Market News – Cautiousness ahead of Fed, NFP & Earnings.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

* Trading remains quiet in a very busy week of data, earnings, supply, NFP and the Fed.

* Treasury yields and Wall Street posted small gains on the day but overall reain steady. It looks like fatigue has set in for the bears after knocking bonds and stocks sharply lower on the month.

* European equity futures are also steady, while the USD rose slightly against the G7 amid speculation the Fed may take a more hawkish tone when announcing its policy decision on Wednesday.

* German retail sales bounced 1.8% m/m in March. Sales were still down -2.7% y/y, but the rebound at the end of the first quarter is encouraging and suggests that higher wages and lower inflation are boosting consumption trends.

* German import price inflation was higher than expected. With the Euro lower against the Dollar, import price inflation is set to continue to nudge higher.

* French GDP expanded 0.2% q/q in the Q1 of the year.

* Japan’s unemployment unexpectedly was at 2.6% in March 2024, the same pace as in the prior month.

Financial Markets Performance:

* The USDIndex recovered slightly but holds below 105.90.

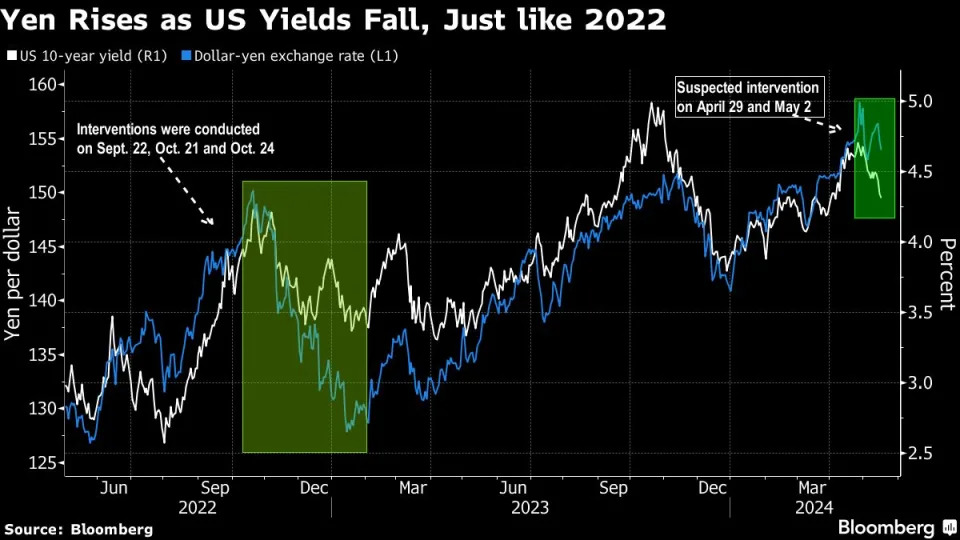

* After the assumed MoF intervention to support the Yen USDJPY was knocked down to an intraday low of 154.54 from a new 34-year high of 160.17.

* Soft Commodities: Top losers are Cocoa (-11.15%) and Wheat (-9.84%). Gains are led by Sugar (3.74%), Cotton (1.57%) and Rapeseed (1.25%).

* Metals: Top gainers are Platinum (3.70%) and Copper (2.12%). Biggest losers are Steel Rebar (-0.81%) and Silver (-0.50%). In addition, there was a slight change on Gold (-0.14%).

* Energies: Top commodity gainers are Natural gas (6.78%). Biggest losers are Natural Gas UK GBP (-4.89%), Natural Gas EU Dutch TTF (-3.85%) and Crude Oil WTI (-1.22%). In addition, there was a slight change on Brent Crude Oil (-1.09%).

Market Trends:

* Stocks were modestly higher with gains of 0.39% on the Dow, with the S&P500 and NASDAQ advancing 0.32% and 0.35%, respectively.

* Tesla rallied as much as 15% after receiving the green light for full self-driving technology in China, while Trump Media jumped 12% to boost gains on Wall Street.

* Earnings releases this week from the biggest US players include Amazon, McDonald’s, Apple and Coca-Cola. Meanwhile, Paramount is expected to post its earnings after today’s close.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Редактировалось: 1 раз (Последний: 30 апреля 2024 в 11:52)

Understanding the Implications of the FOMC Meeting.

Trading Leveraged Products is risky

The FOMC will issue its post-meeting statement at 18:00 GMT tonight. “High-for-longer” is the expected outcome (but not higher) given more indications that progress on bringing inflation sustainably down to the 2% target has stalled out. With no new quarterly forecasts, it will be all about Chair Powell’s press conference when the Fed announces its policy stance tonight.

The major question at this point will be how hawkish will he be?

It is unlikely to be any more hawkish than what the markets are pricing in. Indeed, Chair Powell will have to acknowledge that the data are going the wrong way and he may even pre-empt the likely first question out of the box, “is a rate hike in the cards?”

Meanwhile, Fed funds futures have not only fully priced out chances for a rate cut for this meeting and for June, but July as well. Risk for a reduction in September fell to below 50-50 on the initial spike in implied rates on the ECI news. The November contract reflects 20 bps in cuts, with a full quarter point easing now not seen until December. The FOMC is also expected to announce a slowing in Treasury runoff for June.

Economic Projections & Market Interpretation:

The March update of the SEP revealed notable adjustments in key economic indicators. GDP forecasts for 2024 experienced a substantial upward revision, reflecting a more optimistic outlook with a growth rate of 2.1%, up from 1.4% in December. Similarly, projections for 2025 saw improvements, with the median jobless rate forecasts showing mixed trends but generally aligning with recent patterns. Expectations for headline and core PCE chain price indices also witnessed slight adjustments, indicating potential shifts in inflation dynamics.

