Market Update – August 29 – Stock markets supported by China hopes and falling yields.

Trading Leveraged Products is risky

Treasuries and Wall Street rallied to kick off the last week of the month for what’s been a pretty bearish August. The same stands so far today. Rate hike fears amid a “higher for longer” policy stance, supply concerns, worries over spillover from slowing growth from China, mixed earnings, and fading AI enthusiasm helped knock bonds and stocks lower through August. But with yields having climbed to 16-year highs and much of the threat from still-hawkish monetary policy priced in, shorts covered and dip buyers emerged.

Treasury yields declined across tenors, with the 2-year dropping to slightly below 5%. The auctions of 2- and 5-year Treasury notes Monday drew the highest yields since before the 2008 financial crisis, a reflection of the US bond-market selloff that deepened last week in anticipation of another rate increase by the Federal Reserve. This is the first 5% handle and the highest award rate since July 2006.

This morning, the Japan unemployment rate for July came in higher than expected & German GfK consumer confidence dropped to the lowest level since May. Pessimists far outnumber optimists and the full breakdown, which is only available until August, showed that the assessment of income expectations deteriorated markedly. Not a positive report and the disappointing numbers tie in with the weakness in business confidence readings. Overall GDP growth is expected to contract this year and political headlines at home are not helping to lift the mood. The ECB seems to be expecting a soft landing though, so those numbers don’t necessarily mean that the ECB will pause next month, as the hawks seem to favor getting any additional hikes that may be needed out of the way.

*FX – USDIndex weakened against the G10 and dipped to 103.73 overnight, EURUSD spiked to 1.0837 (strong resistance area at 1.0840) , GBPUSD holds gains at 1.2617 and USDJPY sideways at 146.27-146.75. – Goldman sees Yen falling to 1990 levels if BOJ stays dovish!

*Stocks – The US100 advanced 0.84%, with the US500 up 0.63% on broadbased gains. Of note, this is the first back-to-back gain for August. The US30 was up 0.62%. NVDA +1.78%, Alphabet +0.87%, 3M +5.22%, GS +0.84%, DIS +0.96%, AAPL +0.88%, AMD +0.35%. European stocks made a positive start today, tracking positive momentum around the world.

*Commodities – USOil up by 0.35% to $79.55.

*Gold – rose 0.2% to $1,925.75.

*BTCUSD rose 0.3% to $26,054.53, ETHUSD rose 0.2% to $1,649.81.

Today: US Housing Price Index, Jolts & Consumer Confidence.

Interesting Mover: EURAUD (-0.26%) broke below 1.6800, with a bearish cross of 10- and 20-period EMA extending lower.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 30 – Data bring Joy, for now?

Trading Leveraged Products is risky

Weaker than expected consumer confidence and JOLTS numbers helped diminish Fed rate hike risks which in turn underpinned strong gains in Treasuries, Wall Street & the Asian stock market today as the markets clawed back some of the hefty losses in August also on speculation that the Fed is nearing the end of the tightening cycle. The USDIndex slumped on the less hawkish Fed outlook. Short and intermediate Treasuries outperformed with yields dropping about 12 bps. The break of technical levels and another solid note auction added to the bullish momentum. The 2-year rate fell to a low of 4.865% but closed at 4.879%. The 5-year richened to 4.26%. The 10-year was at 4.10%. These are the lowest rates in about 2 weeks after recently hitting new cycle highs of 5.08%, 4.48%, and 4.34%, respectively, the cheapest in about 16-17 years. The curve bull disinverted to -76 bps from -84 bps Monday.

German import price inflation at the start of the session is also helping to bolster speculation of a pause from the ECB, especially after a round of dismal confidence readings.

*FX – USDIndex slumped to 103.28 on the less hawkish Fed outlook, currently at 103.48. This broke two straight days over the 104 mark for the first time since June 6-7. Central bank differentials will be important for the Greenback, and it could find some footing if JPY and CNY remain weak. EURUSD spiked to 1.0890 (above the 2-week channel), GBPUSD steady at 1.2640 and USDJPY retested 147.45 but turned quickly lower at 145.77.

*Stocks – Mega-caps climbed after a tough August. The US100 surged 1.74%, while the US500 advanced 1.45%, with the US30 up 0.85%. Gains were broadbased but paced by communication services, consumer discretionary, and IT. The US500 rose for a third straight session, the first time since the end of July. And it broke resistance at 4440 to extend the move to 4495.

*Nvidia jumps by 4.16% as Google AI Alliance expands. Disney at 9-year lows.

*Commodities – USOil higher through the session, rallying 1.3% to $81.33, the highest in over a week, on a combination of factors:

1. Overnight reports of a fresh round of stimulus from China helped support the demand outlook.

2. The advance has been boosted by the advent of Hurricane Idalia which is threatening supply as shipping is halted and some terminals are closed.

3. DOE reported Cushing stockpiles declined -1.9 mln barrels, near January lows.

4. The drop in Treasury yields & the USD are also underpinning.

5. On the other side of the coin, China’s biggest refiner Sinopec said product demand growth is expected to slow in 2H.

*Gold – spiked to $1,938. Gold is likely to remain resilient, with any dip likely to attract buyers. Lisa Shalett, chief investment officer at Morgan Stanley Wealth Management, said in a note yesterday that “regarding the intermediate outlook, we are buyers of gold on weakness or declines in rates”, and others are likely to take a similar stance.

*BTCUSD rose 5.32% and is currently settled at 27,354.

Today: US ADP and Preliminary GDP Price Index in focus.

Key Mover: USOIL (+0.54%) extended more than 50% of August downleg, with next key restistance levels at 81.60 and 82.30.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 31 – Markets sustain the “Bad News Is Good News” stance.

Trading Leveraged Products is risky

Asian stock markets traded mixed overnight, with mainland China bourses underperforming. Chinese manufacturing contracted in August for a 5th straight month, while Chinese property stocks fell after Country Garden, once the country’s largest developer by sales, reported record losses and China Vanke cancelled a share placement. China’s property sector is dealing with a renewed liquidity crisis. Country Garden on Wednesday reported a $7bn first-half loss, its worst ever. European stock futures are higher, also helped by upbeat reports from UBS. French inflation numbers were much higher than anticipated.

German retail sales disappointed again. Sales dropped -0.8% m/m in July. Expectations had been for a slight rise, after the two consecutive months of contraction. Consumer confidence also deteriorated again in data released yesterday, and high inflation and rising debt financing costs are still curtailing consumption.

*FX – USDIndex recovered to 103.25 from 102.84 lows, EURUSD turned to 1.0889 from 1.0949, GBPUSD steady at 1.2700 and USDJPY lifted to 146.30 with the Yen still close to the weakest level in over nine months as markets continue to test the resolve of officials to keep the currency underpinned.

*Stocks – The US100 surged 1.74%, while the US500 advanced 1.45%, with the US30 up 0.85%. The US500 rose for a 4th straight session, the first time since the end of July. And it broke resistance at 4440 to extend the move to 4495. UBS reports huge 2Q profit skewed by Credit Suisse takeover, foresees $10B in cost cuts.

*Commodities – USOil sideways at 81.44 failing o break the 61.8% Fib. level from the August downleg.

