Market Update – July 24 – It is all about central banks!

Trading Leveraged Products is risky

It is all about central bank decisions this week with three major banks on the calendar including the FOMC, ECB, and BoJ, with the markets positioning ahead of these releases. Trading was quiet heading into the weekend while Treasuries have gone through several gyrations in recent weeks amid on-again, off-again expectations regarding the future policy path. Dollar steadied at 100.73 as bearish US Dollar bets prevail. Today, stock markets traded mixed and Japan bourses rallied, as comments and reports suggest the bank sees little need to tweak policy or address the side effects of YCC.

Sunday: Spain was plunged into political uncertainty on Sunday night as both the right and left failed to secure a clear path to forming a government, even though the opposition People’s Party won the most seats in parliament.

OIL is still headed north, USOil regained $76, UKOil is trading above $80. You have probably heard about the rally in agriculturals and it’s good to keep an eye on the commodities prices input for future inflation developments. Anyway, Wheat price is still well below where it has been for the vast majority of time since the beginning of 2022.

*FX – The USDIndex firmer at 100.73. USDJPY at Friday’s highs at 141.55 as gains against JPY were pronounced after indications from BoJ Ueda that the Bank is not looking to tweak YCC any time soon. GBP hovering around 20-DMA, at 1.2870, while EUR holds above 1.11 for now.

*Stocks – The JPN225 closed up 1.23% at 32,700.7 amid the automakers rally including Mitsubishi (+5.55%). GER40 and UK100 are down -0.4% and US futures are narrowly mixed, with the US100 outperforming slightly. Hong Kong’s Hang Seng index was a bit of an outlier on the downside with a drop of 1.5%, dragged lower by Chinese property developers which tumbled more than 5%. #Nvidia -2.66%, #META -2.73%, Chevron +1.46% (strong oil earnings) & #Tesla -1.10%.

*Commodities – USOil remains supported as supply restrictions start to bite, at $76.60.

*Gold – failed to break 20-DMA and currently settled at $1962.80.

Today – Data on Consumer Confidence, Q2 GDP and US inflation. Microsoft, GM, Verizon, Alphabet, Exxon Mobil, Meta and more stocks to watch this week.

Biggest FX Mover @ (06:30 GMT) EURUSD (-0.54%) return below 1.1100 post German manufacturing PMI.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 25 – Investors are Buying into Hopes

Trading Leveraged Products is risky

Optimism in China’s recovery has made a comeback and investors are buying into hopes that decisive stimulus action from Beijing will boost domestic demand. The Chinese equities jumped on Tuesday, after the country’s ruling politburo vowed to boost employment and revive a “tortuous” economic recovery. China’s powerful 24-member politburo said it would tackle unemployment, speed up issuance of local government special bonds and boost consumption of electronics, electric vehicles and other goods. The JPN225 struggled through and gains in Australia were much more muted. Futures in Europe and the US haven’t moved much as markets turn cautious ahead of this week’s key central bank announcements in Germany, the US and Japan. Wheat prices climbed to a 5-month high on Tuesday, as Russian assaults against Ukrainian ports that ship the grain intensified.

*FX – The USDIndex is at 101.26. USDJPY is struggling for a third day in a row to overcome 142.00. GBP closed below 20-DMA yesterday and holds below it so far at 1.2840, while EUR holds above 1.11.

*Stocks – Hong Kong jumped as much as 5% and the Hang Seng is currently up 4.0%, while the CSI 300 has rallied 2.9%.

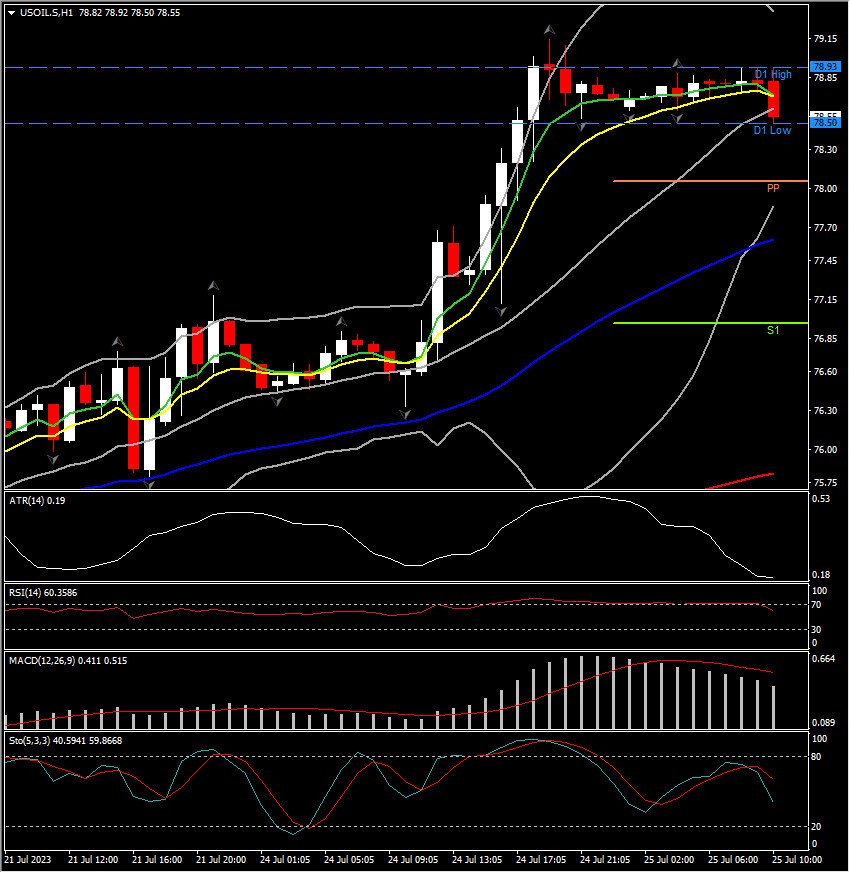

*Commodities – USOil spiked to $79 area. Oil is heading for a solid monthly gain, as output cuts start to bite and counterbalance concern that the sluggish recovery in China will cap demand. There are now more signs that Russia is making good on its pledge to rein in supplies with data showing that the country’s crude shipments fell to a 6-month low in the 4 weeks to July 16. Supply could further tighten in August, as Russian oil exports are set to be reduced further. A decline in drilling activity in the US is adding to supply concerns and the US Energy Information Administration has already revised down its short-term outlook for US production with further corrections possible unless the trend in drilling activity reverses. Also China flagged more measures to boost economic growth, aiding the outlook for energy demand just as the global market shows signs of tightening.

*Gold – holds a floor above 50-DMA at $1955.

Today – Germany’s Ifo business survey and IMF publishes an update to its World Economic Outlook. Earnings: Microsoft, Alphabet, Visa, Verizon, UBS, Nextera.

Biggest FX Mover USOIL spiked to $79.16 while today it sustains gains above 78 territory.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

China stocks rallied and hit a 6-week high, as investor confidence in official stimulus measures strengthened. Property, financial and consumer related stocks in particular benefited, after signals of further support. The BoJ signalled a widening of the band for the 10-year yield, which was taken as a sign that the BoJ is heading for policy normalisation. The Yen rallied as a result. Bunds are selling off in early trade, after much stronger than expected French GDP numbers and as markets continue to digest yesterday’s ECB announcement. French inflation dropped to 5%, the lowest level for 16 months. In US, much stronger than expected GDP, tighter than projected jobless claims, a pop in durable goods orders, a bounce in pending home sales, and a narrowing in the goods trade deficit boosted risk for a 12th rate hike for the FED. Bonds and Stocks selloff.

Overnight: BoJ tweaks yield curve control. The BoJ kept the target for 10-year yields at around 0% but signalled that the 0.5% ceiling was now a reference point, not a rigid upper limit. It will offer to buy bonds at the 1% mark, which means an effective widening of the band. Ueda vowed to keep easing, while at the same time, he pledged to continue to ease tenaciously and to add further easing if necessary. Ueda added that he expects inflation to slow before gradually picking up again.So some attempt to play down the importance of today’s surprise move and prevent markets from buying into an imminent move towards policy normalisation.

*FX – The USDIndex held most of yesterday’s gains and is at 101.72, as the 10-year Treasury yield inched higher. The Yen strengthened with USDJPY at 138 lows. GBP drifted to 1.2760 and EUR at 1.0950.

*Stocks – The CSI 300 is up 2.1%, the Hang Seng still 1.2%, and JPN225 declined. #Evergrande plunged as trading resumed nearly 16 months after the stock was suspended pending the release of financial results. #Ford stock is higher after hours after the automaker reported strong second quarter earnings and also upped its full-year profit forecast, though it did project steeper annual losses in its EV division. Ford’s results come after its crosstown rival #GM reported strong earnings and raised its full-year profit guidance for a second time. #Intel’s (+8% after hours) earnings surprised positively after two consecutive quarters of record losses. Strong sales of drugs for cancer and diabetes helped #AstraZeneca beat sales and earnings expectations.