During the March meeting, the “dot plot” estimates hinted at a dovish stance by Fed members, with no indications of further rate hikes and median estimates suggesting potential rate cuts in 2024. This interpretation led markets to anticipate the initiation of quarterly rate cuts starting in June. As investors await the June SEP update, there is speculation about further adjustments in GDP estimates, PCE chain price indices, and the potential revision of rate cut expectations.

Analyzing the labor market reveals a complex picture of recovery and ongoing challenges. Payrolls have shown resilience in 2024, surpassing the previous year’s averages, albeit with variations across sectors. Despite improvements, the jobless rate remains a focal point, with fluctuations reflecting broader economic conditions. Additionally, metrics like the U-6 rate and wage growth provide insights into the labor market’s health and potential inflationary pressures.

Inflation Trends and Consumption Patterns:

Inflation dynamics have been closely monitored, particularly amid recent fluctuations in commodity prices and supply chain disruptions. While recent CPI and PCE chain price measures suggest some moderation in inflationary pressures, concerns linger about the sustainability of these trends. The Fed’s attention to inflation remains paramount, shaping expectations for future policy actions.

Consumer spending, a key driver of economic growth, has exhibited resilience despite ongoing uncertainties. Real personal consumption expenditures (PCE) have maintained positive growth rates, contributing to overall GDP expansion. However, shifts in consumption patterns and potential impacts on future economic performance warrant careful observation.

Market Expectations and Implications:

As the FOMC meeting approaches, market participants are closely monitoring economic indicators and policy developments for insights into future market dynamics. The verbiage of the Fed statement and subsequent press briefing will be scrutinized for any hints regarding the timing of potential policy adjustments. Investors should remain vigilant and adaptable, considering the evolving economic landscape and its implications for investment strategies.

The upcoming FOMC meeting holds significant implications for investors and economic stakeholders. Understanding recent economic developments, market expectations, and potential policy shifts is essential for navigating the dynamic financial environment. By staying informed and proactive, investors can position themselves to capitalize on emerging opportunities while managing risks effectively.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stocks mixed; Yen support still on; Eyes on NFP & Apple tonight.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

*As the Fed maintained a “high-for-longer” stance, stocks gave up their gains with attention turning back to earnings.

*Chair Powell and the Fed were not as hawkish as feared and the markets reacted immediately and in textbook fashion to the still dovish policy stance.

*The Fed flagged that recent disappointing inflation readings could make rate cuts a while in coming, but Fed chief Jerome Powell characterized the risk of more hikes as “unlikely,” giving some solace to markets.

*Stocks traded mixed across Asia, while in Europe, DAX and FTSE futures are finding buyers and US futures are also in demand, after the Fed’s message.

*Yen: Another suspected intervention by authorities, this time in late New York trading, ran into resistance from traders keen to keep selling the currency.

*Swiss CPI lifted to 1.4% y/y in April from 1.0% y/y in the previous month. Headline numbers are still at low levels and base effects play a role, with the different timing of Easter this year also likely to distort the picture. That said, the numbers may not question the SNB’s decision to cut rates, but they do not support another rate cut in June.

Financial Markets Performance:

*The USDIndex has corrected to 105.58, but USDJPY is already inching higher again, after a sharp drop to a low of 153.04 on Tuesday that sparked fresh intervention speculation. The pair is currently trading at 155.38.

*Treasury yields plunged and were down over double digits before profit taking set in.

USOIL finished with a -3.6% loss to $79.00, the lowest since March 12. Currently it is as $79.53.

*Gold was up 1.4% to $2319.55 per ounce, reclaiming the $2300 level.

Market Trends:

*Wall Street climbed initially with gains of 1.4% on the NASDAQ, 1.2% on the Dow, and 0.96% on the S&P500. The NASDAQ and S&P500 closed with losses of -0.3%, while the Dow was 0.23% firmer.

*The Hang Seng rallied more than 2%, and the ASX also posting slight gains, while CSI 300 and Nikkei declined.

*Apple’s earnings report is due after the US market closes today, will give investors a better sense of how the iPhone maker is weathering a sales slump, due in part to a sluggish China market.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Dow Jones Close To 1-Month High, Eyes on Disney Earnings.

Trading Leveraged Products is risky

*The stock market trades at a 3-week high after significant support from the latest earning reports and US employment data.

*Economists continue to expect a rate cut no earlier than September 2024 despite the US unemployment rate rising to 3.9%.

*The US Dollar Index trades higher on Tuesday and fully corrects the decline from NFP Friday.

*Dow Jones investors wait for Disney to release their latest quarterly earnings data. The stock holds a weight of 1.93%.

USDJPY – The US Dollar Regains Lost Ground

The USDJPY is an interesting pair on Tuesday as the US Dollar is the best performing currency within the market while the Yen is witnessing the strongest decline. Investors will continue to monitor as we enter the European Cash Open to ensure no significant changes. The exchange rate has been declining since the 29th of April when the Japanese Government is believed to have intervened and strengthened the Yen. However, the US Dollar has been gaining over the past 24 hours. During this morning’s Asian Session, the exchange rate trades 0.44% higher.

Currently the only concern for the US Dollar is the latest employment data which illustrates a potential slowing employment sector. However, investors are quick to point out that this cannot be known simply from 1 weak month. This is the first time the NFP data read lower since November 2023. No major data is in the calendar for the next two days which can influence the US Dollar. Despite the weaker employment data and lower wage growth, investors continue to predict a rate cut no earlier than September 2024. This is something which can also be seen on the CME FedWatch Tool, which shows a 34.3% chance of rates remaining unchanged in September.

In regard to the Japanese Yen, most analysts expect the next rate increase in the second half of this year depending on a stable movement of inflation. In addition, investors are monitoring the actions of financial authorities, expecting new currency interventions from them against a weakening Yen. This is the main concern for investors speculating against the Yen. However, economists continue to advise the Yen will struggle to gain even with a small rate hike, unless the rest of the financial world starts cutting rates.

USA30 – Investors Turn To Disney Earnings Data!

