher lows as well as highs. The asset also continues to trade lower than the main trend lines, Moving Averages and in the “sell” zone of the RSI. Based on the past 3 retracements, the average retracement size is 1.41%, which means similar retracements could see the price rise a further 0.42%. If the price rises above this level or above $17,234 (Fibonacci retracement 60.0 level), the possibility of a correction or new trend rises.

The question for investors is if the market will take advantage of the lower price to better their entry. This will depend on the upcoming earnings data. This week’s most influential reports for the NASDAQ are:

* Tesla – Tuesday After Market Close

* Meta – Wednesday After Market Close

* Microsoft – Thursday After Market Close

* Alphabet – Thursday After Market Close

The most influential reports will be Microsoft and Alphabet which have the highest “weights” within the index. Tesla on the other hand continues to worry shareholders and CEO Musk cancelled a trip to India over the weekend due to an urgent meeting at Tesla. The company advised they would reduce their workforce by 10% and cut the prices of certain products. Tesla is the NASDAQ’s ninth most influential stock. If earnings and revenue fall short of already subdued expectations, there is a strong chance for the stock price to potentially further decline.

For this reason, the performance of the price movement is likely to depend more on the above upcoming earnings data. If earnings are better than expectations, the index may attempt a correction. Otherwise, investors may see little reason to further expose to that market. If the price drops below $17,102.03, the price action would continue to follow the bearish trend pattern.

EURUSD – Reverting Price Conditions

The Euro is one of the better performing currencies of the day so far, but investors remain concerned about the ECB’s monetary policy. The exchange rate continues to follow a reverting price pattern with the average price at 1.06441. The price currently maintains a “neutral” signal as the price trades at the 75-Bar EMA and slightly above 50.00 on the RSI.

The main price drivers for the Euro over the next 24 hours will be the ECB President’s Speech this evening and tomorrow’s PMI indexes. If President Lagarde continues to advise the Eurozone is close to adjusting interest rates, the currency could come under pressure once more. Also investors will monitor tomorrow’s PMI indexes for the services and manufacturing sector. If the data reads lower than expectations, the Euro again could come under pressure with short term targets at 1.06088.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

European PMIs Paint Mixed Picture, ECB advise a June Cut is Certain.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* The German DAX recorded its highest monthly increase as investors continue to predict a weaker EU monetary policy.

* JP Morgan again advised stocks are overcrowded and may see a stronger downward correction. However, economists advise this is only possible if geo-political tension escalates or companies fail to beat earnings predictions.

* Gold witnesses its strongest decline in 2024 falling 2.64% on Monday and a further 1.32% during this morning’s Asian session.

* The Euro is the best performing currency after the day’s PMI releases. However, investors should note that the US Dollar during the Asian session was performing significantly better.

USA500 – Visa and Tesla Ready Shareholders For Earnings Release!

The SNP500 rose 0.87% during the US trading session and also broke the previous swing high. However, JP Morgan again told journalists there are signs that the stock market is “overcrowded”. When institutions are overexposed to certain stocks or industries, it only takes one big fund to start de-levering and then others will follow.

Though, investors should note that this would also depend on three factors. The first is earnings, the second is geo-political tensions and the third is inflation. This week, investors will largely watch earnings, particularly Visa and Tesla. Visa and Tesla currently hold a weight of 2.00% and are two of the most influential stocks. Tesla continues to be one of the worst performing stocks, but Visa’s earnings are less certain.

Visa has beat earnings and revenue expectations over the past 4 occasions but has been struggling over the past 30 days. Analysts expect earnings and revenue to remain at the same level compared to the previous quarter. However, higher earnings can potentially increase demand. Visa stocks have risen 5.20% in 2024 and have a dividend yield of 0.76%.

However, as mentioned above, the performance of the stock market will largely depend also on inflation and geo-political tensions. Though these are not likely to change within the upcoming days. In regard to inflation, investors will be eager to see if inflation again rises, in which case, interest rate cuts will likely not be possible for 2024. If this scenario materialises, stocks can decline between 20-30% ($3,700-$4,220).