*Commodities – USOil spiked to $80.30 on tighter supply (Fed raises interest rates by 25 bp, US crude inventories fall less than expected, ECB raises rates to 23-year high, OPEC+ panel meeting in focus)

*Gold – drifted to $1941 from $1980, amid strong US economic data which renewed the Fed’s pledge to stay hawkish.

Today – German Inflation, Canadian GDP and US PCE, Earnings: Exxon Mobil, Procter & Gamble, Chevron etc.

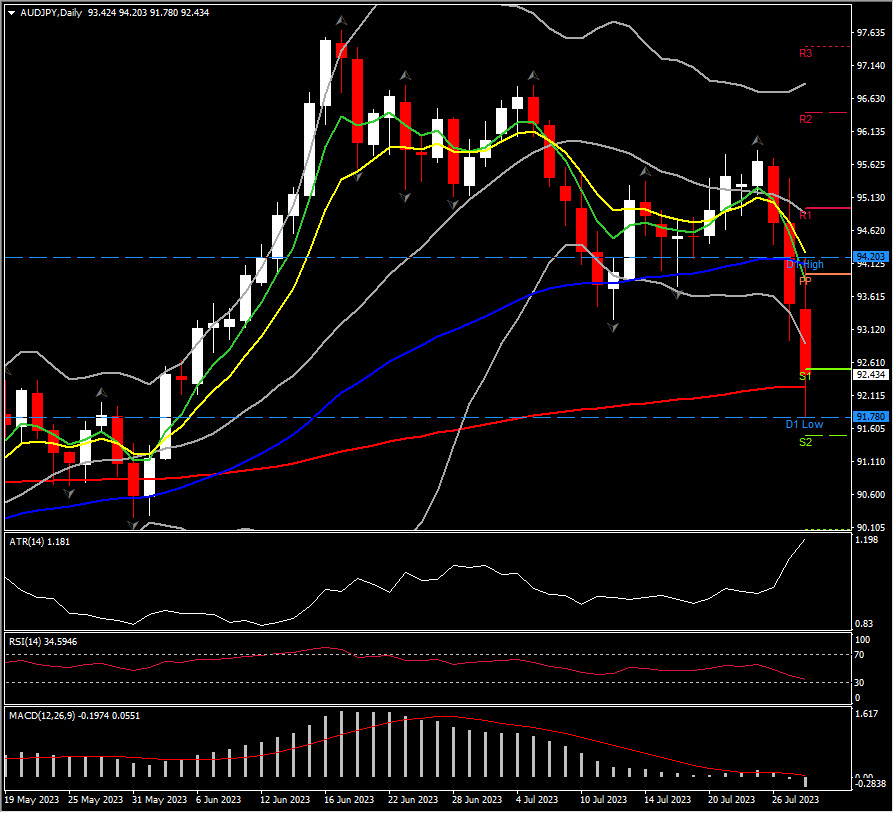

Biggest FX Mover (@6:30 GMT) AUDJPY (-1.31%) bottomed at $91.78 with RSI and MACD turning below neutral in line with 3-day sharp decline. ATR(H1) is at 0.591 and ATR(D) is at 1.181.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 31 – Another month of gains for stocks comes to an end.

Trading Leveraged Products is risky

Last Friday, the headline PCE figure for June came in at 3%, the lowest annual increase since March 2021 and just one percentage point over the Fed’s target of 2% inflation; Core set at 4.1. US indices cheered the data and are set for another strong month of gains, the fifth in a row for the US500 that is up 3% in July compared to Nasdaq which has increased 3.8%. Industrial production y/y fell in Japan as did retail sales on a monthly basis; in China, manufacturing PMI is still in contraction (49.3), while the services component is deteriorating (51.5 from 53.2). China just issued measures to recover and expand consumption as per a State Council Document just released. JPY keeps collapsing despite the ”adjustment” on the 10y policy: last Friday a mysterious buyer stepped in at 0.57%, today the BOJ officially announced unscheduled bond buying at 0.60%. This week we have the BOE and RBA (the latter tomorrow morning, expected to raise by 25 bps to 4.35% despite the latest inflation data), US NFP data and the earnings season continues with AAPL and AMZN reporting on Thursday.

Overnight: BoJ tweaks yield curve control. The BoJ kept the target for 10-year yields at around 0% but signalled that the 0.5% ceiling was now a reference point, not a rigid upper limit. It will offer to buy bonds at the 1% mark, which means an effective widening of the band. Ueda vowed to keep easing, while at the same time, he pledged to continue to ease tenaciously and to add further easing if necessary. Ueda added that he expects inflation to slow before gradually picking up again.So some attempt to play down the importance of today’s surprise move and prevent markets from buying into an imminent move towards policy normalisation.

*FX – USDIndex is up 0.2% to 101.61 boosted by a weak Yen (USDJPY -0.46% at 141.81). EURUSD sits just above 1.10, Cable hovers around 1.285, AUDUSD is bid before the RBA tomorrow (+0.51% at 0.6681).

*Stocks – US futures are slightly in red: US500 -0.13%, US30 -0.07%, US100 -0.17%. A similar picture in Europe where GER40 futures are -0.14%. GOOGL increased 10% last week and the US market is set for another month of (broad) gains.

*Commodities – USOil -0.5% now at $80.25, UKOil hit $85 and is now at $84.51.

Gold – down -0.23% to $1954.91, XAG – 0.40% at $24.24.

USDJPY, 30 mins

Today – Germany retail sales, GDP from Italy, Spain and Europe, European HICP, US Chicago Purchasing Managers’ Index.

Biggest FX Mover (@6:30 GMT) Coffee (-2.11%) trading at $158.60 heading south towards the recent $154.50 bottom area. RSI at 41.46 and downward sloped, MACD negative, 50d – 200d MAs downward sloped (and have recently crossed).

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 1 – A traditionally volatile month kicks in.

Trading Leveraged Products is risky

Overnight RBA left rates unchanged at 4.1% against expectations: recent CPI and PPI data – much weaker than expected – must have weighed on the decision even if the bank stated that ”further monetary policy tightening may be required” and considers that inflation ”is to return to the target range of 2-3% by late 2025”. Keep in mind the tight local labour market. We had more bad data from China where Caixin Manufacturing shrank to contraction territory in July (49.2) and house sales figures reported the largest dip in a year. At least HSBC reported an 89% rise in pre-tax profit and is up 1.8% in HK. 10y JGB are still finding a bottom at 0.60%, Yen is tumbling and the Japanese Minister of Finance Suzuki is back to the rhetoric of ”closely monitoring the market”. US markets were up again yesterday and US500 has not had a >1% drop in 41 days now; Russell 2000 has been the monthly best performer testifying to how the rally is no longer driven only by Tech mega-caps but its breadth is broadening. This is the busiest week of the earnings season and after more than 160 companies included in the US500 have already reported, today we await Merck, Pfizer, Caterpillar, Norwegian, AMD and many more.

US500, 5 mins, Intraday Shorts covering at the close?

*FX – USDIndex is up 0.15% to 101.77, AUDUSD fell 0.74% after RBA decision (0.6668) giving up just some of yesterday’s gains, EURUSD is just shy of 1.10, Cable down 0.1% to 1.2820. USDJPY eyes 143.

*Stocks – US and EU futures are slightly red, -0.1% on average. Dax has been trading above its previous ATH seen in June for a couple of days now. Nikkei up 0.65% on weak JPY.

Commodities – USOil extends its rally, trades at $81.52 now. Corn, Wheat fractionally up after a 5 day losing streak, Copper reacts to $400 but is surprisingly edging higher on a 2 month perspective.

*Gold – trading at $1959 this morning, XAG at $24.85.

Today – Germany, Europe unemployment, US Canada – Spain – Italy – France – Germany Manufacturing PMI, API weekly Crude Oil Stock. EARNINGS: Uber, Pfizer, Caterpillar, Norwegian BFO; AMD, Starbucks, MicroStrategy, Pinterest, ATC.