The Dow Jones is close to trading at a 1-month high and is also trading slightly higher this morning. The index recently has been supported by the latest employment data which indicates a higher possibility of rate cuts by the Fed. Today investors focus on the quarterly earnings report for Disney.

Disney stocks are trading 0.37% higher during this morning’s pre-trading hours indicating investors believe the report will be positive. So far this year the stock is trading 28.40% higher and is one of the better performing stocks. Yesterday, the stock rose by 2.47% but remains significantly lower than its all-time high of $197. Currently analysts believe the earnings data will either be similar to the previous quarter or slightly lower. If earnings and revenue read higher, the stock is likely to continue rising. The stock is the 22nd most influential stock for the Dow Jones and will only influence the USA30 and USA500, not the USA100.

Currently, technical analysis continues to indicate a strong price sentiment. The price trades above the 75-bar EMA and above the VWAP. In addition to this, the RSI is trading at 68.11 which also signals buyers are controlling the market. The only concern for traders is retracements. A weaker retracement could decline to $38,703, whereas a stronger retracement can fall back to $38,571.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stocks mixed; Yen support still on; Eyes on NFP & Apple tonight

Trading Leveraged Products is Risky

Economic Indicators & Central Banks:

* As the Fed maintained a “high-for-longer” stance, stocks gave up their gains with attention turning back to earnings.

* Chair Powell and the Fed were not as hawkish as feared and the markets reacted immediately and in textbook fashion to the still dovish policy stance.

* The Fed flagged that recent disappointing inflation readings could make rate cuts a while in coming, but Fed chief Jerome Powell characterized the risk of more hikes as “unlikely,” giving some solace to markets.

* Stocks traded mixed across Asia, while in Europe, DAX and FTSE futures are finding buyers and US futures are also in demand, after the Fed’s message.

* Yen: Another suspected intervention by authorities, this time in late New York trading, ran into resistance from traders keen to keep selling the currency.

* Swiss CPI lifted to 1.4% y/y in April from 1.0% y/y in the previous month. Headline numbers are still at low levels and base effects play a role, with the different timing of Easter this year also likely to distort the picture. That said, the numbers may not question the SNB’s decision to cut rates, but they do not support another rate cut in June.

Financial Markets Performance:

* The USDIndex has corrected to 105.58, but USDJPY is already inching higher again, after a sharp drop to a low of 153.04 on Tuesday that sparked fresh intervention speculation. The pair is currently trading at 155.38.

* Treasury yields plunged and were down over double digits before profit taking set in.

* USOIL finished with a -3.6% loss to $79.00, the lowest since March 12. Currently it is as $79.53.

* Gold was up 1.4% to $2319.55 per ounce, reclaiming the $2300 level.

Market Trends:

* Wall Street climbed initially with gains of 1.4% on the NASDAQ, 1.2% on the Dow, and 0.96% on the S&P500. The NASDAQ and S&P500 closed with losses of -0.3%, while the Dow was 0.23% firmer.

* The Hang Seng rallied more than 2%, and the ASX also posting slight gains, while CSI 300 and Nikkei declined.

* Apple’s earnings report is due after the US market closes today, will give investors a better sense of how the iPhone maker is weathering a sales slump, due in part to a sluggish China market.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Insights: The BOE’s Potential Dovish Pivot and Current Indications.

Trading Leveraged Products is risky

*The Bank of England is in focus as the regulator will confirm their rate decision and how their future monetary policy path may look.

*The GBP trades sideways but the FTSE100 continues to trade higher. Economists are contemplating if the market is pricing a dovish tilt by the BOE.

*The Dow Jones was Wednesday’s best performing index, rising 0.48%. The DJIA’s best performing stock was Amgen which rose 2.33%.

*Federal Reserve members continue to apply further pressure on the market’s sentiment with more indications that inflation is too high.

GBPUSD – Investors Focusing on A Potential Upcoming Dovish Pivot!

The GBPUSD trades sideways and did not form a significant trend the day before. This morning the price trades slightly in favour of the US Dollar, however most institutions are waiting for confirmation from the Bank of England on monetary policy adjustment. The price movement will depend on the future guidance of the Governor and the Monetary Policy Committee’s votes.

The market is expecting the interest rate to remain at 5.25%. However, there’s anticipation that regulators may hint at upcoming monetary policy easing, potentially impacting the Pound. Analysts anticipate a shift to a “dovish” policy this year but differ on timing. Most foresee changes in June or August, possibly with two 25-point rate cuts. The price of the GBP will depend on when the BOE will indicate a rate cut is likely. If 1 or 2 members of the MPC vote for a cut and the Governor advises they are now considering a cut, then the GBP potentially could decline based on a June rate cut.

Market participants are anticipating a dovish indication due to inflation declining for 3 consecutive months and declining to a 32-month low. In addition to this, the UK’s employment change has weakened for 2 consecutive months as has the UK GDP growth. Traders can see the market is pricing a dovish indication due to the GBP’s decline over the past 3 days as well as the bullish price movement seen on the FTSE100.

USA30 – When Will The Buy Signal Again Become Active?

The Dow Jones was the best-performing US index as investors increased their exposure due to its connection with defensive stocks. 70% of the Dow Jones’ components rose in value and the best performing stocks were Amgen, Boeing and JP Morgan which all rose more than 2.00%.

The next influential earnings report for the Dow will come from Home Depot next Tuesday morning. Investors are expecting a 23% rise in earnings compared to the previous quarter. In addition to this, analysts expect revenue to rise, and traders should note the company has beaten expectations over the past 4 reports. Home Depot stocks hold a weight within the Dow Jones of 5.78%.

The price of the index continues to trade above the 75-Bar EMA and above the “neutral” point on the RSI. These factors indicate buyers are controlling the market. However, this morning the price is retracing, therefore a buy signal will not be active unless the price rises above $39,091 which is the breakout level, or at least forms a bullish crossover (8-bar EMA & 18-bar SMA).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The BoE To Cut Rates In September. US Employment Data Falters!

