Market Update – November 29 – Tightening Tilt, COVID Control & Month End Flows.

Trading Leveraged Products is risky

*The USDIndex rallied to 106.70 in the previous session but formed a correction in Asia session to 106.00 ahead of a COVID-19 press briefing in China that is spurring hopes of a potential easing in the country’s strict pandemic restrictions.

*Fed Officials Signal Higher rates: Hawkish reminders from key Fed officials Williams, Bullard, and Brainard that rates will have to go higher helped weigh on the markets in Monday action. Wall Street was weaker overnight on the back of Williams’s and Bullard’s comments, and slipped further as Brainard tripled down on the rate outlook.

*US houses prices fall like in 2008.

*Stocks – Global stocks rise after yesterday’s dip. US100 and US500 dropped -1.58% and 1.54%, respectively, with the US30 off -1.45% amid broadbased weakness. Today however the rumours of an earlier easing of strict COVID-19 restrictions along wihth vaccinations for over 80-year olds, found buyers in the stock market with a Chinese stocks rebound. Hang Seng and CSI 300 bounced 4% and 3% respectively. ASX and Nikkei closed narrowly mixed. GER40 and UK100 futures are up 0.5% and 0.4% respectively.

*EUR – reversed from 5-month peak. Currently at 1.0360. ECB’s Lagarde said overnight that inflation had not peaked and it risks turning out even higher than currently expected, hinting at a series of interest rate hikes ahead.

*JPY along with Yuan, Aussie and Kiwi on bid.

*GBP – turns again below 1.20 at 1.1987.

*USOil – jumps to 80.00 as China refines its approach for dealing with protest and Covid control. All eyes are on weekend OPEC+ meeting. EU fails to agree on Russian oil price cap once again.

*Gold – fully recovered yesterday’s losses, currently at $1754.

Today – Swiss GDP, German HICP , Canadian Q3 GDP, US Consumer Confidence and BOE Governor Bailey speech.

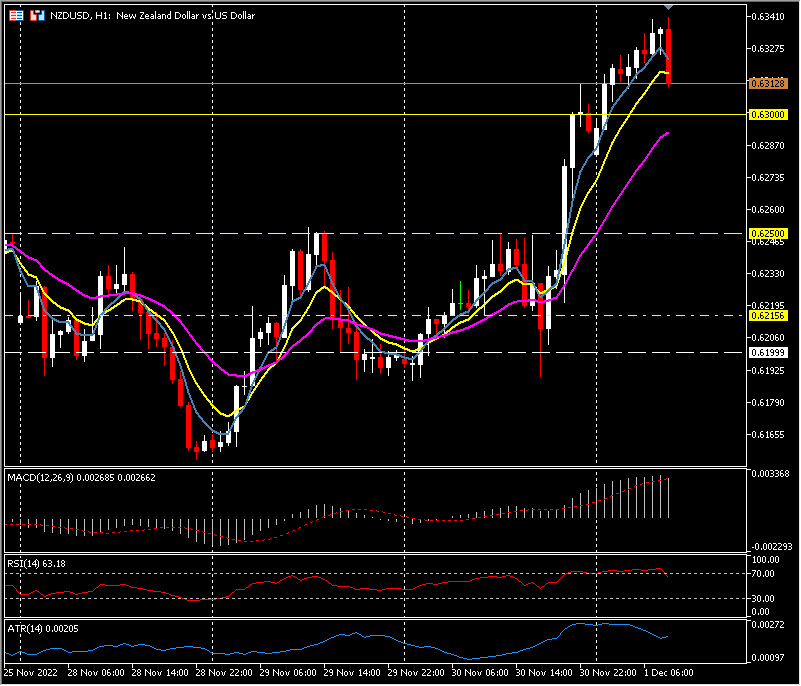

Biggest FX Mover @ (07:30 GMT) NZDUSD (+1.10%), bounces to 0.6235. MAs aligning higher and RSI at 63 but MACD histogram & signal line remain below 0. H1 ATR 0.00147, Daily ATR 0.00962.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex slightly below 1-week amid reports of a softer stance on Covid emerging in China’s official rhetoric, which is keeping hopes alive that there won’t be a move back to tighter restrictions. All eyes are on an expected hawkish stance from Chair Powell’s speech today.