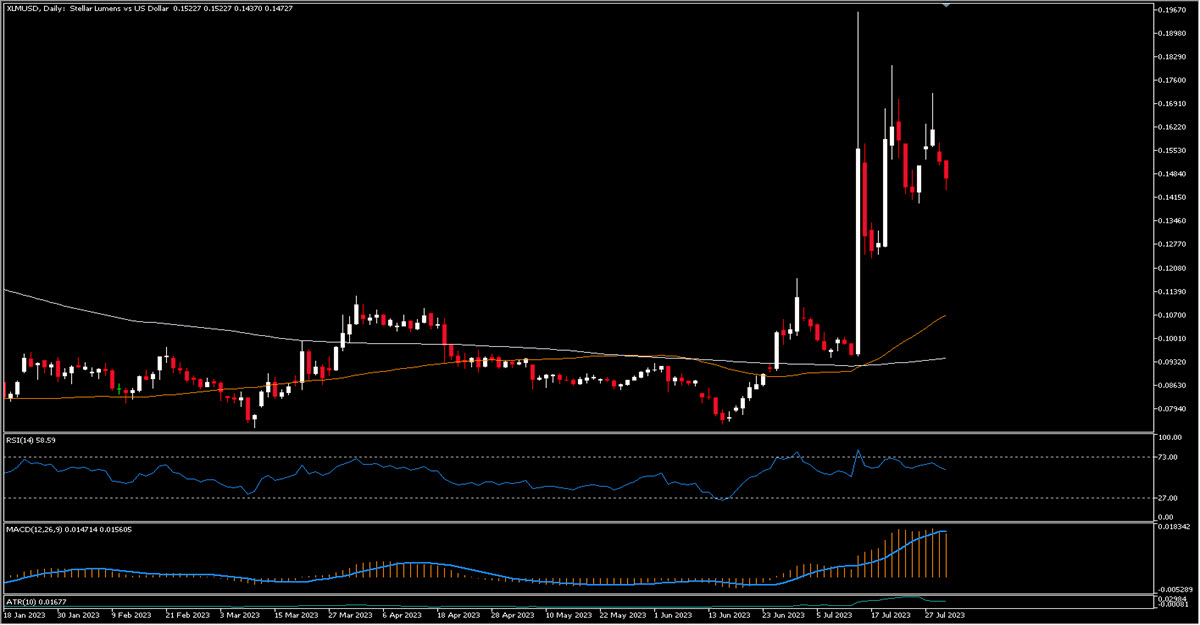

Biggest FX Mover (@6:30 GMT) XLMUSD (-3.67%) trading at $0.1468 and consolidating within a triangle after the recent rally. MACD histogram just crossed to the downside, RSI negatively sloped.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 2 – U.S. rating downgraded at Fitch.

Trading Leveraged Products is risky

US stock futures fell Tuesday night after Fitch downgraded the US’s long-term rating to AA+ from AAA Tuesday night, citing ”an erosion of governance and expected fiscal deterioration over the next three years”. The agency called out brinksmanship in Washington around debt ceiling negotiations earlier this year. This sparked some risk aversion flows with APAC indices falling led by Japan while JPY is strengthening on safe haven trading even if Bank of Japan has pushed back on speculation its recent policy adjustment marked the start of a tightening cycle. Bonds are lower around the globe with 10Y US back above 4% and 10Y JGB at 0.62%. The negativity in Asia was also fostered by the softening of the manufacturing activity across the ASEAN region that expanded at the slowest pace in 7 months. We saw some weak macro data in the US yesterday (ISM, Jolts Jobs Openings) and particularly eye-catching has been the Crude Oil inventory data which pointed to a record weekly drawdown (-15.4M) and helped Crude to climb above $82. Earnings season is more than halfway over with results coming in stronger than expected. Of the S&P 500 companies that have reported, about 82% have posted positive surprises as of last night.

US Debt to GDP ratio

*FX – JPY is the best performing major this morning, USDJPY –0.45% to 142.68, EURUSD +0.04% at 1.0989. All other currencies are down vs the USD with antipodean leading the losses, AUDUSD –0.56% at 0.6577, NZDUSD -0.74% at 0.6104. USDIndex just shy of 102.

*Stocks – Futures are negative this morning: US500 -0.49%, US100 -0.78%, GER40 -1.17%. Asia fell led by NIKKEI -2.44%, HK – 2.23%. AMD rose 2% after market after reporting better-than-expected quarterly results.

*Commodities – USOil regains $82, $82.17 now. Copper clearly lost $400 ($389 now), Agriculturals trade up with conviction.

*Gold – stuck at $1949 this morning, XAG at $24.32.

Today – US ADP National Employment. EARNINGS: PayPal, Qualcomm.

Biggest FX Mover (@6:30 GMT) JPN225 (-2.42%) trading at 32590 and just in contact with its 50d MA. RSI negatively sloped at 48.36, 5 month trendline awaits at 32k this morning.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 3 – 48 sessions later, the BOJ’s weak heart, BOE, AAPL & AMZN await.

Trading Leveraged Products is risky

48 sessions: this is how long it has been since the last time the US500 was down more than 1%, on 23 May. Fitch’s downgrade was a good excuse to sell a probably expensive market and the US100 fell 2.21%. Rates were sold, especially on the long end (the 10y) which led to a steepening of the curve again (the 2y10y is now at -77 bps): this is a classic where the movement comes not from a change in the outlook for growth, inflation etc but from a (minimal) ”increase” in country risk. Currently only Moody’s retains the AAA qualification. Admittedly, a much higher than expected ADP figure helped the selling pressure on bonds (+324k vs. +189k expected) but let’s not be under any illusions about the NFP: it has long proved to be a poor forecaster.

US500, H4

Overnight the BOJ implemented its second unscheduled bond buying intervention as the JPY sank again. Later we will also have the BOE’s decision, which is expected to make a difficult choice between a 50 bps increase or perhaps 25 bps with a focus on more quantitative tightening. Interestingly, the easing cycle started in South America and then Chile, while Brazil also cut 50 bps yesterday, more than expected. Finally, let us not forget the big names that will report tonight, Amazon and Apple: for the former the options market is pricing an implied movement of 5.9% after the results, for the latter only 1.59%.

*FX – USDJPY is up to 143.88 on a sinking Yen, further dragging down the USD Index that stays at 102.60 now. EUR and GBP are little moved while AUDUSD and NZDUSD sank to 0.6535 and 0.6073 respectively.

*Stocks – US Futures are slightly up (0.1%) this morning after yesterday’s sell off. China50 +0.78%, JPN225 -0.94%. Qulacomm slipped nearly -7% after hours after missing on fiscal 3rd quarter revenue and guidance for the current period.

*Commodities – USOil suffered some selling pressure as did the overall market yesterday (-2.95%) and is now trading at $79.59, Copper at $385.15.

*Gold – flat this morning after having retreated to $1934, XAG at $23.66.

Today – European HCOB Composite and Services PMI, EU PPI, BOE Interest Rate Decision, US Jobless Claims, US Factory orders, Services PMI. EARNINGS: Apple, Amazon, Coinbase, Airbnb after the close, Moderna BTO.

Biggest FX Mover (@6:30 GMT) Coffee (+1.64%) trading at 167.45, continues the upward move from the $154.5 support, RSI positively sloped at 55.51, MACD still negative but moving north.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Welcome to our weekly agenda, our briefing of all the key financial events globally.

The fallout from the Fitch ratings downgrade for the US and the worries over the debt situation the US is facing could continue weighing on the Stock market. Robust results from tech giants such as Amazon helped to lift sentiment. This week’s agenda is relatively quiet with Inflation out of the US and China dominating the calendar along with earnings releases.

Tuesday – 08 August 2023 -----------------------------------------------------------------------------

Trade Balance (CNY, GMT 03:00) – China’s trade surplus fell to $70.62 billion in June 2023, as exports dropped more than imports amid persistent weak demand from home and abroad.

Harmonized Index of Consumer Prices (EUR, GMT 06:00) – The German inflation for July is anticipated to remain steady at 6.5% y/y and 0.5% m/m.

Wednesday – 09 August 2023 -----------------------------------------------------------------------------

Consumer Price Index (CNY, GMT 01:30) – The Chinese inflation sank in June at 0.2%, with Core inflation, which excludes food and energy costs, at 0.4% in June, compared with 0.6% in May. PPI sank 5.4% in June from a year earlier, while the annual decline in June was China’s ninth consecutive drop and its steepest since December 2015.

RBNZ Inflation Expectations for Q3 (QoQ) (NZD, GMT 03:00)

Thursday – 10 August 2023 -----------------------------------------------------------------------------

Consumer Price Index and Core (USD, GMT 12:30) – The CPI is expected to show gains of 0.2% for the headline and 0.3% for the core in July, after June gains of 0.2% for both the headline and core. CPI gasoline prices look poised to rise 0.5% in July. We expect dissipating upward pressure on core prices through 2023 as disruptions from global supply chain bottlenecks and the war in Ukraine subside. As-expected July CPI figures would result in a bigger y/y headline rise of 3.3% from 3.0% in June, versus a 40-year high of 9.1% in June. A persistent moderation in y/y gains should be seen for all the inflation gauges through 2023 that will trim pressure on the Fed to tighten monetary conditions.