Trading Leveraged Products is Risky

* The UK economy experiences its strongest growth since August 2023, with Monthly GDP increasing 0.4%, four times higher than expectations.

* The Bank of England saw 2 out of 9 members vote for an interest rate cut. The dovish members of the BoE are Dr Swati and Sir Ramsden.

* The BOE Governor, Mr Bailey, said two rate cuts are likely in 2024 as “one cut will keep us in restrictive territory”. However, he advises there is a higher chance the first cut will come in September.

* The UK’s FTSE100 declines close to 0.20% as the UK’s GDP reading indicates an interest cut is less likely to take place in June 2024.

GBPUSD – The UK Economy Moves Out of a Technical Recession!

The GBPUSD over the past 24-hours has been influenced by three factors: the monetary committee’s votes, the Governor’s guidance and the UK’s latest GDP figure. The GBPUSD first fell to a 2-week low due to the higher number of votes for an interest rate cute. However, the GBPUSD has since risen 0.77%. Therefore, how can traders view the price movement and the latest developments?

A large factor influencing the pricing is whether the regulator is likely to adjust its policy in June or September. A rate cut in September would support the GBP as it would keep rates higher for longer compared to the Eurozone and other competitors. The Monetary Policy Committee votes indicates the BoE is almost ready to cut rates. The Governor also said they wish to steadily move away from a restrictive policy. In the UK a restrictive monetary policy is 5.00% and above.

The reason for the price increase is the Governor indicating that there is a higher possibility the regulator will cut in September not June. In addition to this, the strong economic growth confirmed this morning further lowers the possibility of a cut in June. This is because there is less pressure on the BoE to support a stagnated economy. Therefore, a rate cut is now likely to take place in September 2024, which is on par with the Federal Reserve’s guidance for its own policy.

The Federal Reserve and The US Dollar

The US Dollar on Thursday evening was considerably pressured by the Weekly Unemployment Claims, which normally has a limited affect. The US Unemployment Claims rose to 231,000, higher than predictions of 212,000 and the highest since November 2023. Therefore, the US has seen lower NFP data, higher unemployment rate and now higher unemployment claims. This has investors questioning if the US employment sector may be weakening for the first time since raising interest rates. If so, the Federal Reserve may consider a cut in July. Currently, the CM Exchange’s tool shows a 30.8% chance of a cut in July, if this figure rises, the US Dollar could potentially weaken.

GBPUSD – Technical Analysis

Technical analysis indicates the price of the GBPUSD may rise to the previous resistance levels between 1.25650 and 1.25936. However, if the market continues to price a Fed rate cut in September, it is improbable the exchange rate will reach the resistance level at 1.26340. The exchange rate currently trades above most trend lines such as the 75-Bar EMA and is above the 60.00 mark on most RSI periods. The price has slightly retraced since rising after the GDP announcement. For this reason, the buy signal has turned into a neutral. However, if the price rises above 1.25362, the buy signal may materialize again.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Stock markets traded mixed; Flat USD ahead of US CPI.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

*Japanese government bond yields surged to multi years highs after the BOJ’s unexpected move to decrease the quantity of bonds it typically purchases during routine operations, signaling a more hawkish stance to the markets.

*BOJ Kato stated that it’s natural that monetary policy will revert to positive interest rates, while BOJ Governor Ueda signalled the potential for multiple rate hikes ahead.

*Chinese authorities have kicked off plans to sell $140bn of long-dated bonds on Friday, in order to support investment in key areas and reinforce economic momentum in the second quarter amid the country’s lengthy property crisis.

*US government plans to raise tariffs to a raft of Chinese exports were weighing on sentiment.

*BlackRock stated: The Yen’s weakness is turning foreign investors away from Japanese stocks.

Financial Markets Performance:

*The USDIndex is steady at 105 lows, at 105.58 ahead of US CPI on Wednesday, while USDJPY is holding at 155.80, after retesting May’s high at 155.96.

*EURUSD steady above 1.0750 as the euro zone prepares for an inflation reading of its own on Friday.

*USOIL declined amid demand concerns and as traders looked ahead to an OPEC+ meeting on supply policy. On the supply front, the Iraqi Oil Minister initially claimed that production cuts were adequate and opposed further reductions but later deferred decisions to OPEC. Next OPEC+ meeting: June 1. Currently USOIL is at $77.78.

*Gold corrected to $2349 per ounce, from $2380 highs.

Market Trends:

*Asian stocks fluctuate between gains and losses, as sentiment was impacted by disappointing Chinese economic data alongside optimism amid reports indicating that the country plans to initiate the sale of ultra-long bonds.

*European markets are also narrowly mixed in opening trade, while US futures are slightly higher.

*The NASDAQ is outperforming. Bonds are finding buyers and the 10-year Treasury yield is down -1.0 bp, while Bund and Gilt yields have corrected -1.3 bp and -2.3 bp in early trade.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*Asian stocks and European futures kept to small ranges as focus turned to upcoming US inflation reports.

*JGB yields surged to their highest levels in over a decade amid growing speculation that the BOJ might raise interest rates soon.

*Former central bank executive Momma stated that the BOJ might opt to deduct its planned bond purchases next month in an effort to revive a bond market that has been largely impaired by its ongoing substantial purchases.

*BOJ Governor Kazuo Ueda emphasized the importance of the market determining long-term yields independently rather than relying solely on the central bank’s actions.

*UK wage growth remained solid amid a slowdown in the job market, providing further arguments for the BOE’s monetary policy hawks to await more concrete signs of easing inflationary pressures before considering interest rate cuts.

*Eyes today are on producer price data in the US, followed by consumer price data the next day, which will provide insights into whether the Fed will consider interest rate cuts later in the year or postpone them until 2025.

Financial Markets Performance:

*The USDIndex is steady at 105 lows.

*The Yen extended losses for an 8th day against the Greenback to a 2-week low. Currently USDJPY is at 156.45.