*Gold – Spiked to $1,949.

Today: Eurozone CPI readings are likely to surprise on the upside, which will boost rate hike bets. Also the July income, consumption, and PCE deflator numbers will be scrutinized, along with weekly jobless claims.

Key Mover: XAUEUR (+0.51%) retests 2-month Supply Zone at 1785-1795.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 1 – The Calm Before the Storm?

Trading Leveraged Products is risky

The markets were quiet on the last day of August, awaiting the key jobs report today. Treasuries and the US Dollar were firmer, but off their best levels, while Wall Street closed mixed. Ongoing expectations that the FOMC can pause, or is done with rate hikes continued to support along with the lingering impact from the dovish JOLTS result, the cooling in ADP, and the downward revision to Q2 GDP. Income numbers were in line with expectations, including the pick up in y/y inflation metrics, and hence did not hurt the optimistic Fed outlook. The drop in jobless claims was also overlooked. Month-end buying also supported.

Asian stock markets traded mixed, with Hang Seng and ASX struggling, while JPN225 and CSI 300 nudged higher. Futures are posting fractional gains in Europe and the US, although the US100 is struggling. The 10-year Treasury yield is up 0.4 bp as the all important US jobs report comes into view.

*FX – USDIndex recovered Wednesday’s losses and is currently settled at 103.71, EURUSD turned down to 1.0830, GBPUSD pulled back to 1.2650. Both EUR and Sterling corrected today as markets reined in tightening expectations for BoE and ECB, with yields dropping across the board and Eurozone spreads coming in. US data added further support for the USD as markets assess the interest rate outlook.

*Stocks – Wall Street gave up its gains and faded into the close, leaving the US30 and US500 down -0.48% and -0.16%, respectively, breaking a string of four straight days of gains. The US100 was up 0.11%, higher for a fifth consecutive session.

*Commodities – USOil prices have extended gains with WTI now up 1.9% to $83.65 and Brent 1.25% firmer at $87.15. This is a sixth consecutive session of gains on WTI, the best run since the start of the year. Along with the signs of a still robust US economy, indication of more stimulus from China, and declining stockpiles, Bloomberg reports that Russia has agreed with OPEC+ to extend output cuts. Also, the impacts from Hurricane Idalia are still being assessed.

Key Mover: USOil & UKOIL have extended gains by 1.9% to $83.65 and 1.25% to $87.15 respectively as Bloomberg reported Russia has agreed with OPEC+ to extend output cuts.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 4- The first full week of a historically negative month for Stocks and Gold kicks in.

Trading Leveraged Products is risky

First of all a reminder: US and Canadian cash markets will be closed today because of the Labour Day celebration, obviously resulting in diminished flows this afternoon. Going back in chronological order, APAC is led by the excellent performance of the China50 and especially Hong Kong where a surge on real estate stocks helped the indices to add 2.5% and 1.8% respectively. This comes after embattled Country Garden reportedly won approval to extend payments for an onshore Private Bond and is now up 7.9% (just out the wire they are trying to get financing in Malaysian Ringgit); the overall Mainland Properties Index is +7.32%. This week there will be important data from this hemisphere with the RBA rate decision and the Chinese trade balance.

Friday’s NFP figure was slightly better than expected (+187k vs +170k expected) but at the same time the previous two readings were revised downwards by 100k, while the unemployment rate surprisingly jumped to 3.8% (3.5% expected) also as a result of an increase in labour force participation (62.8% vs 62.6%). There are more people seeking employment and this is probably one of the factors that led to a fractional decrease in Average Hourly Earnings. Overall, we emerge from the week with the impression that the labour market is finally starting to slow down.

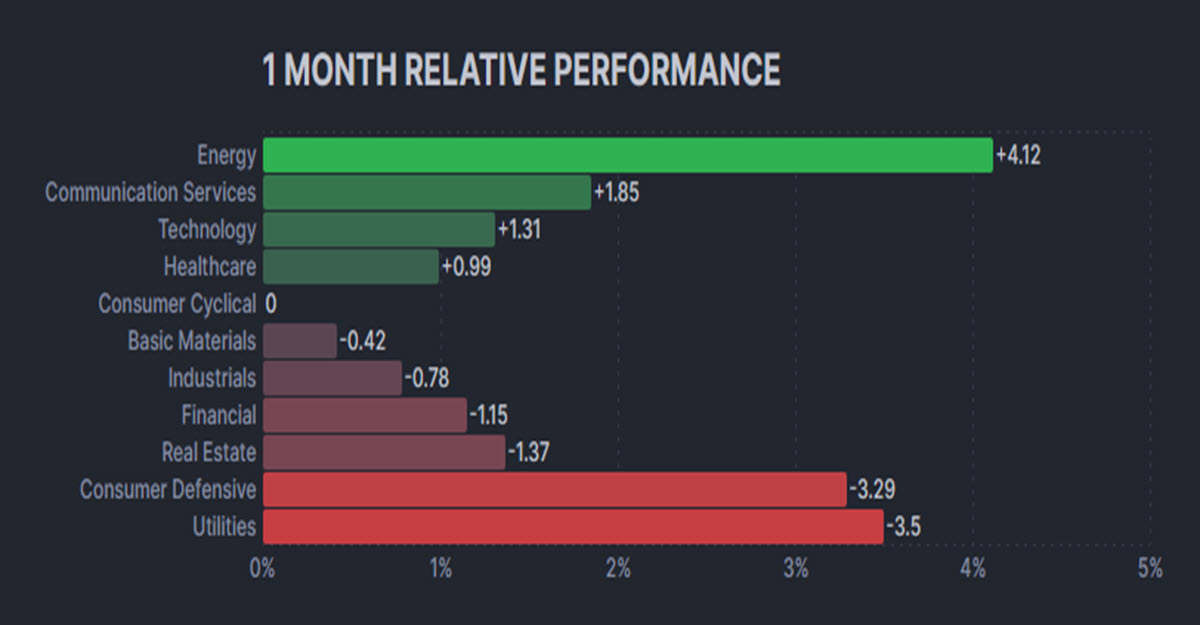

Relative Performances by Sector, August

Yields and USD reacted by plummeting shortly after the data, before totally reverting the move and ending the day up; the long-end has experienced the heavier selling pressure, resulting in the curve steepening.

Crude oil soared again (+2.30%) with the EIA and API data showing considerable pressure on stocks during the week probably due to the effect of several months of production cuts. At the same time, Copper hit $390 before sellers emerged, adding to its 6.50% rally since mid August on decent Chinese Manufacturing data.

*FX – USDIndex recovered 104 (104.09 now), EURUSD turned below 1.08 (1.07865, GBPUSD just north of 1.26 (1.2609). USDJPY sits above 146 once again, USDCNH 7.2667.

*Stocks – US30 closed higher on Friday and notched its best week since July. US500 +0.2%, US100 -0.02% but still up +3.67% on the week. In Europe GER40 closed -0.6%, CAC40 – 0.29%.

*Commodities – USOil is digesting last Friday’s rally, now -0.61% at $85.48, the spread against UKOil has reduced to $2.97. Copper flat at $385 after sellers emerged at $390 on Friday.

*Gold – still hovering around $1940, XAG pulled back powerfully from $25 ($24.18 now).