Friday – 11 August 2023 -----------------------------------------------------------------------------

Gross Domestic Product (GBP, GMT 06:00) – GDP is the economy’s most important figure. Q4’s GDP is expected to be unchanged at 0% q/q and 1.1% y/y.

Producer Price Index (USD, GMT 12:30) – July PPI gains of 0.1% for the headline and 0.2% for the core are expected, after June rises of 0.1% for both the headline and the core. As expected readings would result in the y/y headline PPI metric rising to 0.6% from 0.1%, versus an all-time high of 11.7% in March of 2022. We expect the y/y core measure to fall to 2.2% from 2.4%, versus an all-time high of 9.7% in March of 2022. The y/y calculation has fallen sharply through mid-2023 as comparisons have become much easier.

Michigan Sentiment (USD, GMT 14:00) – The US consumer sentiment printed 71.6 for the final July reading (was 72.6 preliminary). It is up 7.2 points on the month after rising 5.2 points to 64.4 in June. Confidence has been recovering from the -5.0 plunge to 62.0 in March on the fallout from the SVB collapse and related banking fallout. This is the strongest since October 2021’s 71.7 and is now well above the record nadir of 50.0 from June 2022.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

arket Update – August 7 – ‘Soft landing’ or even ‘no landing’?

Trading Leveraged Products is risky

A smaller than expected 187k NFP rise and -49k in downward revisions to May and June provided the spark for the bond market to correct from the post-Fitch and supply driven selloff. The belly of the curve outperformed as the jobs report did not alter Fed policy expectations and the markets continue to price in only about a 33% risk for another rate hike. The steepening of the 2-year/30-year yield curve by 30 basis points was one of the biggest weekly moves in over a decade. The ‘soft landing’ or even ‘no landing’ narrative is gathering momentum, and JP Morgan on Friday became the latest Wall Street bank to remove or delay their US recession call. Stocks initially rallied on the employment headlines, but spillover from disappointing Apple earnings results, which overshadowed Amazon’s beat, saw buying peter out and profits taken through the afternoon.

This morning: German industrial production contracted -1.5% m/m in June – more than anticipated after two strong months of orders inflow for the manufacturing sector. The strong bounce in manufacturing orders offers some hope for the coming month, but construction is likely to continue to struggle. Consumption may have strengthened in the second quarter, but these numbers leave the risk of a downward revision to Q2 GDP.

*FX – USD Index rose at 102.05, EURUSD fell back to 1.0980, USDJPY recovered some losses but is struggling to break 142.30. Cable holds at 1-month lows, currently at 1.2720.

*Stocks – The US100, US500 and MSCI World index last week all registered their biggest weekly losses since March. Amazon closed +8.27% and Apple at -4.8%. Today, Asian share markets were in a cautious mood, JPN225 is flat, EUROSTOXX 50 -0.3%, UK100 0.5%, US500 +0.3% and US100 +0.5%.

*Commodities – USOil at $82.85, after Saudi Arabia and Russia confirmed that they will extend voluntary output cuts. Ukraine added a new front in its war against Russia over the weekend, using drones to strike a naval vessel at a Russian oil-exporting port in the Black Sea and an oil tanker in the Kerch Strait.

*Gold – pulled back to $1935.44 below PP.

Today: July CPI and earnings out of Disney will highlight the calendar this week. Asia’s corporate earnings season picks up this week, with Alibaba the standout in a trickle from China.

Biggest Mover: (@6:30 GMT) GBPUSD holds at 1-month lows. It is approaching the resistance line of a down channel Support: 1.2620.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 8 – Risk Appetite Picked Up.

Trading Leveraged Products is risky

Risk appetite picked up,the US Dollar has been supported as Yields backed up and US futures outperformed. On the other hand, the advent of the August refunding supply left Treasuries heavy, especially in the wake of the debt warnings from the Fitch downgrade. Further erosion in recession outlooks contributed to the rally while the mix of earnings made for choppy upside action. Markets are looking ahead to this week’s US inflation report, after Fed’s Bowman suggested over the weekend that more hikes may be needed. NY Williams also left the door open for more hikes. Overnight we had seen China exports plunge again, which weighed on confidence.

*FX – USD Index is choppy and holds close to 102. EUR and GBP corrected amid weak economic data and as confidence in a soft landing for the US strengthened. EURUSD sideways at 1.10, Cable holds in the downchannel, currently at 1.2765. USDJPY extended 143.45.

*Stocks – The US30 led the way with a 1.16% surge, recovering from 3 straight declines. The US500 advanced 0.90% and the US100 was up 0.61% after 4 consecutive drops on both indexes. #BeyondMeat abandoned its hopes of becoming cash flow positive this year and cut its sales outlook, sending its shares down more than 8% in extended trading.

*Commodities – USOil has corrected from recent highs and is currently settled at $80.90.

*Gold – Ranging within $1930-$1938 area.

Today: FOMC Member Harker speech, Eli Lilly, UPS, Duke Energy earnings on tap.

Biggest Mover: (@6:30 GMT) NZDUSD (-0.76%) broke August lows at 0.6060. Next immediate support levels are set at 0.6050 and 0.6030.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 9 – Defensive Stock Markets.

Trading Leveraged Products is risky

Treasuries put in a good day, finding a solid bid as poor Chinese trade data elevated fears over global growth again. Also, there was weakness in the regional banking sector after Moody’s downgraded 10 small and medium sized banks. Fedspeak supported too after Harker and Barkin indicated the FOMC could probably be patient, though more data will be needed to make sure. Stock markets across Asia were mostly under pressure as yesterday’s bout of risk aversion lingered. Yields continued to decline and Bonds are also higher in Europe and the US, while European and US futures are finding buyers after yesterday’s sell off. Falling wages and the speculation of additional stimulus measures for China are also adding support.

Overnight: China faces deflation as data for July showed that both consumer and producer prices dropped versus July 2022. CPI was down -0.3% y/y, the first decline since February 2021. PPI contracted -4.4% y/y, which was the 10th consecutive month of negative annual rates. It was the first time since November 2020 that both consumer and producer prices were in negative territory and the numbers are a further sign that both consumers and businesses are struggling, with plunging demand for exports and weak consumer spending weighing on the economy. The data will add to pressure on officials to do more to boost activity.

*FX – USD Index corrected from yesterday’s highs and is at 102.334 as risk appetite improved. EURUSD sideways at 1.0970, Cable retests at 1.2800.

*Stocks – Wall Street ended in the red but off of early lows. The US100 declined -0.79%, while the US30 was down -0.45%, with the US500 falling -0.42%. Financials and materials underperformed. The JPN225 closed with a -0.5% loss, Hang Seng and CSI 300 are also in the red. AMC rose nearly 3% after hours, while it has risen about 26% so far this year. AMC said that the current quarter was off to a strong start, driven by box-office hits such as Barbie and Oppenheimer, after posting a surprise profit and beating second-quarter revenue estimates.

*Commodities – USOil spiked to $82.62.

*Gold – was 0.3% higher at $1,930.18.

Today: Disney earnings on tap.

Key Mover: USOIL retests 10-month resistance, while it has fully recovered the week’s losses and is currently settled at 82.70.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 10 – Disney missed forecasts – US Inflation ahead!

Trading Leveraged Products is risky

Yields have moved higher, but stock market sentiment also improved as investors look ahead to key US inflation data. The Hang Seng underperformed overnight, but elsewhere indexes managed to move higher. European markets are narrowly mixed at the start of the session, US futures are moving higher. Bonds have pared overnight losses, but the US 10-year rate is still up 1.3 bp at 4.018%, while Bund and Gilt yields have lifted 2.7 bp and 2.4 bp respectively. Fears that the CPI report might be too elevated to keep the FOMC sidelined in September elicited profit taking on recent gains. In earnings front, Disney missed revenue forecasts, Disney reporting that streaming losses totaled $512 million in its fiscal third quarter, about half of the $1.1 billion loss reported in the prior-year period and less than the $777 million loss forecast by analysts. European gas prices rose 30% on fears over Australian supply.

Overnight: China faces deflation as data for July showed that both consumer and producer prices dropped versus July 2022. CPI was down -0.3% y/y, the first decline since February 2021. PPI contracted -4.4% y/y, which was the 10th consecutive month of negative annual rates. It was the first time since November 2020 that both consumer and producer prices were in negative territory and the numbers are a further sign that both consumers and businesses are struggling, with plunging demand for exports and weak consumer spending weighing on the economy. The data will add to pressure on officials to do more to boost activity.

*FX – USDIndex was little changed at 102 after trading in a narrow range from 102.29 to 102.58. EURUSD higher at 1.1020, Cable jumped to 1.2760 from 1.2705.