*EURUSD rebounded slightly to 1.0785, however overall holds within a downwards channel with key resistance at 1.0850.

*USOIL held steady ahead of the release of an OPEC market outlook, with traders eagerly awaiting signals regarding the extension of supply curbs. Despite a decline since April, oil prices have remained relatively high this year due to ongoing supply restrictions by OPEC and its allies, with expectations that these curbs will be prolonged into the second half of the year. Currently USOIL is at $77.78.

*Gold (-0.93%) declined further to $2338 per ounce. Copper rose at +2.46% and Platinum +0.54%.

Market Trends:

*The 10-year JGB yield to a 6-month high of 0.965%. The 2-year JGB yield, which closely reflects policy expectations, rose to 0.340%, its highest since June 2009. The 20-year and 30-year JGB yields also surged to their highest levels in 11 years and since July 2011, respectively.

*FTSE100 stands by record highs, the S&P500 is close to topping March’s record high. The Nasdaq rose by 0.3%, with four of the Magnificent Seven stocks rising. The Hang Seng has added 20% in a rally that is entering a fourth week.

*Alibaba and Tencent report earnings later today.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Treasuries rallied, NASDAQ at new high, DXY lower after PPI pop.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

*JGB yields slipped, as markets paused amid a recent bond sell-off, awaiting a crucial US inflation report expected to influence the Fed’s short-term interest rate decisions. Remember, that typically yields move inversely to bond prices.

*US: Stronger than expected prints on PPI did not have the textbook effects on the markets. Interestingly, Treasuries and Wall Street rallied, while the US Dollar slipped. The guts of the report were not as worrisome as the headlines suggested, and the CPI is viewed as more important.

*Global equities are set for a fresh record after a big tech-led rally in US gauges.

Financial Markets Performance:

*The USDIndex slumped to 104.7, EURUSD rose to 1.0830 and USDJPY drifted at the EU open below 156.

*Gold rose almost 1% to $2358.12 per ounce, while USOIL advanced to $78.18 after shrank US stockpiles, and as traders looked ahead to a report from the International Energy Agency that’ll shed light on market balances into the second half.

*Copper spiked to a fresh record high at $5.12 a pound after a squeeze partly due to traders playing the arbitrage between futures on Comex and the Shanghai Futures Exchange.

Market Trends:

*Big tech climbed, however, boosting the NASDAQ 0.75% to a new all-time high of 16,511. The S&P500 rose 0.48% to 5246. The Dow advanced 0.3%.

*Sony shares jumped by 12% after strong earnings, a stock split and a share buyback of ¥250bn ($1.6bn).

*Tesla gained 3.3%. Tencent Holdings surged after the company’s revenue beat estimates , while Alibaba Group Holding Ltd.’s slid on a profit plunge, highlighting the growing divergence between China’s twin Internet powerhouses.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*Stocks and bonds gave a big sigh of relief after CPI and retail sales came in below expectations, supporting beliefs the FOMC will be able to cut rates by September.

*The markets had positioned for upside surprises. Wall Street surged with all three major indexes climbing to fresh record highs.

*Technical buying in Treasuries was also supportive after key rate levels were breached, sending yields to the lows since early April.

*Fed policy outlook: there is increasing optimism for a September rate cut, according to Fed funds futures, BUT most officials say they want several months of data to be confident in their actions. Plus, while price pressures are receding, rates are still well above the 2% target, keeping policy on hold. But the market is now showing about 22 bps in cuts by the end of Q3, with some 48 bps priced in for the end of 2024.

*Stagflationary Risk for Japan: GDP contracted much sharper than anticipated, for a 3rd quarter in a row. This is mainly due to consumer spending. The GDP deflator though came in higher than expected but still down from the previous quarter. The sharper than anticipated contraction in activity will complicate the outlook for the BoJ, and dent rate hike bets.

Financial Markets Performance:

*The USDIndex slumped to 103.95, the first time below the 104 level since April 9.

*Yen benefitted significantly, with USDJPY currently at 154.35 as easing US inflation boosted bets on the Fed easing monetary policy this year, weakening USD, boosting the Yen.

*Gold benefited from a weaker Dollar and a rally in bonds and the precious metal is trading at $2389 per ounce. At the same time, the precarious geopolitical situation in the Middle East is underpinning haven demand.

*Oil prices rebounded slightly after the shinking of US stockpiles and the risk-on mood due to declined US Inflation. However USOil is still at the lowest level in 2 months, at 78.57.

Market Trends:

*The NASDAQ popped 1.4% to 16,742. The S&P500 advanced 1.17% to 5308, marking a new handle. And the Dow rose 0.88% to 39,908.

*Treasury yields tumbled sharply too on the increasingly dovish Fed outlook. Additionally, the break of key technical levels extended the gains to the lowest levels since early April before the shocking CPI data on April 10 boosted rates.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Asian and European futures followed Wall Street lower.

Trading Leveraged Products is risky

Economic Indicators & Central Banks:

*The Dow topped 40,000 for the first time ever, but was unable to close with that historic handle. Concurrently, the S&P tried for its 24th record high this year but failed too.

*The rise in Treasury yields after stronger than expected import prices, and a drumbeat from Fed officials that rates need to remain high for longer, encouraged profit taking.

*Most Asian equity markets and European futures have followed Wall Street lower, after US data dented rate cut hikes.

*Chinese data showing slowed consumption and a drop in home sales, although industrial production numbers looked relatively robust.

*Japan’s core consumer inflation slowed for a 2nd month in a row in April from a year earlier, while the core consumer prices index (CPI) is expected to decelerate to 2.2% from 2.6% in March, the lowest level in 3 months, but still at or above the central bank’s 2% target for more than two years.

Financial Markets Performance:

*The USDIndex firmed slightly to 104.518 and up from the day’s nadir of 104.080. But it held a 104 handle for a second straight day. It traded above the 105 level from April 10 until May 15.