LATER TODAY: German Trade Balance, Switzerland GDP, EU Sentix confidence, ECB’s Lagarde speech

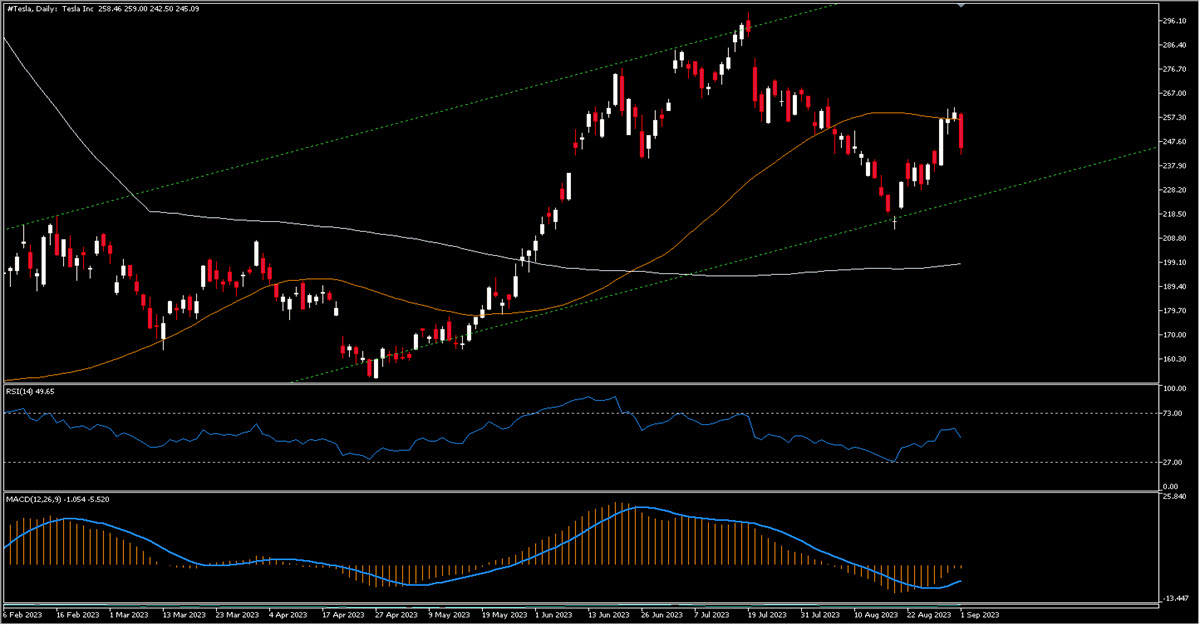

INTERESTING MOVER: TESLA -5.06% at $245.01 after lowering the US prices of its Model S and X for the seventh time in 2023, now $30k and $40k respectively cheaper than at the beginning of the year. The price was rejected by the 50MA and the MACD is negative.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 5 – RBA on hold, Chinese services deteriorate after a Monday without US lead

.

Trading Leveraged Products is risky

First of all a reminder: US and Canadian cash markets will be closed today because of the Labour Day celebration, obviously resulting in diminished flows this afternoon. Going back in chronological order, APAC is led by the excellent performance of the China50 and especially Hong Kong where a surge on real estate stocks helped the indices to add 2.5% and 1.8% respectively. This comes after embattled Country Garden reportedly won approval to extend payments for an onshore Private Bond and is now up 7.9% (just out the wire they are trying to get financing in Malaysian Ringgit); the overall Mainland Properties Index is +7.32%. This week there will be important data from this hemisphere with the RBA rate decision and the Chinese trade balance.

Friday’s NFP figure was slightly better than expected (+187k vs +170k expected) but at the same time the previous two readings were revised downwards by 100k, while the unemployment rate surprisingly jumped to 3.8% (3.5% expected) also as a result of an increase in labour force participation (62.8% vs 62.6%). There are more people seeking employment and this is probably one of the factors that led to a fractional decrease in Average Hourly Earnings. Overall, we emerge from the week with the impression that the labour market is finally starting to slow down.

Relative Performances by Sector, August

Yields and USD reacted by plummeting shortly after the data, before totally reverting the move and ending the day up; the long-end has experienced the heavier selling pressure, resulting in the curve steepening.

Crude oil soared again (+2.30%) with the EIA and API data showing considerable pressure on stocks during the week probably due to the effect of several months of production cuts. At the same time, Copper hit $390 before sellers emerged, adding to its 6.50% rally since mid August on decent Chinese Manufacturing data.

*FX – USDIndex recovered 104 (104.09 now), EURUSD turned below 1.08 (1.07865, GBPUSD just north of 1.26 (1.2609). USDJPY sits above 146 once again, USDCNH 7.2667.

*Stocks – US30 closed higher on Friday and notched its best week since July. US500 +0.2%, US100 -0.02% but still up +3.67% on the week. In Europe GER40 closed -0.6%, CAC40 – 0.29%.

*Commodities – USOil is digesting last Friday’s rally, now -0.61% at $85.48, the spread against UKOil has reduced to $2.97. Copper flat at $385 after sellers emerged at $390 on Friday.

*Gold – still hovering around $1940, XAG pulled back powerfully from $25 ($24.18 now).

LATER TODAY: German Trade Balance, Switzerland GDP, EU Sentix confidence, ECB’s Lagarde speech

INTERESTING MOVER: TESLA -5.06% at $245.01 after lowering the US prices of its Model S and X for the seventh time in 2023, now $30k and $40k respectively cheaper than at the beginning of the year. The price was rejected by the 50MA and the MACD is negative.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 6 – Saudis, Russia extend voluntary production cuts.

Trading Leveraged Products is risky

US stocks fell on Tuesday – with the exception of the US100 – weighed down by higher oil prices and rising Treasury yields. Saudi Arabia will extend its 1 million barrel per day voluntary oil production cut until the end of the year, according to the state-owned Saudi Press Agency, and the cut adds to the 1.66 million barrels per day that other OPEC members have put in place until the end of 2024. Russia, through its Deputy Prime Minister Novak, also pledged to extend its 300k bpd cuts until the end of December, and will review the measure on a monthly basis. UKOil traded above $90 till a few minutes ago (now $89.84) and USOil went as high as $88 at some point yesterday. This was immediately reflected firstly in US yields, which rose 6bps on the 10-year, and the USD also benefited. The phantom of inflation may not yet be vanquished with the main raw material of our energy-intensive societies rising by 30% in just over two months. Stocks have fallen: airline and cruise stocks obviously suffered but all sectors except Energy, Technology and Consumer discretionary went down. European indices also dropped as economic data for the region came in mixed. Eurozone producer prices fell 7.6% in July from a year ago. But business activity in August dropped at the steepest rate in nearly three years. Overnight the Australian GDP figure showed a slowdown compared to the previous quarter, but was less marked than expected.