*Stocks – The US100 underperformed, sliding -1.17% on the weakness in big tech. The US500 dropped -0.7% and the US30 declined -0.54% with IT leading the way lower.

*Commodities – USOil spiked to $84.26 breaking 11-month highs, supported by the spike of gas. European natural gas prices surged more than 30%, as the potential for liquefied natural gas supply disruptions from Australia spooked traders who have been betting against the price. A pop in USOIL prices to 11-month high at $84.65 added to anxiety over inflationary pressures.

*Gold – is ranging at $1,915- $1,920.

Today: US inflation and Jobless claims.

Biggest FX Mover: CHFJPY (+0.56%) spiked to 164.89, with 165 the next resistance level.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

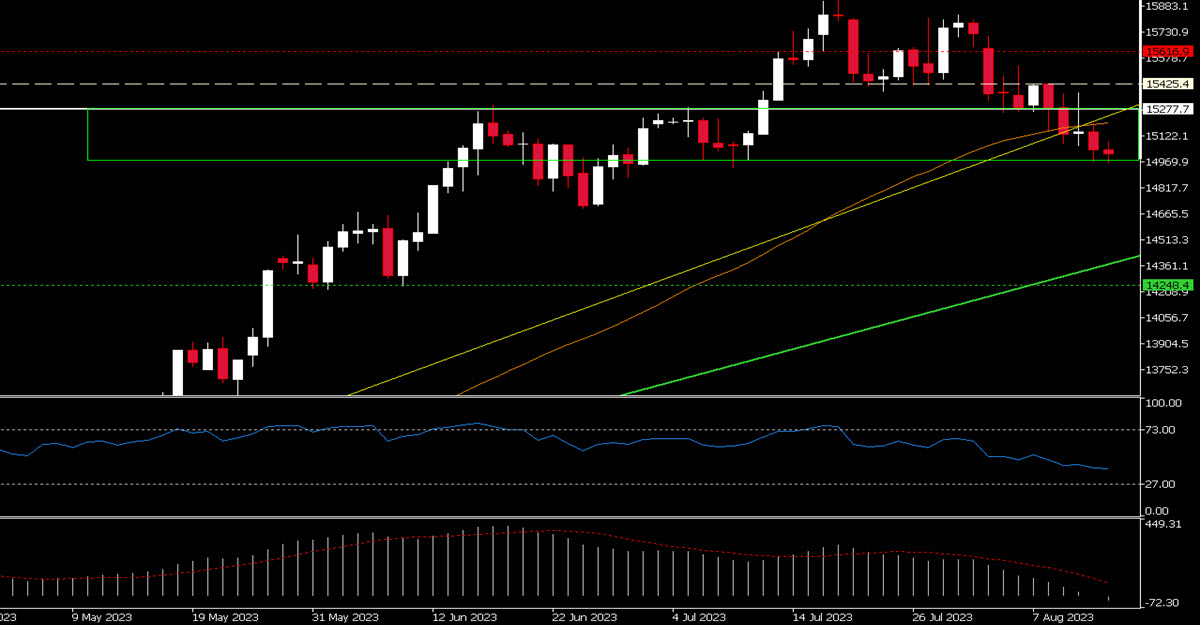

Market Update – August 14- CNH, CHINA50 slide, JPY nears 2022’s intervention zone, PPI ticks up.

Trading Leveraged Products is risky

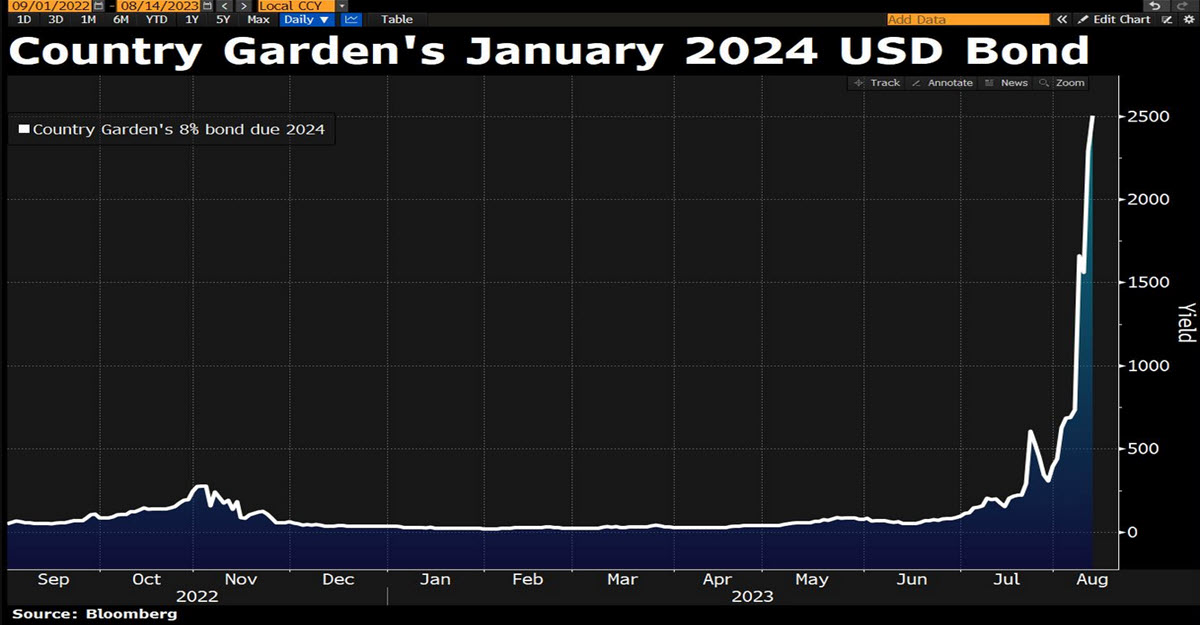

Asia is in dire straits: CHINA50 and HK are down more than 2% as problems with developer Country Garden intensify and the stock is down almost -15% at its lows after suspending trading on 11 onshore bonds. Its issuance dated 01/2024 has fallen as low as 9 cents, indicating a yield of 2500%: a bankruptcy now seems inevitable, it remains to be seen how much the system will be able to sterilise it. The USDCNH currently trades at 7.2757, what would be the highest settlement of the year. But it is not the only one: the USDJPY touched 145.20, a new one-year low for the yen. Last year above 146, the BOJ’s monetary defence with open market interventions had begun and many traders expect something similar this year.

Back in the West, a higher-than-expected PPI figure favoured another red day for the US indices from which only the US30 was saved: that’s two weeks in a row of declines for both the US500 and US100. Remember that producer prices move ahead of consumer ones. Meanwhile, the USD continues to rise for the fourth week in a row and so does the Crude, up for 7 weeks in a row: the energy sector is now the best performer and has largely overtaken technology in short-term performance. Rates are on the rise again with the 2y at 4.90% and the 10y at 4.17%.

*FX – USDIndex up for weeks in a row trading at 102.80 now, approaching the channel down and the 200MA; both EURUSD and CABLE are -0.10% (1.0938, 1.2681) and seem to be close to break down their 10 months long uptrends.

*Stocks – US futures are -0.2% this morning, JPN225 -1.44%, AUS200 -0.87%, DAX -0.4% and clearly trading below its 50MA (as US100 is).

*Commodities –USOil -0.96% at $82.24, UKOil -0.93% at $85.58, another red day for Copper ($370).

*Gold – Down at $1913 as yield are rising.

Today: No data till tonight when Japanese GDP, RBA minutes and Chinese Retail Sales + Industrial Production will hit the tape.

Interesting Mover: US100 (0.15%) is trading below its 50MA and have broken the first steepest (yellow) trendline. 14935 area is now a weak static support.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

BRICS Summit’s Bold Gambit: The Drive Towards a New Currency Takes Centre Stage.

Trading Leveraged Products is risky

The BRICS summit serves as a gathering of strategic minds hailing from Brazil, Russia, India, China, and South Africa — a formidable union constituting nearly a quarter of global GDP and embracing 40% of the world’s populace. This annual convergence navigates a spectrum of vital concerns: trade, investment, innovation, development, and the orchestration of global governance. The 15th BRICS summit is set to unfold from August 22 to 24, 2023, with Sandton, South Africa’s iconic skyline, painting the backdrop.

At the epicentre of this summit rests a notion that could potentially recalibrate the global financial paradigm: the inception of a unified BRICS currency. It is a proposition with profound implications, wherein some BRICS members are aiming to offer an alternative to the dominant US Dollar, which holds the reins of international trade and finance with an iron grip—commanding 88% of global transactions and 58% of foreign exchange reserves. Yet, BRICS nations have weathered the dollar’s storm—navigating sanctions, trade tensions, debt quandaries, and inflationary waves.