*Silver has surged nearly 25% this year, outpacing Gold and becoming a top-performing commodity, though it remains relatively inexpensive compared to gold. Both metals have hit record highs due to central-bank buying and increased interest in China.

*USOil is 0.75% higher at $79.23.

Market Trends:

*All three major US indexes closed slightly in the red after posting all-time highs on Wednesday.

*The NASDAQ closed with a -0.26% decline, while the S&P500 lost -0.21%, and the Dow was off -0.1% at 39,869. It was a corrective day for Treasuries too. Bonds unwound part of their recent rally that took rates down to the lows since early April.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Gold Reaches a New All-Time High: What’s Driving the Surge in Prices?

Trading Leveraged Products is risky

*Gold renews its all-time highs after surging 1.64% on Friday and a further 1.24% during this morning’s Asian session.

*The price of Gold has risen due to 3 factors; Iran’s helicopter crash killing at least 2 politicians, a potential rate cut and a weaker US Dollar.

*Commodities all continue to increase with Copper leading after rising a further 3.45% intraday.

*Investors are refocusing on the NASDAQ in anticipation of NVIDIA’s quarterly earnings report, which will be made public mid-week.

XAUUSD – Weaker Dollar and Chinese Demand!

Gold’s price has been increasing for the past 2 weeks but saw significant gains mainly on Friday and early this morning. Another factor investors should note is that the demand is not solely coming from the US trading session but rather all 3 trading sessions (Asian, European & US). Why is Gold again renewing its highs?

The first factor that investors need to take note of is that the price of all commodities have been rising over the past 2-weeks. Here we can see that commodities in general are seeing demand and lower supply, not solely Gold. The second factor is that China is still noticeably increasing their reserve in Gold as the country looks to enhance its currency. Additionally, the country is looking to de-Dollarize ahead of the US elections. China has considerably increased their orders for the commodity and investors should note that the Renminbi has become the fifth most traded currency in the world.

According to economists, the higher price has a lot to do with the increase in orders from certain countries. In addition to this, some investors continue to predict a rate adjustment from the Federal Reserve after a slight decline in inflation from 3.5% to 3.4%. However, traders should be cautious that the Fed’s representatives are not changing their rhetoric. Loretta Mester said that achieving their target of 2% will take longer than expected, but maintaining current interest rates will help reduce price pressure. The official added that the US Fed needed more evidence of an inflation reduction to begin easing monetary policy. Below are the dates some of the main global banks expect the Federal Reserve to start easing:

July 2024 – JP Morgan & Goldman Sachs

September 2024 – Morgan Stanley & UBS Group

December 2024 – Bank of America and Deutsche Bank AG.

Technical analysis continues to point towards an upward price movement including the VWAP, Moving Averages and Bollinger Bands, though the price is understandably overbought on most oscillators including the RSI. However, based on the previous two impulse waves on the daily chart, the price potentially can increase a further 2-3% before losing momentum if it is going to follow previous patterns.

USA100 – Investors Focus On NVIDIA Earnings Report

The USA100 was the worst performing index on Thursday and Friday. However, the index will again be under the spotlight as NVIDIA’s Quarterly Earnings Report will be released Wednesday evening. Economists have said one of the main reasons behind the loss of momentum towards the end of the week was the “higher weight” stocks underperforming. Of the “magnificent seven” stocks, only three have outperformed the NASDAQ over the past month. These include NVIDIA, Alphabet and Amazon.

On the positive side, the price this morning is increasing as are other global indices, indicating a “risk-on” appetite. Furthermore, an influential factor will be NVIDIA’s earnings and revenue data. Analysts expect the company’s Earnings Per Share to rise 7% and revenue to increase to $24.55 billion, a new record high. If the report is higher than expectations, the price of the stock is likely to rise and support the NASDAQ accordingly.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

NASDAQ Soars with AI and Semiconductor Stocks Leading the Charge, While AUD Struggles.

Trading Leveraged Products is risky

*The NASDAQ witnesses a large surge in buy orders at the opening of the US trading session, adding 0.80%. The index has added 13.74% in 2024 up to now.

*AI & Semiconductor stocks are mainly behind the upward surge in the market ahead of NVIDIA’s earnings report tomorrow evening.

*The Australian Dollar is again the worst performing currency for a second day with the AUD Index trading 0.22% lower.

*The RBA’s Meeting Minutes confirm the committee deem a “pause” the strongest case, but that a hike may be necessary if data is “overoptimistic”.

USA100 – AI Stocks and The Semi-Conductor Sector Ensure Momentum Continues!

The NASDAQ saw a decline in the price before the US market opened, but quickly changed thereafter. At the opening of the US session, the NASDAQ rose for 3 straight hours adding 0.80% before losing momentum. Due to the bullish momentum, the index again rose to renew its all-time highs.

The best performing stocks with yesterday’s markets were largely AI driven companies as well as companies within the semiconductor sector. Some of the best performing stocks within these sectors were Applied Materials (+3.71%), Lam Research Corp (+3.29%) and Micron Technology (+2.96%). However, investors are of course mainly focusing on NVIDIA which is also likely to determine the investor sentiment towards the index in general. NVIDIA stocks rose 2.49% during yesterday’s session and is trading 0.27% higher during today’s pre-trading hours.

No major events are in the books for the day which may influence NASDAQ. However, investors will monitor the FOMC Member’s speech, Mr Christopher Weller, who is also likely to add to the rhetoric from the past week. However, investors have largely ignored comments from the Fed regarding less rate cuts than previously thought. Therefore, the speech is likely to have minimal effect unless extremely hawkish.

Technical analysis does continue to point towards an upward price movement in the medium – longer term. The price waves continue to form higher lows and higher highs. Simultaneously, the price of the index is trading above the Moving Averages and above 50.00 on the RSI. However, technical analysts advise the upward price movement may be lesser than yesterday’s due to the upcoming earnings data.