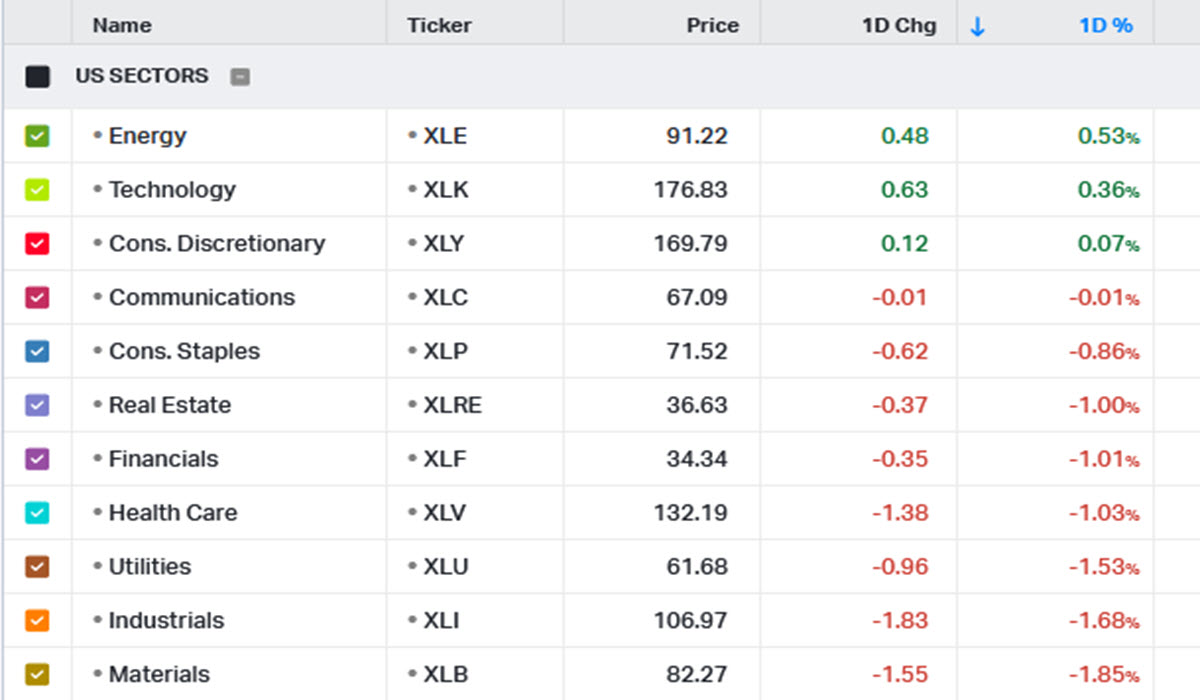

Sectorial Etf Performances

*FX – USDIndex hit its highest level since 10 March, now at 104.64. USDJPY at 2023 highs, 147.08 now but traded as high as 147.815. USDCNH slides to 7.31 but previously touched 7.325. EURUSD -0.61% at 1.0737 now close to critical levels, GBPUSD at 1.2581 with its price clearly below a trendline.

*Stocks – Flattish Chinese indices, JPN225 +0.77% at 33227, AUS200 -0.75%. US Futures all aligned at -0.07% right now, EU Futures -0.2%/-0.3%. Yesterday Materials -1.85%, Industrials -1.68%, Utilities -1.22%.

*Commodities – USOil touched $88.05, trading at $86.50 right now; UKOil rose as high as $91.12 now at $89.83.

*Gold – pressured again, -0.56% yesterday now flat at $1926. XAG dropped -1.67%, further down -0.33% at $23.45 now.

LATER TODAY: Germany Factory Orders, EU Retail Sales, US Trade Balance, PMIs, Bank of Canada Interest Rate decision, Fed Beige Book.

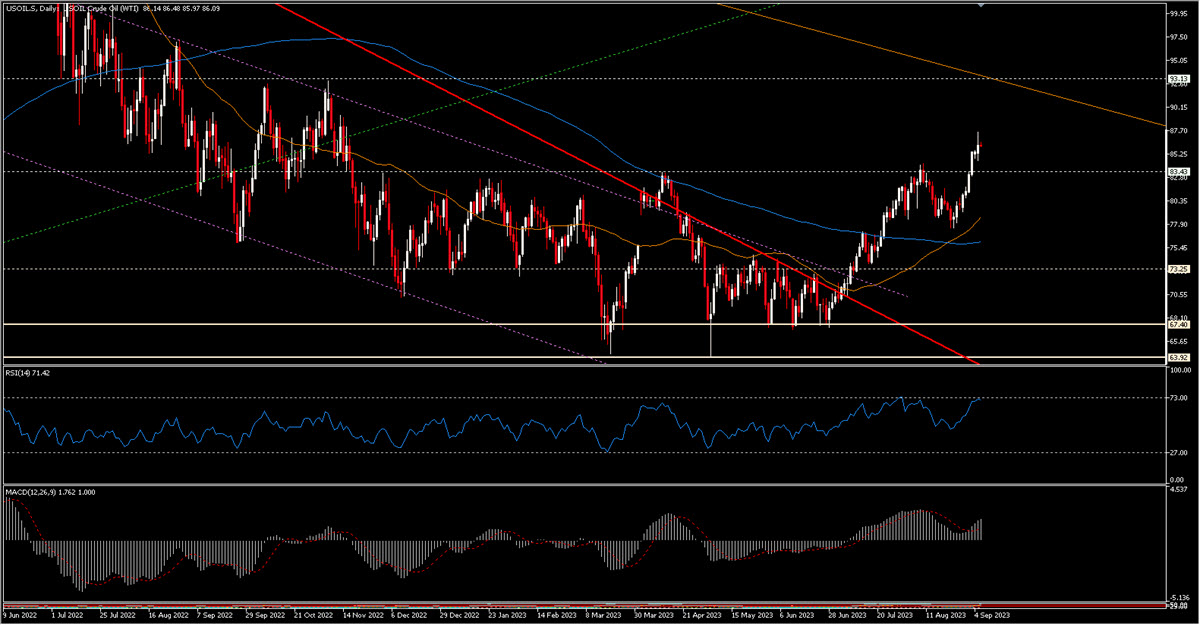

INTERESTING MOVER: USOil added another +0.84% ($86.7) to its more than 2 month long 30% rally. Resistances at $88.5/$89 and $92.5/$93 areas, support in the $83.5/$84 area. MACD, RSI positive, Price above 50d-200d MAs that recently crossed to the upside.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 7 – Futures negative on Oil, rates rise, weak data; EU GDP ahead.

Trading Leveraged Products is risky

European markets are heading for a lower open today (Thursday) with investors looking ahead to the Q2 GDP and employment change over the same period. Data continues to come in very weak from Germany where Industrial Production just showed a further decline after Factory Orders plummeted again yesterday (-11.7% m/m). This also plays a role in last night’s weak Chinese imports data, which declined again -7.3% y/y, although this was less than expected. Exports also contracted and to stay within the same region, the Australian Trade Balance deteriorated by about 2 billion in July. Yesterday the BOC left rates unchanged at 5% while the FED’s Beige Book saw an unusual abuse of the word ”recession” (used 15 times), despite it having clearly disappeared from the last corporate earnings reports.

Equity markets are weak while Rates and USD keep going higher. The Chinese have given up defending their onshore FX exchange rate (CNY) and it has broken above recent highs. Oil is unstoppable on the back of recent news and apparent supply shortage. EU GDP is expected to have been positive in Q2 (+0.3%) and also on a yearly basis (+0.6%). US Jobless claims will give us new insight into the labour market which seems to have slowed down as per last week’s data.