Endeavours to free their economies from the dollar’s grasp are well underway. Consider Russia and China begging to trade in their own currencies, or the flourishing partnerships fostering alternatives such as the Euro and Gold. The potent Yuan has knitted stronger ties between Brazil, India, and China, while the New Development Bank (NDB) stands tall as a testament of their collective might—enabling BRICS to channel investments into robust infrastructure and sustainable dreams, all while dealing in their own currencies.

However, fashioning a new currency is like sculpting a masterpiece. The path forward is laden with challenges, such as a delicate choreography of design, governance, issuance, distribution, exchange rates, and global acceptance. As they embark on this journey, we also have to acknowledge the differences in economic magnitude, structure, policy orientation, and strategic visions between these countries. These divergent elements, while inspiring, present challenges to the harmonious orchestration of a new currency.

The dollar’s supremacy will not crumble overnight. Its roots run deep, fortified by the intricate web of global finance and unwavering trust. Governments, banks, corporations, investors, and individuals alike view the Dollar as a paragon of value, a cornerstone of commerce, a sanctuary for assets, and a bedrock for reserves. The allure of the US financial markets adds to its enduring power.

The pursuit, though risky, promises metamorphosis. Imagine a new BRICS currency, vibrant and resilient, standing shoulder to shoulder with the Dollar. Should it emerge as a contender, it could provide a much-needed alternative, branching out international trade and finance. The repercussions would resonate, and potentially see the dollar’s dominance challenged, its grip weakened, and the stage set for a more diverse financial narrative. Beyond the tangible, if successful the new currency could shield the countries within BRICS from the tempestuous winds of external shocks and dollar-driven fluctuations. It could amplify their voice in global economic governance, adding to the world’s economic discourse.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – 21 August – PBOC disappoints, markets quiet.

Trading Leveraged Products is risky

APAC stocks traded mixed as the disappointment from China’s decision on its Loan Prime Rates overshadowed its recent support efforts; Hong Kong underperformed. PBOC opted for a narrower-than-expected cut to the 1-year LPR alongside a surprise hold on the 5-year LPR, which is the reference rate for mortgages. PBOC and regulators met with bank executives and told lenders to boost loans to support the economic recovery instead. Meanwhile Country Garden has been delisted from the Hang Seng as the real estate sector in China crumbles before our eyes.

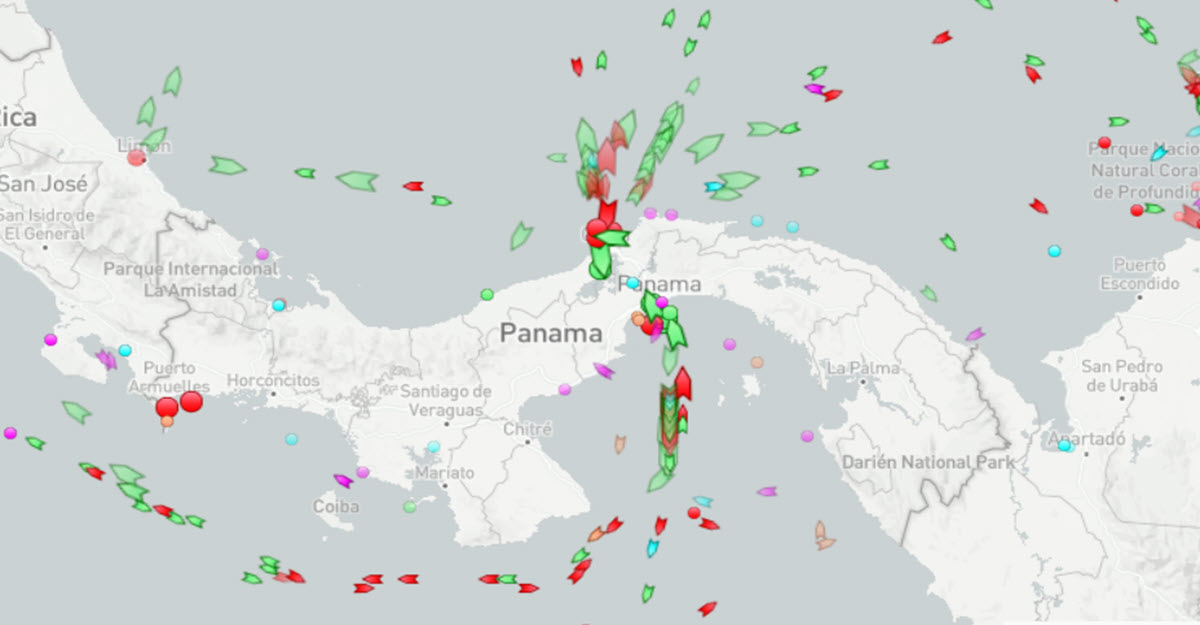

US500 futures were little changed on Sunday night after another losing week for the major averages: US100 closed the week lower about 2.6%, down for a third straight week for the first time since December. Meanwhile, the Dow closed the week lower by 2.2%, its worst streak since March. And the S&P 500 dropped 2.1% and posted its third consecutive losing week, which hadn’t happened since February. German PPI are just out, showing another consistent decline, but Unions at Woodside Energy’s North West Shelf offshore gas platforms on Sunday announced plans to strike as early as September 2nd, sending EU Natural Gas +18% this morning. On the inflation side we also have Japan, which is set to increase minimum pay by a record amount as inflation takes hold and 200 cargo ships are stuck waiting to cross the Panama Canal Water as shortages caused by the worst drought in 100 years have forced the canal operators to reduce the flow of traffic, which could have consequences for the global supply chain also as a result of what appears to be a still strong American consumer market.

Panama channel congestion real time

*FX – USDIndex is steady above 103 (103.32 now) and well above its 50-200 MAs; USDJPY found support above 145 (145.45 now), USDCNH heading north (7.33). NZDUSD keeps drifting lower (as does AUDUSD) after the Trade Balance data. Cable flat and lateral (1.2690 – 1.2765).

*Stocks – US and EU Futures are flat, Hong Kong slides again (-1.60% at 17631) despite Country Garden delisting.

*Commodities – USOil keeps recovering some ground, currently +0.61% at $81.88, the same for Copper steady at $371.20 after rebounding from the trendline last week.

*Gold – flat at $1,889 as is Silver ($22.75).

Today: No more relevant data after PBOC rate decision and German PPI earlier this morning.

Interesting Mover: VIX (-0.27%) @ 18.45, is pulling back after having tested its 200MA on Friday (Opex day); It’s finally back above the area that has been support after 2020 and should consolidate here. A move to the upside would have the 20.50-22 area as the next target.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

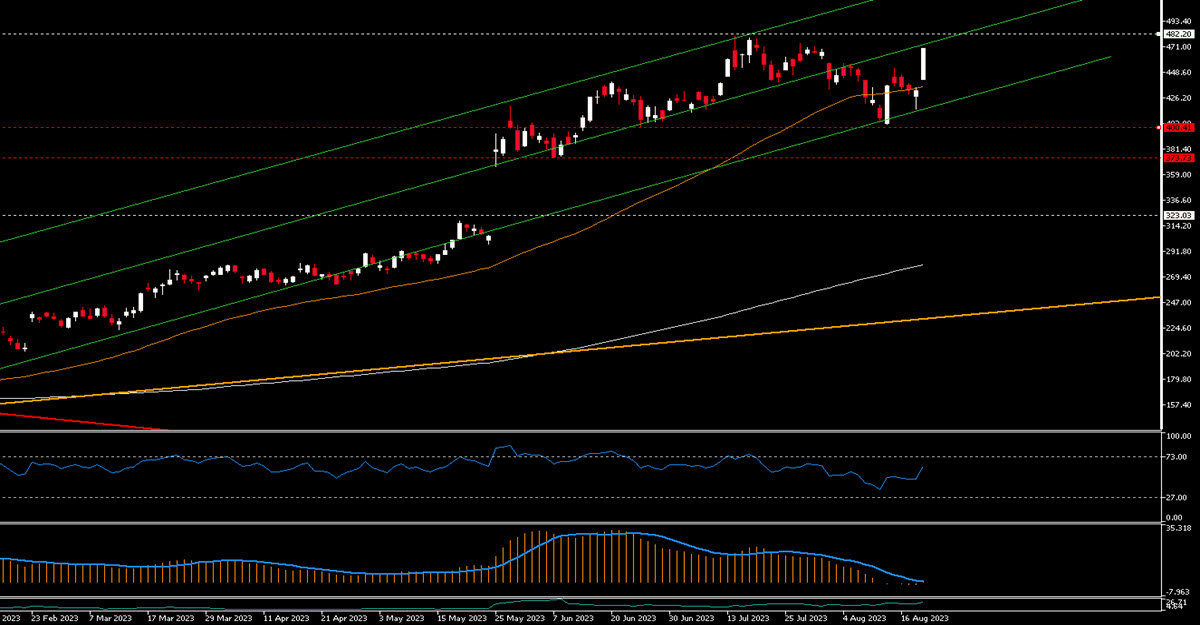

Market Update – August 22 – US 10 year yield hits decades-long high, Tech rallies.