*Stocks – The Nikkei closed with a -0.2% loss, the ASX managed a 0.4% gain and Hang Seng and CSI300 are currently up 1.1% and 0.1% respectively. GER40 and UK100 futures are up 0.6% and 0.4% respectively. US futures are underperforming, but also managing slight gains. Wall Street closed mixed with the NASDAQ dropping -0.59% on weakness in tech and the rise in yields.

*Japan’s factory output fell for a 2nd consecutive month in October, and China’s factory activity contracted at a faster pace in November, weighed down by softening global demand.

*JPY – is holding in the 138-139 range.

*USOil – supported ahead of the OPEC+ meeting on December 4. Energy was lifted by easing in China jitters.

*AUD & NZD downward pressure from worse than expected Chinese manufacturing surveys.

*Gold – extends gain to $1757.

Today – Attention is on Powell’s speech later today, who is likely to reinforce yesterday’s hawkish Fedspeak from Williams, Bullard, and Mester who all stressed rates are headed higher still and could remain so for some time. Elsewhere is EU HICP, US ADP and Q3 GDP.

Biggest FX Mover @ (07:30 GMT) GBPAUD (-0.25%), declined to 1.7816 from 1.7930. MAs aligning lower and RSI at 34.8 and MACD histogram & signal line remain below 0. H1 ATR 0.00267, Daily ATR 0.01538.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*The USD Index has tanked to 105.30 lows today from over 107.10 as Chair Powell more or less confirmed a 50bp hike at the next FED meeting, was sanguine about the terminal rate being over 5% and reiterated (again) that the fight to bring down inflation was far from over. He was as Hawkish as had been expected. Stocks & Treasuries ripped higher with optimism about China’s reopening prospects even after mixed US data yesterday.

*EUR – retakes 1.0450 from under 1.0300 lows yesterday..

*JPY – collapsed to under 136.00 today from 139.85 highs yesterday –

*GBP – Sterling rallied over 200 pips from 1.1900 support and lows to 1.2110 now.

*Stocks – Wall Street erupted higher 2.18%-4.41% (NASDAQ best performer) – US500 +122.48 (+3.09%) closed over 4000 at 4080, has gained 13.8% in 2 months and is over it’s 200MA for the first time in 7 months. FUTS trades at 4085 now.

*USOil – Rallied to $81.50 and trades at $80.00 now. Inventories showed a huge 12.6m drawdown.

*Gold – Rallied to $1780 from $1745 lows, trades at $1776 now.

*BTC – Sentiment woes continue, SFB “I didn’t try to commit fraud”.. Weaker USD takes it over 17K.

Today – German Retail Sales, EZ, UK & US Final Manufacturing PMI, US ISM, Weekly Claims, PCE Price Index, EU Council President Michel visits China, Speeches from Fed’s Barr, Bowman & Logan, ECB’s Lane & Elderson.

Biggest FX Mover @ (07:30 GMT) NZDUSD (+1.57%) rallied from under 0.6200 yesterday and trades at 0.6320 now, next resistance at 0.6350. MAs aligning higher, MACD histogram & signal line positive & rising, RSI 65.00 & falling having been OB, H1 ATR 0.00203, Daily ATR 0.0083.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 2 – USD holds at lows & Stocks at Highs Ahead of NFP.

Trading Leveraged Products is risky

*The USD Index holds at lows not seen since August & June at 104.50 and significantly below the 200-day MA at 105.40. Weaker PCE inflation, lower JOLTS numbers, but tempered by a miss for Weekly Claims all added to pressure for yields too. 2/10 yr remains inverted by 71 bps. Stocks finished flat, Asian markets also flat except Nikkei (-1.59%) as JPY soars. All eyes on NFP; Consensus is a headline of 200k, less than 120k-150k and the USD could slip further, over 250-300k could lift the Greenback.

*EUR – broke over key psychological 1.0500 and holds at 5-mth highs at 1.0530 now.

*JPY – collapsed to under 135.00 today and trades at 134.60 from 139.85 on Wednesday, hitting Japanese stocks.

*GBP – Sterling rallied again to breach 1.2300, briefly and post 5-month highs. Trades at 1.2260 now.