The US 10-year bond yields rose 0.05% during this morning’s Asian session. ideally investors would like to see yields remain no higher than their current point to support a further upward trend. During yesterday’s session 73% of stocks holding a weight of more than half a percent rose. For further upward price movement, investors would ideally like to again see more than 70% of the components rise further.

AUDUSD – A Break Of The Support Level Could Strengthen Sell Signals!

This morning the AUDUSD exchange rate fell 0.33% to retrace upwards when reaching the previous support level. The Australian Dollar Index is the worst performing currency trading 0.22% lower. However, the exchange rate is struggling to gain momentum below the 0.66471 support level. If the price declines below this level, sell signals are likely to strengthen.

For the exchange rate to gain momentum, the US Dollar Index will also need to support price action. The most recent support for the currency is the hawkish comments from members of the Federal Reserve Open Committee. Mrs. Loretta advises 3 rate cuts are no longer appropriate and more or less not possible, and also advises the market is no longer worried that the policy is too restrictive. Mr Bostic also added to the hawkish rhetoric.

The Reserve Bank of Australia’s Meeting Minutes confirm that the committee favor a pause and remain largely predictable. However, the Meeting Minutes also state the regulator would consider a hike if data became more optimistic. Nonetheless, this has not yet had a positive effect.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

UK Inflation Drop Boosts GBP, But Analysts See Correction Signals.

Trading Leveraged Products is risky

*The NASDAQ forms its 5th bullish wave resulting in the index trading 8% higher this month alone. Investors are waiting for NVIDIA’s earnings report.

*The market awaits the release of the latest FOMC Meeting Minutes for further indications on the potential rate adjustments.

*The US Dollar Index declines to a 7-week low, but can tonight’s Meeting Minutes change the trend? Read below what economists are predicting.

*UK inflation declines from 3.2% to 2.3% in its largest drop since December 2023. The Pound increases as the inflation rate did not decline to 2.1% as previously

GBPUSD – UK Inflation Drops But Does Not Meet Previous Expectations!

The GBPUSD is trading 0.30% higher after the release of April’s UK inflation figures. The US Dollar and the Japanese Yen are the worst performing currencies of the day. Traders looking to speculate a rising Pound may benefit from these weakening currencies. The GBPJPY is trading 0.47% higher so far. However, investors should be cautious of any change in price action as the next session (European Market) opens.

The UK’s inflation figure fell from 3.2% to 2.3% which is the largest drop in 2024 so far and brings the Bank of England closer to its target. This would normally pressure the currency, but there are some factors which have triggered a bullish Pound. This includes the Core Consumer Price Index which fell from 4.2% to 3.9% instead of falling to 3.6% which were the previous expectations. Also, certain sectors did not see a decline in inflation in April, which is a continued concern. For these reasons, investors have increased their exposure to the Pound, supporting the currency. Also, economists are advising that the weakening inflation rate can increase investment demand which also further supports the country’s economy and subsequently the currency.

Furthermore, investors will also need to take into consideration the price condition of the US Dollar individually. Dollar traders will be focusing on tonight’s Federal Open Market Committee’s Meeting Minutes. The market will particularly be looking for clarity on how many adjustments are likely in 2024, if any at all. In addition to this, if an adjustment is likely in July, September or later in the year. If the report indicates less cuts and a delay, the US Dollar potentially can witness further demand and a change in trend. This is something which was particularly seen in April 2024.

The price action of the GBPUSD is forming a bullish trend and most trend-based indicators are signalling a higher price. However, there are signs that the price may correct back to the previous range. For example, on the 4-Hour chart the price is witnessing a divergence signal. in addition to this, the price is also trading at a significant resistance level from November, December and January. Though, for the resistance level to become active, the Dollar will likely require support from the upcoming Meeting Minutes. In the short term, sell signals are likely to materialize after crossing 1.27400 and 1.27268.

USA100 – Bullish Trend, But Investor Focus On Meeting Minutes & NVIDIA Earnings

The NASDAQ saw a decline in the price as the US Open was approaching, however, the price momentum quickly changed when US investors started trading. The index rose 0.30% by the end of day and was the best performing US index. During the US Session 62.5% of stocks holding a weight of more than 1.00% rose while 37.5% fell. The main price drivers which supported the upward price movement were Microsoft, Alphabet, Apple, NVIDIA and Netflix.

Investors will closely be monitoring the upcoming earnings report for NVIDIA, but also the FOMC’s Meeting Minutes. A more restrictive monetary policy can pressure the stock market, but the level of pressure and downward price movement will also depend on the results of NVIDIA’s earnings. Additionally, shareholders will also focus on Intuit’s Quarterly Earnings Report tomorrow evening, but this will have a lesser effect compared to NVIDIA.

A concern for intraday traders is the decline in indices around the world in markets which are currently open. For example, the DAX, FTSE100, CAC and Nikkei225 are all trading lower. In addition to this, the US 10-Year Bond Yields are trading 0.0027% higher which is additional pressure on equities. Nonetheless, technical analysis in the medium to longer term continue to point to a continued upward trend.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

NVIDIA Surpasses Earnings Expectations, Fed Considers Another Rate Hike.

Trading Leveraged Products is risky

*FOMC Meeting Minutes confirms certain members believe the current monetary policy may not be “adequately restrictive”.

*The US stock market depreciated after the Meeting Minutes. However, investors quickly bought shares after NVIDIA’s Quarterly Earnings Report. The US Stock Market on average rose 0.50% after the Meeting Minutes.

*NVIDIA’s Earnings Per Share rose from $5.16 to $6.12 and Revenue rose 15% in the first quarter of 2024.

*Yesterday the US Dollar Index rose up to 0.32% and shot upwards 0.15% in the 30-minutes after the Fed release.

USA100 – NVIDIA’s Earnings Increase Sentiment And The NASDAQ To An All-Time High!