*FX – USDIndex +0.05% at 104.87, USDJPY touched 147.87, now -0.14% at 147.47, USDCNH 7.329, Cable – 0.07% and < 1.25, AUDUSD +0.11% @ 0.6387.

*Stocks – EU Futures -0.3% (both GER40 and FRA40), US30 -0.20%, US100 -0.34%, AAPL, NVDA >-3% yesterday.

*Commodities – USOil giving up some of the recent gains but still close to recent highs, -0.43% @ $87.18, UKOil trades @ $90.26.

*Gold – $1917,83, mainly flat. XAG leads the way, -0.47% at $23.06.

LATER TODAY: EU Q2 employment change, EU Q2 GDP, US Jobless claims, FED’s Williams, Bostic, Bowman, BOC’s Governor speech.

INTERESTING MOVER: GBPUSD (-0.26% this morning @ 1.2475) remains heavier than other peers, has broken recent lows and is heading toward 1.2440 support, 200MA at 1.2430, weak RSI, Negative MACD.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 8 – Japanese & EU GDP miss, CNH breaks 2023 lows.

Trading Leveraged Products is risky

Asia-Pacific markets were lower on Friday as Japan released revised second quarter gross domestic product figures (+1.2% vs +1.3% expected, down from 1.5%) and Hong Kong cancelled the morning trading session due to a storm warning. Overnight the US100 fell for a 4th session, weighed by Apple after a report that China is allegedly banning government workers from using iPhones; NVDA, AMD, Qualcomm slipped as well. US30 managed to edge up 0.17% as defensive sectors outperformed (Utilities the best one). Initial Jobless claims fell to 216k last week, below estimates and hinting to a still tight job market after last week’s streak of data. Unit labor costs rose 2.2% (1.9%). A ”positive” note came from Walmart that announced it is lowering its workers entry pay. EU GDP and employment change in Q2 disappointed yesterday and EU stocks are down for the 7th day in a row. German CPI/HICP is just out, in line (CPI +6.1% y/y).

This morning a poll of 69 economists interviewed by Bloomberg showed that the majority of them (39) are seeing an ECB pause in September, with some odds (33) of a new hike by the end of the year. Finally, USDCNH is trading at 7.3528 and has broken 2023 highs the day after CNY did so, showing the Chinese authorities are giving up protecting the 7.30 barrier.

*FX – USDIndex -0.20% at 104.82 retreated back below 105, EURUSD sits in the low 1.07s, Cable lingers below 1.25 and USDJPY trades on a 147 handle (147.15).

*Stocks – EU Futures +0.3% (both GER40 and FRA40), US30 +0.14%, US100 +0.31%, AAPL – 2.92%, AMD -2.46%, Qualcomm – 7.22%.

*Commodities – USOil -0.36% at $86.43, UKOil loses $90, $89.59 now. Strikes began at Australian Chevron LNG plants.

*Gold – +0.38% at $1926.80, XAG +0.82% at $23.15, Palladium +1.15% at $1228 is trying to rebound from 2023 lows.

LATER TODAY: Canadian Unemployment Rate, Fed’s Bostic & Barr.

INTERESTING MOVER: Apple -2.92% at $177.56 is down -6.54% in 2 sessions on heavy volumes after US-China tech-related tensions arose again. It managed to recover the $176 level after opening at 175.18 and hitting a low at $173.54. The MACD is neutral and RSI slightly below 50. Price is between the MM50 ($186.50) and MM200 ($164).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 11 – BOJ & PBOC Caused Turmoil.

Trading Leveraged Products is risky

G20 wraps up, while in Asia central banks have shaken the markets this morning. Verbal intervention from Japan and China helped to bolster Yuan and Yen and saw the DXY dollar index correcting to 104.637, from a close of 105.09 on Friday. Treasuries fell slightly across tenors Monday as traders await US inflation due later this week. Stock markets had a mixed start to the week, while bonds corrected, as most equity indexes found buyers. This turned USDJPY around, with Yen rallies with Yields after BOJ Ueda comments on negative rates fuelled rate hike speculations. USDCNH collapsed just before hitting last year’s highs – Yuan off 16-year lows after PBoC sets strong reference rate and threatens to punish market disruption.

*FX – USDIndex correcting to 104.45, from a close of 105.09 on Friday, EURUSD turned higher to 1.0730 from 1.0683 lows last week, GBPUSD broke 20-day SMA and still holds above it at 1.2526. Against the weaker US Dollar, the Aussie and the Kiwi were among the biggest beneficiaries, each rising close to 1% to hit roughly one-week highs.

*Stocks – JPN225 correcting -0.4% and the Hang Seng losing more than 1%, the latter in catch up trade, after markets were closed on Friday due to adverse weather conditions. The CSI 300 managed to lift 0.7%, the ASX 0.5%, and futures are higher in Europe and the US.

*Commodities – USOil dips shortlived after technical rally, however it remains above the key $84 level, extending gains above 11-month resistance. Currently settled at $86.56. Gold retests $1930 once again.

TODAY: The European Commission is to release its summer interim economic forecast. The central bank’s chief economist Huw Pill speaks at the Kent Invicta Chamber of Commerce.

Key Movers: USDJPY drifted (-1.18%) after BOJ Governor Kazuo Ueda stated that there may be sufficient information by year-end to judge if wages will continue to rise, which is a key factor in deciding whether to pare back its super-easy policy.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 12 – Greenback rebounds ahead of US Inflation.

Trading Leveraged Products is risky

Wall Street closed slightly higher amid strength in big tech. Tesla climbed 10% after Morgan Stanley boosted its outlook on the stock based on expectations on the impacts of the “Dojo” computer. Treasuries posted small losses amid a lack of buyers. Bloomberg suggested it was the smallest range on the 10-year in over 2 years. The 10-year was up 2.5 bps to 4.295%. It was generally contained by the 4.30% level as well as the 4.34% cycle peak from August 21, the highest since late 2007. Today, European futures are higher, US futures slightly lower, as markets wait for US inflation numbers.

This morning: UK wage growth higher than expected – a bit of a negative surprise for the BoE. The ILO unemployment rate was unchanged, jobless claims nudged up 0.9K in the more up to date August report and the July reading was revised down. Mixed signals for the BoE about the overall situation in the labour market, but it seems payroll growth is slowing, which ties in with survey data from the PMI reports. Despite this, wage growth remains uncomfortably higher and the data would back at least one more rate hike from the BoE this month. BoE’s Mann warns against early end to tightening cycle.

*FX – USDIndex lost a little ground, albeit after 8 straight weeks of gains, currently at its lows at 104.63 from 104.37. EURUSD drifted to 1.0725 from 1.0768 and GBPUSD higher after the data at 1.2529. USDJPY higher at 146.85 but Yen holds yesterday’s gains.

*Stocks – The US100 rallied 1.14% on the back of a surge in big tech. The US500 was 0.67% and the US30 was 0.25% firmer. JPN225 also jumped nearly 1%, but elsewhere across Asia the move higher was muted and China bourses traded narrowly mixed, with the CSI 300 down -0.1% and the Hang Seng rising a mere 0.1%. European futures are higher.