*Stocks – Wall Street held on to Wednesday’s gains closing flat – US500 -3.54 (-0.09%) 4076, Big movers included losses for CRM -8.27%, COST -6.56%, Blackstone -7.06%. FUTS trades at 4076 now too.

*USOil – Rallied again (4 consecutive days) to breach $83.00 before cooling to $81.25 now. OPEC meet over weekend and into Monday possibly

*Gold – Rallied to and broke the key $1800 and holds at $1802 now.

*BTC – Sentiment woes continue, but a weaker USD means it holds at 17k.

Today – US & Canadian Jobs Reports, EZ Producer Prices, Speeches from ECB’s Lagarde & de Guindos, Fed’s Barkin & Evans.

Biggest FX Mover @ (07:30 GMT) NZDUSD (+0.52%) rallied again to test 0.6400 today from 0.6300 yesterday and lows on Monday at 0.6150. MAs aligning higher, MACD histogram & signal line positive but falling, RSI 69.00 & rising, H1 ATR 0.00127, Daily ATR 0.0083.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 5 – Dollar slips, Gold hovers around $1800.

Trading Leveraged Products is risky

*USDIndex back to 104 area for the 1st time since June, Global Stocks are up on the hopes of reopening of China ignoring the strength in the headline payroll gains and the pick up in earnings. USDINDEX down by 1.4% last week and 5% in November. (worst month since 2010)

*Yuan surge to its strongests levels since September as. China’s zero Covid pivot accelerates – announcing an easing of coronavirus curbs over the weekend as China tries to soften its stance on COVID-19 restrictions in the wake of unprecedented protests against the policy.

*Wall Street banks weighs 30% bonus cuts.

*Stocks boosted. The Hang Seng rallied more than 4%, the CSI 300 nearly 2%. Nikkei and ASX underperformed, but also managed fractional gains. GER40 and UK100 are little changed though and US futures slightly lower, as markets weigh the impact of China’s move on economies and central bank moves elsewhere. The US 10-year rate is up 5.4 bp at 3.54% at the moment, and the 10-year Bund rate is up 2.9 bp at 1.87%.

*Europe: The beginning of the G7’s $60-a-barrel price cap on Russian oil. Russia Rejects as it was expected!

*USOil – settled lower at $80.30 as Russia rejects EU cap. Jumped initially at $81.90 as China reopening would eventually brighten the outlook for global growth and commodity demand. OPEC+ left their quotas for oil production unchanged.

*JPY holds below 200-DMA, below $135.

*EUR – peaks to 1.0583 and GBP for a 3rd day above 200-DMA, at 1.2345.

*Gold – is hovering around $1800.

Today – Attention on US ISM services survey, European retail sales data today and Central bank meetings in Canada and Australia later in the week.