On Wednesday, the NASDAQ spent most of the day witnessing intraday declines which gained momentum after the Fed Minutes. After the Federal Reserve Meeting Minutes, the NASDAQ was trading 0.69% lower and the SNP500 0.74% lower. The decline was a result of the ultra-hawkish comments within the Federal Open Market Committee regarding monetary policy and inflation. However, as the price fell to $18,619.54, the price thereafter surged more than 1.50% within the next 8-hours.

The change in trend is a result of the positive Quarterly Earnings Report from NVIDIA. NVIDIA’s Earnings Per Share rose from $5.16 to $6.12 and Revenue rose 15% in the first quarter of 2024. Shareholders held onto their shares while buy orders rose triggering a much higher price. In addition to this, NVIDIA’s director’s speech expressed confidence in earnings and the upcoming quarters. NVIDIA’s management also compared their success to the industrial revolution.

As a result, NVIDIA’s stock rose more than 6.00% after market close and is now trading above $1,000. In addition to this, the comments and earnings data had a positive effect on investor sentiment in the broader stock market, but particularly for semiconductors and chipmaking companies. For example, AMD’s stocks rose almost 2.00% and Applied Material Stocks rose 1.75% after NVIDIA’s earnings report.

Due to the volatility the price of the index is obtaining primarily “buy” signals from indications and technical analysis in general. The price has also become “overbought” on the RSI on some timeframes but remains within a buy signal and not overbought on intraday timeframes. Though investors should note that the Fed’s Meeting Minutes does bear risk for the index. This will be expanded on below.

EURUSD – The US Dollar Rises As Fed Members Play With The Thought Of Another Rate Hike!

The EURUSD is trading within an upward facing corrective swing measuring 0.14%. The bullish price movement is currently only forming a retracement pattern as the EURUSD exchange rate has been trading within a bearish trend for 5 days but gained momentum yesterday due to the US Meeting Minutes.

According to the Meeting Minutes, certain officials believe the policy requires a 25-basis points hike to achieve the 2% target. In addition to this, even the members which are known to be more dovish were troubled by the rise in inflation. Economists continue to believe the Federal Reserve is unlikely to increase rates despite the recent comments. There is a 49% possibility of a rate cut in September according to the CME FedWatch Tool. However, 13.00% of the market believe there will be no cuts at all in 2024.

The hawkish comments regarding higher interest rates are positive for the US Dollar and have triggered various sell signals for the EURUSD. However, investors should also note that a hawkish Fed can also significantly pressure the stock market. Currently, economists are battling amongst each other over whether the higher earnings or the hawkish Fed will be the main price driver. Currently, the higher earnings data is winning, but this may not be the case if inflation does not decline this month.

In terms of the Euro, the latest price driver is the European PMI data for Germany and France. German PMI beat expectations while French data saw a mixed reaction. Investors will now turn their attention to the US data later in this afternoon.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market News – Erosion in Fed rate cut odds; Stocks, Oil & Gold under pressure

Trading Leveraged Products is Risky

Economic Indicators & Central Banks:

Nvidia bigger than entire stock market – Market cap now greater than Australia, South Korea and Russia.

* After the massive Nvidia beat, rallying over 9% on the day, failed to reinvigorate the rally at the close. It was unable to support the major indexes.

* Wall street: The profit takers ruined the party, taking advantage of recent record highs to take some chips off the table. Erosion in Fed rate cut expectations provided extra incentive to sell.

* Strong US economic activity: Strong PMI, tight jobless claims, slump in Home sales and high home prices pushed Fed rate cut expectations further back. US jobs data released showed initial applications for unemployment were slightly lower than expected, indicating the economy was holding up despite high rates. The data, Fedspeak and the FOMC minutes, have cast doubt over whether officials will have enough evidence of the disinflation trend to begin cutting rates by September.

* It is an early close in bonds today and that could accelerate activity as traders position ahead of the long Memorial Day weekend.

Asian & European Open:

* Asian equities dropped today, following Wall Street lower.

* Chinese officials announced an Rmb300bn ($42bn) lending package to help buy back real estate from the nation’s indebted property developers.

* Japan: Inflation slowed for the 2nd straight month in April, making it difficult for BOJ to proceed with further tightening. Inflation could pick up due to weaker Yen and rising Oil.

* BOE UK consumer confidence recovered while retail sales slumped. For the BoE that means there is less risk of a wage-price spiral as companies will increasingly struggle to pass on higher labor costs. More arguments in favor of an early rate cut then, despite recent data showing that headline inflation is not coming down as fast as hoped.

Financial Markets Performance:

* The USDIndex found its footing, extending against G10 for a 5th day.

* Pound dropped after the UK Retail Sales, with GBPUSD at 1.2670.

* Oil declined after hitting its 3-month low as the market flashed signs of weakness ahead of the US summer driving season. Elsewhere, Gold remains weak at $2337, for a 3rd day.

Financial Markets Performance:

* The Dow lost -1.5% to 39,065 with Boeing down over -7%. Live Nation dove as the DoJ filed suit to divest Ticketmaster. The S&P500 slumped -0.74% to 5267. And the NASDAQ declined -0.39%.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

The New Zealand Dollar Tops All Currencies, Gold Lags Behind Silver!

Trading Leveraged Products is risky

*Silver and Gold increase in value during Monday’s Asian Session. Silver rises more than 2.00%, considerably more than Gold. Will Gold gain momentum during the US trading session?

*Citi Group advise the price of Gold can potentially rise to $3,000 in the next 12 months. The institution also advises commodity prices are likely to remain high.

*The New Zealand Dollar is the best performing currency on Monday followed by the Japanese Yen. The Yen loses momentum as the Asian Session comes to an end.

*Of the NASDAQ’s 20 most influential stocks, only 4 ended Friday’s session in the red. The index ended the session 1.10% high and 0.06% higher in today’s Asian Session.

XAUUSD – Gold Lags Behind Silver, But Where Will Buy Signals Materialize?