Trading Leveraged Products is risky

Futures are marginally higher this morning after US100 and US500 snapped a four day negative streak yesterday with the tech heavy index posting its biggest advance of the month (+1.65%) boosted by Tesla and Nvidia‘s performances. The chip maker rose 8.47% after being upgraded by HSBC (target price $780) and only 2 days before the much-anticipated earnings report that will come out Wednesday after the bell when we’ll find out whether the company’s revenue forecast – which was 50% higher than Wall Street estimates – will come to fruition. The Tech rally held despite yields on US Treasuries spiking again with the 10Y closing at 4.342% – its highest level since November 2007 – the 2Y trading above 5% and 10Y real rates shortly hitting 2%. Typically higher rates are negative for tech and growth stocks as they affect their future flows discount (despite of their cost of financing) but this was not the case yesterday. On the stock side, Softbank’s chip unit ARM is set to list at Nasdaq, becoming the largest IPO of 2023. Also, Zoom shares climbed around 4% after the close after reporting earnings that beat expectations.

*FX – USDIndex is trading at 103.04 right now (-0.16%), EURUSD is north of 1.09 (1.0918, +0.21%) and trading between its 50 and 200 MAs as CABLE is doing (1.2784). USDJPY is pulling back (145.89) after having touched 146.50 overnight.

*Stocks – US and EU Futures marginally higher (+0.07% US30/+0.15% US100/+0.16% GER40); JPN225 rose 0.9% on tech strength while China slipped on Miners weakness.

*Commodities – USOil -0.15% at $80.76 after having pulled back from $82.44 yesterday; Copper is catching a bid (+0.7% at $374.5) as are other metals (Palladium +0.62%, Platinum +0.82%).

*Gold – Shy of $1900 despite higher rates.

Today: EU current account, Richmond Fed Index, speeches from Fed’s Barkin, Bowman & Goolsbee.

Interesting Mover: Nvidia rose 8.47% to $469.67, jumping above its 50-day MA and putting its recent highs ($480) in sight. Seems to have found support on the lower bound of an extremely steep channel; RSI heading higher and not overbought.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 23 – Waiting for Nvidia, PMIs & Jackson Hole.

Trading Leveraged Products is risky

On a day when Monday’s optimism had already faded in US markets, weighed down by both a new downgrade of the banking sector’s credit rating – this time by S&P – and the pullback of NVDA, one of the most interesting movements was the USD. Without any real news flow and without any abrupt movements in the bond market, the US currency appreciated steadily throughout the day – slowly but surely – especially against the currencies of the European continent (the YEN was saved from the selling and this is another piece of news). This was a purely technical movement, without any important levels being vulnerable – an adjustment of flows – but the EURUSD for example fell 97 pips from the highs to the lows of the day. All this on the day that the BRICS meeting in Johannesburg started, there was talk of ”inevitable de-dollarisation’‘ and President Putin assured that the trade in USD between the constituent countries is now only 28%. Back on the corporate side, retail is showing much more mixed results than the official stats show: yesterday MACY‘s dropped 14% after reiterating its conservative outlook, while LOWE‘s rose 3% after beating expectations; Nike has been down for 8 consecutive sessions, its worst streak ever. Today will see Peloton, Foot Locker, Abercrombie and especially NVIDIA after the close: implied volatility in the options market is for an 8.8% move after the results. Today is PMI day, tomorrow the Jackson Hole Symposium kicks off.

*FX – USDIndex -0.05% at 103.42 after rebounding on its 200 MA yesterday; EURUSD sitting on its ST support (1.0855), CABLE 1.2748, YEN eked out a gain yesterday and is now trading at 145.667. USDCNH < 7.30.

*Stocks – US and EU Futures higher (+0.28% US30/+0.56% US100/+0.42% US500/ +0.34% GER40); China50 -0.59% despite good BAIDU earnings results.

*Commodities – USOil is below $80 ($79.54 now), UKOil relatively stronger at $83.87.

*Gold – Rising at $1904.41, XAG outperforming (-1.17% at $23.67).

Today: HCOB PMIs Composite, Manufacturing, Services in Germany, France, Europe, SP PMIs in UK, US, Home Sales in US, European Consumer Confidence.

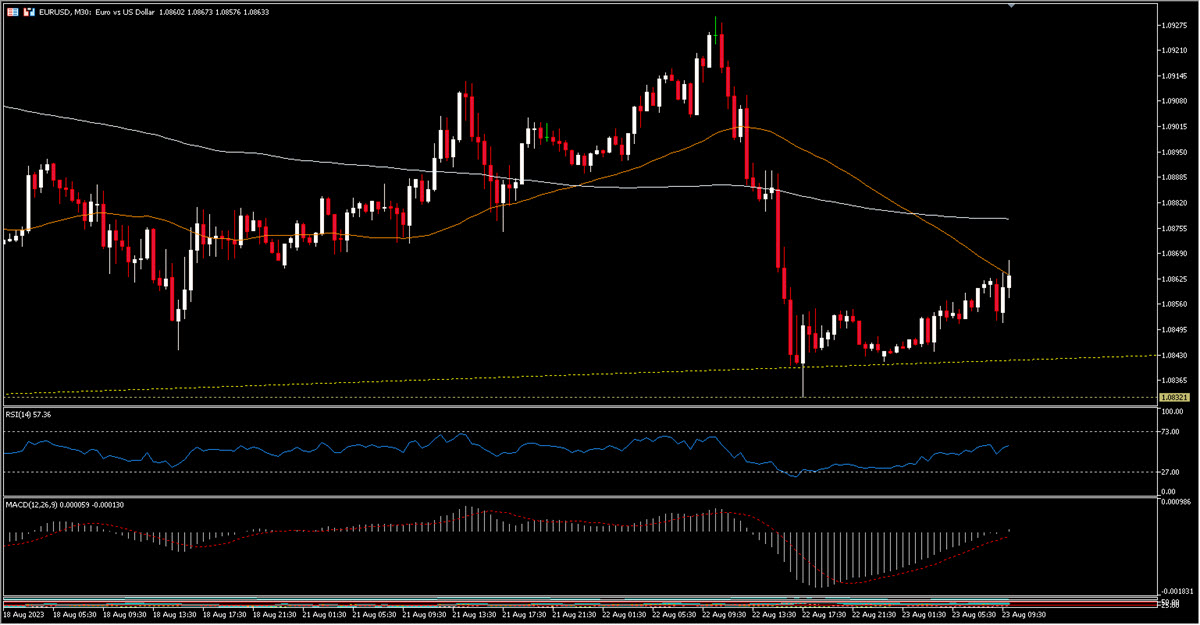

EURUSD, 30 mins

Interesting Mover: EURUSD (+0.12% @ 1.0859) hovering around the support area of 1.0840/1.0855 after falling from a high of 1.0930 to a low of 1.0832 yesterday. MA 200 at 1.08.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 24 – NVDA posts stellar Q2 results; Stocks, Bonds, Metals rally on eve of Jackson Hole.

Trading Leveraged Products is risky

Let’s start with NVIDIA that after the close reported results of a stellar Q2 and topped analyst estimates both on Revenues ($13.51 billion vs $11.22 billion expected) and EPS ($2.70 vs $2.09). The company raised its forecast again and expects its Q3 revenues to climb to $16 billion, an increase of 170% y/y. Gains are driven by the data center business. In after hours trading the chip-maker rose 6.57% also driving up AMD (+4%) and TSMC (+3.1%). Indices added to this week rally despite weak PMIs data around the Developed Markets that instead weighted on local currencies: EUR, GBP and USD fell in this order during the day after lackluster readings. Interestingly, the EURUSD perfectly rebounded on its 200 MA.

US 30y mortgage rate soared to 7.31% and this led to the lowest Mortgage applications since 1995: despite that, US new home sales rose in July. Bonds rallied around the world with the UK Gilt up 2.13% after traders repriced the terminal rate well below 6% and a narrow majority of economists polled by Reuters now believe the September hike to 5.5% will be the last one. German Bund gave up >10 bps and the 10y US T-note is 17bps off this week’s high. All of this gave wings to Gold, which touched $1921, and especially Silver, which rose 3.88%. Overnight, Asia joined the party and China50 rebounded strongly from near one-year lows.

US Mortgage 30 Years Rate and Mortgage Applications

*FX – USDIndex -0.05% at 103.28, EURUSD flat at 1.0865 after falling as low as 1.0802 yesterday, GBPUSD -0.09% @ 1.2713 still between the recent 1.2615/1.2785 range, USDJPY back above 145 (breached yesterday).