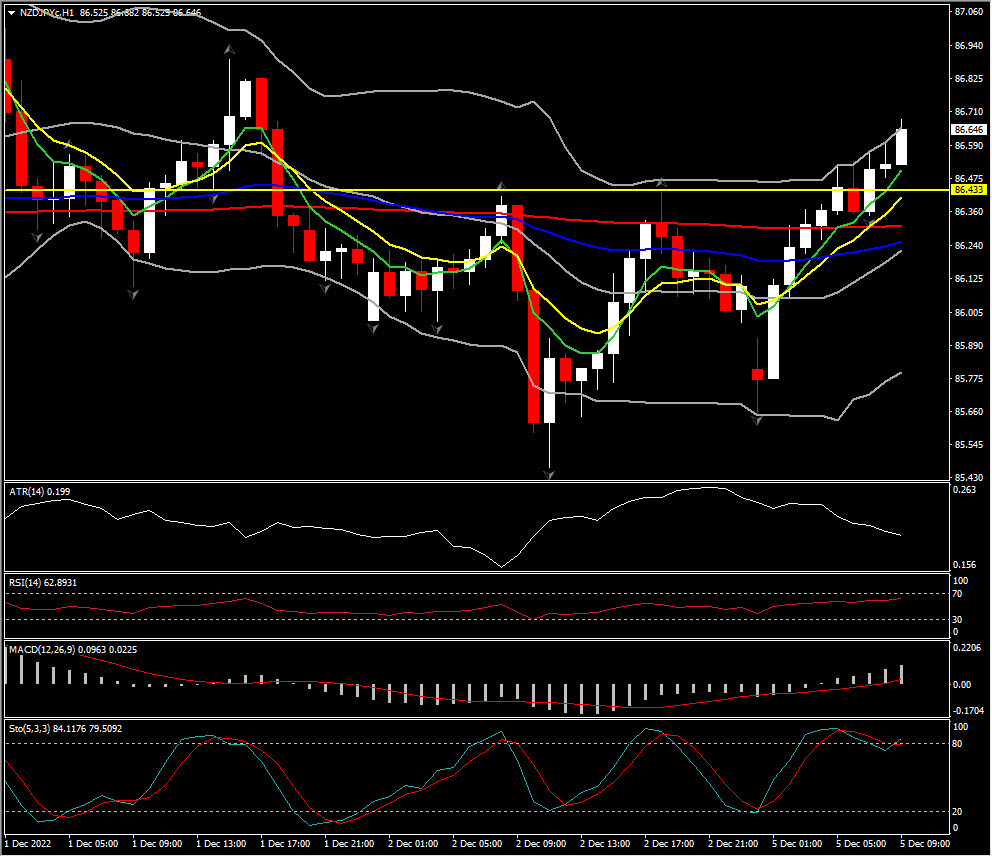

Biggest FX Mover @ (07:30 GMT) NZDJPY (-0.25%), jumps at 86.70 extending above all MAs. 5- and 9- EMAs aligning higher, RSI at 62 and MACD histogram & signal line rising above 0. H1 ATR 0.199, Daily ATR 0.889.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 6 – USD Rallies, Stocks off Highs, RBA Add 25 bp in Hawkish hike.

Trading Leveraged Products is risky

*The USD Index has climbed to 105.39 but off its 200-DMA following the stronger than data, including the ISM services and Factory orders reports that also showed still elevated price levels. The less hawkish Fed views & uncertainty over rate path adds a ceiling on USD. Treasury yields extended higher, Stocks under pressure as data add to the impacts from Friday’s jobs report to reinforce the FOMC’s view that it will have to maintain a more restrictive policy stance for some time.

*The curve inversion deepened to -80 bps, not seen since 1981.The belly of the curve continues to lead the weakness in Treasuries with the 3-year yield up 15 bps to 4.129%. The 10-year is 11.7 bps higher at 3.603%.

*AUD – ranging at 0.6720-0.6735 following 25 bps hike from RBA and a prediction of further hikes ahead.

*EUR – pullback to 1.0484 from 1.0590 yesterday. German manufacturing orders stronger than expected but failed to boost EUR.

J*PY – jumped to 137.30.

*GBP – dip to 1.2160 from 1.2345.

*Stocks – US100 closed with a -1.93% decline, with the US500 off -1.79% and the US30 -1.40% in the red. The declines saw the US500 drop back below 4,000, with the US30 under 34,000.

*USOil – The January WTI crude slipped -3.8% to $76.93 on concerns Fed tightening will weaken demand. There was little impact as the EU price cap went into effect.

*Gold – reverts to $1770 from $1809 highs, as the USD backed up from early lows amid US data releases. Bullion failed to close above $1800.

Today – US Goods & Services Trade Balance and Canadian Ivey PMI.

Biggest FX Mover @ (07:30 GMT) AUDJPY (+0.69%) turned above 200-DMA. MAs flattened indicating the end of the uptrend, MACD signal line is at 0, RSI 62.00 & falling, H1 ATR 0.178, Daily ATR 0.998.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