*Disney and Charter gained. Both stocks climbed after reports of a deal to restore channels including ESPN and ABC to the cable operator’s subscribers. Warner Bros. Discovery also rose.

*Nvidia fell. The chipmaker edged lower, extending a rocky September. Advanced Micro Devices also declined. J.M. Smucker shares fell after the snack giant agreed to buy Twinkies owner Hostess.

*Commodities – USOil higher as attention shifts to outlooks from OPEC & US.

*Bitcoin rose after dropping to the lowest since June on Monday

TODAY: The Apple product event, German ZEW Economic Sentiment. OPEC and US EIA will both publish monthly market reports later.

Key Movers: BTCUSD rallied by +2.77% today.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 13 – Stocks retreat as markets wait for CPI.

Trading Leveraged Products is risky

Wall Street succumbed to further profit taking as concerns over tech weighed. This morning, stock markets headed south across Asia, as markets wait for the key US CPI numbers due to be released today. The USDindex tumbled into the close with the index sliding to 104.573 from the day’s high of 104.918 after a Reuters report said the ECB saw inflation holding over 3% in 2024. European and US futures are in the red and yields are moving higher with Eurozone markets underperforming after the Reuters source story.

Today so far: UK GDP contracted -0.5% m/m in July, more than expected and wiping out the 0.5% gain in the previous month. The three month trend rate remained steady at 0.2%. Industrial production contracted -0.7% m/m, services fell -0.5% m/m and construction output declined -0.5% m/m. The visible trade deficit narrowed somewhat, but that will also be due to lower energy prices. Wet weather and strikes are partly to blame, but the numbers also tie in with weaker survey numbers and a wider weakness in activity, with the UK economy set to move essentially sideways over the next quarter, after what was a quicker bounce back from the pandemic than initially reported. For the BoE that means further hikes after the likely move this month seem increasingly less likely.

*FX – USDIndex at 104.742, up from a session low of 104.515. EURUSD dipped to 1.0730 from 1.0764 and GBPUSD retested its 1.2440 low. USDJPY higher at 147.30.

*Stocks – The US100 led the declines with a -1.04% drop, while the US500 fell -0.57% and the US30 slipped -0.04%. A lot of the weakness stemmed from Apple and Oracle with the former hit by more fallout from China’s restrictions on iPhones, while the latter suffered from a poor earnings report. Apple’s iPhone 15 launch did not provide much support.

*Commodities – Oil prices have remained supported ahead of the CPI report and on forecasts by OPEC and the US that output cuts will tighten the market in the months ahead. USOIL is at $88.50.

*Gold has corrected to $1908 as the USDIndex has nudged up from early lows and is starting to eye the 105 mark again, which is keeping a lid on the precious metal, although gold is still up more than 12.5% over the year.

Key Movers: AUDUSD (H1 chart) in a 3-day downchannel with key Resistance intraday at 0.6410 and 0.6420.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 14 – A hotly contested day ahead!

Trading Leveraged Products is risky

CPI was a little hotter than expected, but not enough to alter expectations that the FOMC will skip hiking rates at its meeting next Wednesday. And the report did not change views that the door is open for a tightening in November, but it still not any more than a 50-50 bet. Treasuries went into the CPI data priced for upside risks and Yields spiked on the 0.6% jump in headline and the 0.3% gain in the core, which resulted in respective y/y rates of 3.7% and 4.3%. However, yields quickly dropped back and closed richer on the session amid short covering. Today, Asian stocks inched higher as investors shrugged off stronger than expected US inflation figures and anticipate the ECB decision.

The ECB meeting takes place today with reports that the updated staff projections will push the 2023 inflation forecast above 3% having boosted bets of another 25 bp hike. A hawkish pause would not be a surprise, but we think there is a slightly higher chance that the ECB will move again this week, especially considering the likely upward revision to the inflation forecast and the most recent rise in energy prices.

*FX – USDIndex is at 104.60. EURUSD mixed but lower in EU session at 1.0733 from 1.0754 and USDJPY holds above 147.00 floor, eyeing 148.

*Stocks – The JPN225 surged 1.4% to 33,168.10, US500 edged up to 4534, US100 jumped to August ceiling and the US30 failed to extend above 35k, as Stocks and bonds were supported ahead of ECB and US data.

Stocks of airlines were some of the biggest losers in the US500 after a couple warned of the hit to profits they’re taking because of higher costs. United Airlines sank by 3.8% and 2.8% for Delta Air Lines. On the flipside, Amazon climbed 2.6%, Microsoft gained 1.3%, and Nvidia rose 1.4%. Moderna rallied 3.2% after it reported encouraging results from a flu vaccine trial.

*Commodities – Oil well supported as markets focused on the prospect of sustained supply tightness this year. USOIL is at $88.60, recovering from $87.60 lows.

Today: ECB rate decision & Press Conference, US Retail Sales and PPI.

Key Movers: XAGUSD (-1.18%) broke 5-day range, extending the September’s downleg, with attention turning to 22 and 21 Support level.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Редактировалось: 1 раз (Последний: 14 сентября 2023 в 21:13)

Next week will be one marked by multiple decisions by the world’s major Central Banks, the Fed in the first place. PMI data will then give colour to the expected strength of the economy in the coming months, while we will continue to keep our eyes firmly on prices, after the impromptu rise we saw in the US, for example.

Tuesday – 19 September 2023

->Harmonized / Core Harmonized Index of Consumer Prices (EUR, GMT 09:00) – Next week will be one marked by multiple decisions by the world’s major Central Banks, the Fed in the first place. PMI data will then give colour to the expected strength of the economy in the coming months, while we will continue to keep our eyes firmly on prices, after the impromptu rise we saw in the US, for example.

->Canadian CPI (CAD, GMT 12.30) – Inflation in Canada is at similar levels to the US, even lower: 3.2% and 3.3% in July on the headline and core components respectively. But the former has risen again in the latest report, and consistently from +2.8% in June: will it follow in its neighbour’s footsteps and mark a second consecutive rise? Expectations are for a +3.8% rise in the headline component.

Wednesday – 20 September 2023

->PBoC Interest Rate Decision (CNH, GMT 01:15) – China’s central bank has been very active this year in trying to stimulate the economy with various instruments and has already tweaked various interest rates and margins requirements from banks several times: in August the key one-year loan prime rate was lowered from 3.55% to 3.45% where it now stands. It remains to be seen whether the bank will take a break after the latest vaguely positive data.

->UK CPI, PPI, Retail Price Index (GBP, GMT 06:00) –Prices in the UK continue to grow at the highest levels among advanced economies: in July y/y CPI was +6.8%, Core CPI +6.9%, Retail Prices +9%. The economy seems to be languishing in stagflation but this is not what policy makers would like to see, as they expect to see numbers close to 5% by the end of the year. Expectations are for a rise of the headline component to +7.1% and a slowdown in the core one, to +6.8%, while RPI is forecasted at +9.3% y/y.