*Stocks – US Futures almost flat (-0.05% US30/+0.16% US100/+0.05% US500), EU Futures up 0.4%/0.6%; CHINA50 +1.42%, Hang Seng +1.91%, JPN225 +0.79%.

*Commodities – USOil is below $79 ($78.48 now) despite the bigger than expected drain from Oil Stocks (EIA data).

*Gold – holding at $1921, XAG consolidating at $24.23 after yesterday’s rally.

Later Today: US Durable Goods Orders, Jobless Claims, JACKSON HOLE kicks off.

Interesting Mover: USDIndex (-0.05% @ 103.28) pulled back after rising as high as 103.90 in what could be the test of the upper bound of a channel. It is trading above both the 50 and 200 MA and both RSI and MACD are positive and upward sloping.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – August 25 – Powell at Jackson Hole, inflation mission not accomplished yet.

Trading Leveraged Products is risky

US equity markets pulled back strongly yesterday with US30 having its worst day since March, US100 its second worst in August and US500 swinging down $105 from the daily high to the daily low and drawing a big bearish engulfing pattern. The mighty NVDA started trading up 6.50% and ended the day +0.10%; JPN225 leads losses in Asia this morning (-2%). Yields rose and USD strengthened. Markets are cautious before today’s Jerome Powell intervention at the Jackson Hole symposium. The general consensus is that he will try to stay neutral, with no big surprises but a slight tilt to the hawkish side. Nothing similar to last year of course: but the FED does not think its fight against inflation is won yet and the strong economic data give it some room to act. Some energy prices have started to rise again lately – see Oil or Gasoline – but also Rice and Pork Belly are getting extremely expensive: the Cleveland Fed inflation tracker anticipates August’s figures will show a noticeable jump. It’s not time to declare ”mission accomplished” yet.

There has been some chatter about R* lately: this is the neutral interest rate of an economy, a mostly academic concept difficult to calculate and around which, incidentally, Powell developed his first speech in Jackson Hole in 2018. Nick Timiraos is a WSJ journalist who is known to be very close to the FED and in a recent article he brought up the subject of if the long-term neutral rate had not moved up in the US. Just yesterday, the WSJ also published an article wondering whether it was not time for the Fed to move the inflation target towards 3%. Is this perhaps a test of the reaction of the most informed and sophisticated investors? The Fed in June capped the R-Star at 2.5%: who knows if Powell will say anything about that and if there will be any news in September.

We shall see at 14:00 GMT.

*FX – USDIndex > 104 (104.12), EURUSD below its 50MA at 1.0783, GBPUSD 1.2570 (-0.24%), USDJPY 146.06, USDTRY pulling back (26.52) after the big drop yesterday following the hike to 25%.

*Stocks – US100 closed -2.19%, US500 -1.35%, US30 -1.08%; NVDA +0.10%, TSLA – 2.88%, MSFT -2.15%, AAPL -2.62%, META -2.55%, GOOGL -2.09%.

*Commodities – USOil in green for a second day, +0.65% at $79.36, Palladium keeps falling (-0.82% after yesterday’s -2.88%).

*Gold – $1913, XAG -0.35% slightly above $24.

Later Today: Jerome Powell’s speech at Jackson Hole, German IFO, US Michigan Consumer Sentiment index, ECB’s Lagarde speech. German GDP out at -0.2% y/y.

Interesting Mover: US500 (-1.35% the cash close @ 4376) gave up $105 (or roughly 2.5%) from the intraday high after testing from the downside the 50d MA and drawing a big bearish engulfing pattern.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Rates differential is only one part of the equation but ECB has it still tough – EURUSD.

Trading Leveraged Products is risky

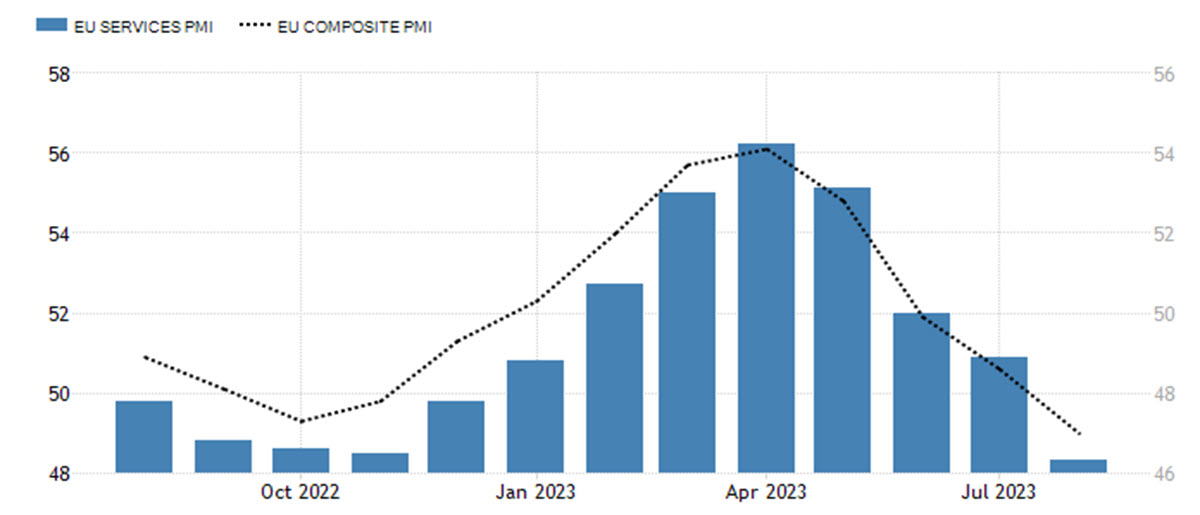

It is widely believed, not without reason, that the task of Lagarde and the ECB is far more difficult than that of her counterpart across the ocean. The PMI data of a few days ago showed grim future prospects, not just for manufacturing which we are used to by now. The leading data on services also returned to contraction after 7 months (48.3), following the composite that relapsed below the critical threshold two months ago. GDP growth for Q2 was not bad (+0.3%), but heavily influenced by the strong Irish figure while Germany continued to stagnate.

Services PMI lhs, Composite PMI rhs

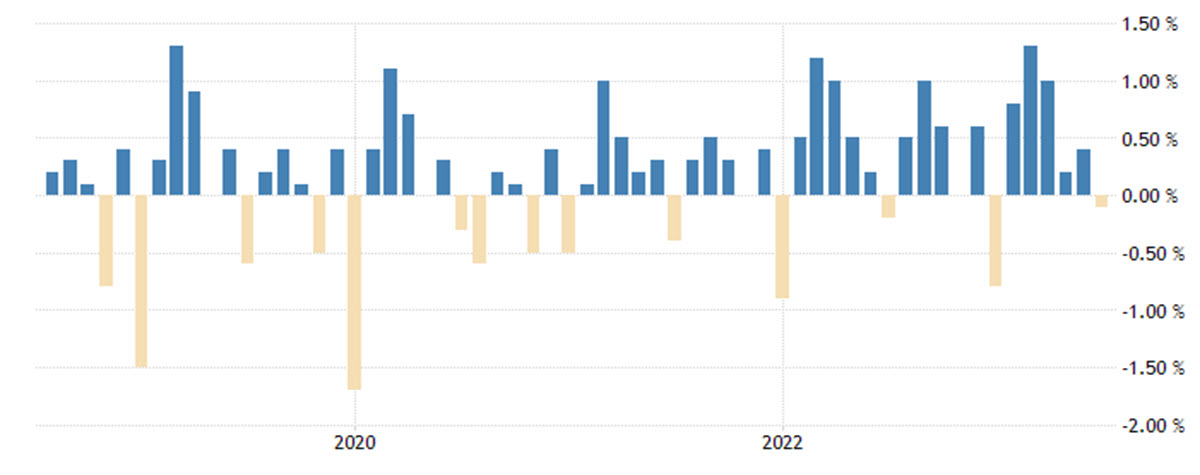

At the same time, price pressure continues to be too high, especially in the service sector, due to wage pressures. True, the PPI has been declining m/m since the beginning of the year and is now in deflationary territory, but both core and headline consumer inflation readings are above 5% (5.5% and 5.3% respectively). If we look at the monthly data, both measures decreased in July but only imperceptibly (+0.1%) and for the first time after 5 months of increases.

Core Inflation m/m

That is why in Jackson Hole last Friday, the president of the ECB said central bankers had to be “extremely attentive that greater volatility in relative prices does not creep into medium-term inflation through wages repeatedly ‘chasing’ prices’’ and that “if global supply does become less elastic, including in the labour market, and global competition is reduced, we should expect prices to take on a greater role in adjustment’’.