GER30 – ECB Ready To Cut Rates In June 2024!

On a 2-hour timeframe the price of the GER30 is trading above the 75-Bar EMA and above the VWAP. In addition to this, the asset is obtaining buy signals also from oscillators and price action. The index has retraced since the release of the European PMI data, but if the price rises above 18,067, without breaking the day’s low price, buy signals will become active.

One of the key drivers, along with this morning’s PMI release for Germany and France, is the latest comments from members of the ECB. According to ECB representative Mr Villeroy, even if oil remains volatile, the regulator will look to cut in June 2024. In addition to Mr Villeroy, Mr De Guindos told journalists that a rate cut in June is “crystal clear”. The guidance given is increasing the demand for the German DAX as are indications of stronger economic data.

The French PMI data saw the Services index rise above 50.00 for the first time since May 2023 and beat expectations. However, the manufacturing index continues to struggle and fell compared to the previous month. The German PMI was a similar picture. The Services PMI rose to a 10-month high and beat expectations, but the Manufacturing Index read lower than the 42.8 expectations and is at a 6-month low.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stock markets strengthen as tech rally widens.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* The bulls are back in town for now. Wall Street climbed, led by tech and especially the Magnificent 7 — all cohorts rallied, even Tesla which broke a 7-session losing streak even as its earnings news was awaited.

* US: The weaker than expected PMI data from S&P Global was the excuse needed to underpin a short covering rally in Treasuries after the big selloff in April.

* Record US Auction boosted demand! A well bid 2-year sale also added to the gains in Treasuries, while signs of future price pressures saw the long end underperform. Demand petered out into the finish, however, especially with the surge on Wall Street, and yields edged off their lows.

* Australia: The hot inflation print pointed to sticky local price pressures and reinforced the case for the RBA to hold rates at a 12-year high. The CPI rose to 3.6% y/y VS 3.5% estimate, while core CPI rose 4%, also higher than forecast and well above the RBA’s 2-3% target.

* Japan: Strong warning for intervention by officials. The BoJ is widely expected on Friday to leave policy settings & bond purchase amounts unchanged.

* NEW YORK (AP) — The Biden administration has finalized a new rule set to make millions more salaried workers eligible for overtime pay in the US.

Financial Markets Performance:

* The USDIndex slumped, falling to 105.39 largely on profit taking and as haven demand faded.

* USDJPY flirts with 155 after FM Suzuki issued the strongest warning to date on the chance of intervention, saying last week’s meeting with US and South Korean counterparts had laid the groundwork for Tokyo to act against excessive Yen moves.

* AUDUSD up for a 3rd day in a row, to 0.6528 amid a broadly weaker USD but also a strong Aussie post a hot inflation print.

* USOIL steady at $83 ahead of sanctions against Iran and shrinking US Inventories.

* Gold closed slightly lower at $2332, but off yesterday’s $2289 nadir.

Market Trends:

* The NASDAQ increased 1.59%, with the S&P500 up 1.20%, while the Dow rallied 0.69%. Dissipating geopolitical risks also supported.

* EU stock futures are posting gains, after a largely stronger close across Asia. Nikkei and Hang Seng gained more than 2% amid a strengthening tech rally. Australian shares underperformed.

* Tesla Inc. (+13.33% after hours) spiked after its statement for the launch of more affordable vehicles despite a sales miss. The stock halted a 7-day plunge, climbing alongside other members of the group.

* Microsoft Corp., Meta Platforms Inc. and Alphabet Inc. are also due to report earnings this week. Profits for the “Magnificent Seven” group — which also includes Apple Inc., Amazon.com Inc. and Nvidia Corp. — are forecast to rise about 40% in the Q1 a year ago, according to Bloomberg Intelligence data. The group of tech megacaps is crucial to the S&P 500 since the companies carry the heaviest weightings in the benchmark.

* Visa revenue advanced by 17% as Consumer Card spending increased.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!