->FED Interest Rated Decision and FOMC Press Conference (USD, from GMT 10:00) -Little drama is expected out of next week’s FOMC. The official rate is in the 5.25% – 5.50% range and the market continues to price in very little risk for a hike next week. Chances for a 25 bp rate hike in November are still on the cards amid sticky core inflation and a still tight labor market. Very important will be subsequent comments from the ever-balanced Jerome Powell, who will perhaps explain the bank’s view on prices that have been rising again over the past two months while growth and jobs seem to be holding strong.

Thursday – 21 September 2023

->SNB Interest Rated Decision and Monetary Policy Assessment (CHF, GMT 07:30) –Earlier this month, economists at Credit Suisse/UBS were saying the SNB could raise the current 1.75% level even in the event that the neighboring ECB paused, citing the usual price fight but also the interest rate differential with the eurozone. Instead, Madame Lagarde raised and even though Inflation is actually below 2%, the Swiss bank’s projections suggest caution and that a 25 bps hike could be in the cards.

->BOE Interest Rate Decision, Minutes and Monetary Policy Summary (GBP, GMT 11:00) –SONIA futures data seem to take it for granted that the BOE will raise at this meeting from the current 5.25% to 5.50%: but most important will be to understand the internal divisions and alternatives on the bench for the bank that is perhaps facing the most difficult situation, with a stagnant economy and prices running hot. Economists polled by Reuters think 2 members will vote for keeping the rate unchanged, up from just 1 at the last meeting.

->US Jobless Claims and Existing Home Sales (USD, GMT 12:30, 14:00) –The US labor market has shown that it is still very tight despite some slowdown that was most noticeable in the ADP data and the pickup in the unemployment rate (+3.8% in August from +3.5%), actually due to a rise in the Labor Force Participation Rate. This week, it is expected that Initial Claims will rise by just 5k to +225k. While mortgage demand has sunk to a 28-year low given the high rates, existing home sales are also suffering (+4070k in July down from +4160k in June) in contrast to new home sales, which continue to climb (+714k). Two more data points to see how strong the US locomotive is. Expectations are for 4100k Existing Home Sales.

Friday – 22 September 2023

->BOJ Interest Rated Decision and Monetary Policy Statement (JPY , GMT early morning time, not disclosed) –Yen weakness, a still negative official rate (-0.1%), recent changes to the YCC on the 10-year, Ueda statements, prices and wages that finally seem to be rising consistently toward the bank’s target bring into question whether or not the process of monetary policy normalization from an ultra loose stance has really begun. With the USDJPY in the 148 area, an event definitely not to be missed. No changes are expected for the Official Interest Rate.

->French, German, European HCOB PMIs, UK S&P/CIPS PMIs (EUR, GBP, starting GMT 07:15) – Yen weakness, a still negative official rate (-0.1%), recent changes to the YCC on the 10-year, Ueda statements, prices and wages that finally seem to be rising consistently toward the bank’s target bring into question whether or not the process of monetary policy normalization from an ultra loose stance has really begun. With the USDJPY in the 148 area, an event definitely not to be missed. No changes are expected for the Official Interest Rate.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 18 – Central Banks Week kicks off.

Trading Leveraged Products is risky

A week that will be marked by meetings and decisions of practically all the world’s most important central banks is off to a slow start, with US futures fractionally up (+0.08% / +0.15%) after Friday’s drubbing. It was a decisive day for the weekly trend, sending both the US500 and US100 into negative territory for the second time in a row: only the US30 managed to close the week at +0.1%. The tech sector was the hardest hit, -2.2%, led by the Oracle debacle, -10%. On the other front, Utilities outperformed, +2.8%. This was on Friday, when the Nasdaq sank -1.75% and the US500 posted -1.22%: two factors contributed to this bad performance. First, the Michigan Consumer Sentiment Index, which came out at 67.7, below expectations and well below its historical average, which is close to 86. This Index accounts for 2/3 of the US economy and is therefore a valuable indicator of the overall state of affairs there. The other major event that certainly helped the declines to be heavy was the UAW strike, for the first time simultaneously at the Ford, GM and Stellantis plants: the demands are for wage increases of up to 40% and the impact of such news on the perception of future inflation can be worrying. Today is poor in data, but from tonight Central Banks Week kicks off with the minutes of the latest RBA meeting and from Wednesday night onwards all the big central banks will cascade. The FED decision will be made on Wednesday evening.

Since the 3rd week of August, Antipodeans + CNH have relatively outperformed

*FX – USDIndex -0.12% at 104.86; Antipodeans are relatively stronger with AUDUSD +0.23% and NZDUSD +0.31%, this comes also on the back of USDCNH <7.30 (7.28 now). GBPUSD sits at 1.24, EURUSD +0.13% at 1.0673.

*Stocks – US Futures fractionally higher (US500 + 0.15%, US100 +0.22%, US30 +0.12%); GER40 futures are turning negative right now (-0.03% at 15869), CAC is -0.05%. Last Friday, META and NVDA sunk >-3%, Microsoft -2.50%.

*Commodities – USOil is trading close to 10-month high at $91.60, UKOil puts $95 in sight.

*GOLD – +0.32% at $1929, XAG +0.73% at $23.20.

Today: highlights include US NAHB Housing Market Index, Bundesbank Monthly Report, remarks from Saudi Arabia’s Energy Minister, ECB de Guindos & Panetta.

Key Movers: XAUUSD (+0.22% @ $1928.09) is in a very tight range between its 50d and 200d MAs and close to the upper bound of a descending channel.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 19 – Slow markets before 5 Major Central Banks decisions.

Trading Leveraged Products is risky

US Stocks barely budged yesterday, with all indices ending the session with tiny gains; volumes were muted too. On the other side of the ocean, we witnessed substantial losses among European indices, probably also weighed down by the ECB’s decision last week. The worst of all was the FRA40 after one of the largest domestic investment banks, Societe Generale, pledged to cut costs and tumbled 12.05%. It is not the first major investment bank to make similar pronouncements lately, with Goldman and Morgan Stanley planning to adjust their workforce next.

Back to America, strikes are hitting the economy with 4.1 million labor hours lost in August, the most in 23 years: perhaps another reason why the indices’ rally has come to a standstill with the Nasdaq – for instance – remaining at the level of three months ago. To be fair, yesterday the good performance of Apple and Meta helped it to gain +0.15%. Technology was the best sector for the day, along with Energy: however, it is striking to see how the latter has been the star performer in recent months – led by the oil rally – with the ETF tracking the sector (XLE) up 14.92% in three months versus a paltry +1% for the US500.

The RBA minutes this morning held few surprises and the AUD, like the USD, is little moved. Rates continue to push slowly upwards and the 2-year is close to its March high of 5.066%. The market believes that the Fed will not move tomorrow – 99% odds – but the Dot Plot predicts another hike this year: GS is convinced that this is just a ”bluff”. We shall see.

*FX – USDIndex flat at 104.86; AUDUSD -0.04% @ 0.6433, GBPUSD < 1.24 (1.2377, EURUSD -0.12% @ 1.0679. USDJPY just shy of 148 and USDCNH back at 7.30.

*Stocks – US Futures are inching lower (US500 -0.12%, US100 -0.25%, US30 -0.09%); EU futures are adding to yesterday’s losses. AAPL +1.69%, Square’s and Lonza’s CEOs to depart the companies (latter one -14%), second interesting IPO in a couple of days with Instacart valued $10B, 75% less than the previous Private VC valuation.

*Commodities – USOil +0.08% at $92.27, UKOil hit $95, now trading at $94.69, Wheat, Corn close to 2023 lows.

*GOLD – -0.13% @ $1931.

Today: Highlights include European HICP, Core HICP, US Housing Starts, Canadian CPI.

Key Movers: FRA40 -1.39% @7276 after testing the top of the channel with a perfect spinning top on high volumes, fell hard yesterday led by the slump of one of the largest French banks (SocGen -12%).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 20 – FED will stay on hold; Dot Plot, SEP are key.

Trading Leveraged Products is risky

In a day that will be centred around the Fed’s deliberations this evening, and above all the quarterly economic projections, the new dot plot and Jerome Powell’s press conference, we start with China where the PBoC just now left its benchmark rates unchanged, with the one-year and five-year loan prime rates at 3.45% and 4.2% respectively. The Central Bank touted the strength of the national economy and said it has ample policy room as analysts bet on future rate cuts. Still in Asia, the Japanese trade balance fell 66.7% in August, coming in at 930.5 billion yen compared with the 2.79 trillion yen deficit a year ago: a smaller-than-expected but still 17.8% drop in imports contributed to this improvement. Yesterday saw the USD suffer badly up to the US open, with the USDIndex at -0.4% at one point and particularly weak against currencies such as the CAD, before recovering most of its losses and closing flat: the EURUSD was back below 1.07 as was the Cable below 1.24. US yields returned to new highs across the curve, on the 2, 5 and 10 year, the latter two being the highest levels since 2007. Stocks and indices closed in the red, led by the US30.

Another extremely interesting movement was that of oil, which saw Brent crude come within a hair’s breadth of $96 and Crude above $92, at very strong resistance levels tested several times last year, before falling back profusely: at the moment, the US blend is trading at $90.35.

FED’s current Dot Plot, representing Members’ rates forecasts

Tonight is the Fed meeting and there is a 99% probability that the official rate will remain in the 5.25%-5.50% range. But September is also the meeting where the Summary of Economic Projections (SEP) will be renewed and the new Dot Plot will be released: these will be key points to understand what will happen next. On the other hand, it is possible that Powell will do everything he can during the conference to reiterate to the markets that they should not think they know what he and the other board members will do in the coming months.

*FX – USDIndex flat at 104.82; EURUSD +0.05% @ 1.0685, GBPUSD -0.30% @ 1.2355, USDCAD +0.06% @ 1.3456, USDJPY flat @ 147.88, USDCNH 7.308.

*Stocks – US Futures are lower to flat (US500 -0.04%, US100 -0.10%, US30 +0.01%); GER40 is +0.10%, FRA40 -0.09%. EV maker TIO tumbled -12%.

*Commodities – USOil -1.11% @ $90.44, UKOil is trading at $93.44 after getting close to hitting $96 last night.

*GOLD – flat @ $1931.

Today: Highlights include UK CPI, PPI, Retail PI (JUST OUT, much better than expected), German PPI, US Mortgage applications, EIA Weekly Oil Stocks Change, FED INTEREST RATE DECISION, FOMC ECONOMIC PROJECTION & PRESS CONFERENCE.

Interesting Mover: USOil -1.11% @ $90.44, perfectly pulled back after reaching a key resistance level at the $92.20 area, drew a spinning top and is dumping overbought levels on the RSI.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 21 – Stocks fade, USD up as CBs spring on.

It was Fed Day and it did not disappoint. As universally expected, the result of the FOMC was a “hawkish hold.”

But we and the markets got a little more than bargained for as Chair Powell and the FOMC revealed an even more restrictive policy stance than anticipated, and clearly signaled a higher for longer stance. The markets got the message loud and clear. Stocks and bond markets are under pressure, after the Fed decision hit risk appetite. The FOMC kept rates on hold yesterday, but signalled that another hike is in the cards later in the year.

Switzerland’s SNB surprised by keeping rates on hold. Expectations had been for another 25 bp hike, but after the recent drop in inflation, the SNB decided to keep policy settings unchanged. The statement stressed that “the significant tightening of monetary policy over recent quarters is countering remaining inflation pressure”, although it left the door open to another hike by saying that “it cannot be ruled out that further tightening of monetary policy may become necessary”. The central bank’s new forecasts put inflation at 2.2% in 2023 and 2024, before a drop to 1.9% in 2025.

*FX – USDIndex has lifted to 105.35 on the Fed outlook and also support from haven demand. It holds above the 105 mark for a fifth straight session. EURUSD extended to 1.0616 lows, while GBPUSD broke 1.2300, breaching its 6-month support level, ahead of BOE rate decision. The Yen struggled and USDJPY lifted to 148.45. It has currently pulled back down to 148.15.

*Stocks – JPN225 and ASX lost -1.4% overnight, after a lower close on Wall Street and European as well as US futures are also in the red. The US100 closed -1.53% in the red, with the US500 down -0.94% while the US30 was off -0.22%.

*Commodities – USOil under $89 per barrel, as the changed rate outlook weighed on demand expectations.

*Gold has continued to trade lower at day’s low $1924.10 as markets wait for the BOE announcement.

Today: BOE Interest Rate Decision and Press Conference, US Initial Jobless Claims, Existing Home Sales, ECB President Lagarde speech.

Interesting Mover: CHFJPY has lost -1.03% so far today after the SNB announcement.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Wall Street closed with broad losses, but sentiment stabilised somewhat overnight, with China bourses outperforming. Japanese markets didn’t benefit from the BoJ’s ongoing commitment to its ultra-accommodative policy settings and the Yen sold off as the BoJ kept monetary policy parameters unchanged. European futures are in the red, US futures slightly higher, as markets continue to digest this week’s policy announcements. The 10-year Treasury yield is down -0.4 bp, the 10-year JGB rate has corrected -0.2 bp, while yields nudged higher across Australia and New Zealand.

BoJ kept monetary settings unchanged – as expected. Japan’s central bank offered no clear sign of a shift in its policy stance. The negative interest rate and the settings of the yield curve control program were left unchanged. The BoJ also maintained the pledge to add further stimulus if needed. The Yen weakened on the policy statement and yen bears will continue to test the officials’ resolve to stabilise the currency.

*FX – USDIndex has remained supported above 105 but off 105.48 highs. EURUSD and GBPUSD steady above 1.0640 and 1.2265 respectively. The Yen sold off and USDJPY lifted again to 148.40. Sterling weakened against the USD to a session low of 1.2250 after data showed retail sales in Britain rose less than expected in August.

*Stocks – US100 slumped -1.82%, with the US500 down -1.64%, and the US30 off -1.08%. Hang Seng and CSI 300 rallied 1.4% and 1.6% respectively. JPN225 ended the day down 0.52% at 32,402.41.

*Commodities – Oil prices have started to stabilise, after being knocked back by the hawkish Fed. USOil is trading at $90.28 per barrel now, Brent at $93.75 per barrel.

*Gold rebounded to $1924.80.

Today: PMIs from Germany, Eurozone, UK and US. Canadian Retail Sales also on tap.

Interesting Mover: NZDJPY has rallied by 0.65% post BoJ announcement and Ueda’s comments.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!