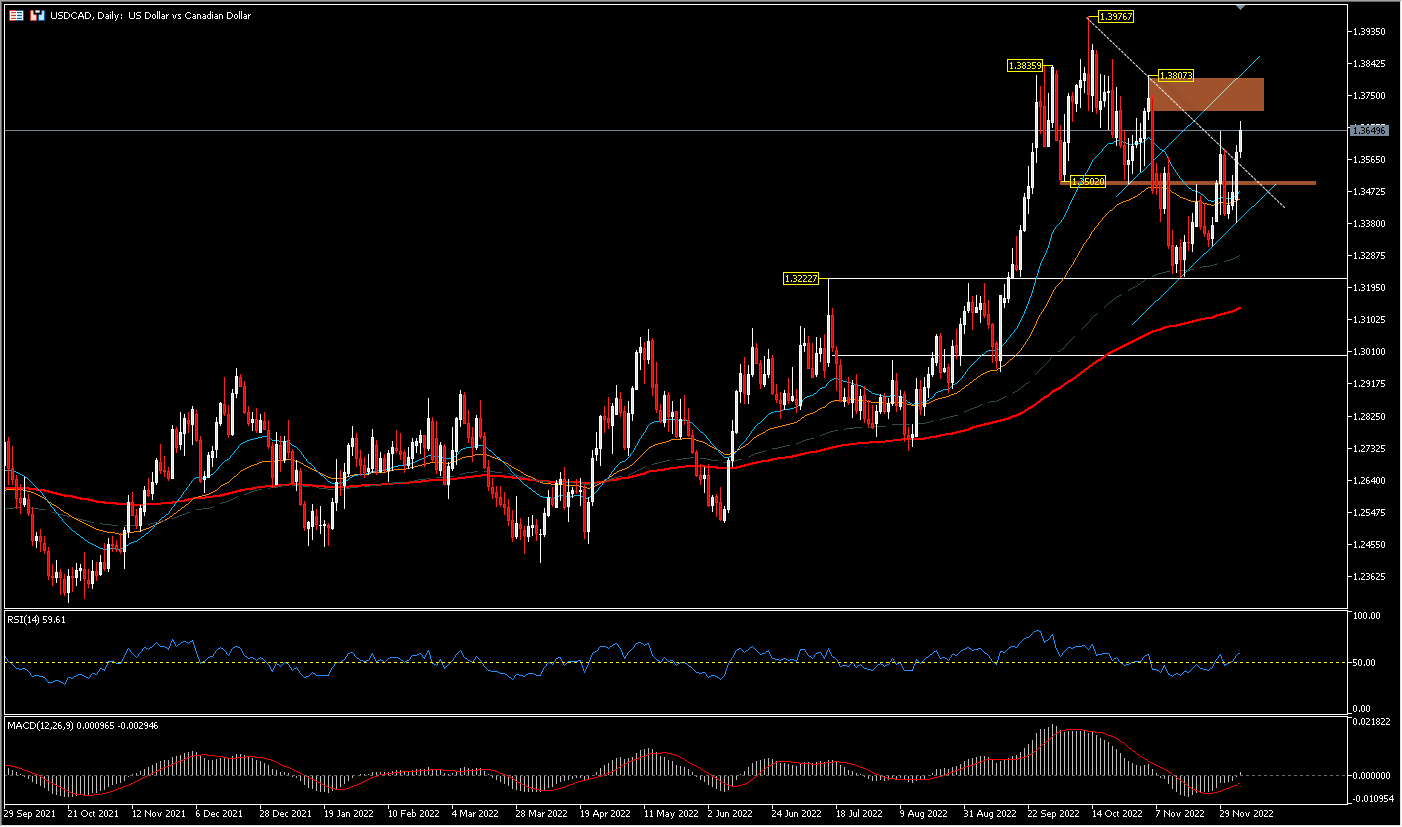

Oil Drops Hit the Loonie, Ahead of BOC Interest Rates!

USDCAD,D1

The USDCAD exchange rate strengthened after a relatively hawkish Fed, which is likely to push interest rates above 5% in 2023, following a series of strong economic data from the US. On Friday, data showed that the US economy added more than 263K jobs in November, while the unemployment rate remained unchanged at 3.7%. Wages jumped 5.2% even as tech companies lost thousands of jobs. And on Monday, data showed that the non-manufacturing PMI spiked in November.

The BOC will hold its 8th and final rate setting meeting for 2022 today (December 7), a week before the Fed and ECB meetings on December 14 and 15 respectively. The rate decision will be announced at 15:00 GMT with a press conference by Governor Macklem at 16:00 GMT. This will be the biggest catalyst for the movement of USDCAD. The market predicts that the central bank will raise interest rates by 0.50% to 4.25%. This decision was taken at a time when Canadian inflation was still high. According to Statcan, the country’s annual inflation rose to 6.9% in October due to rising gasoline and mortgage prices.

Crucially, the BOC’s decision comes at a time when Canada’s yield curve has fallen to its lowest level since the 1980s. The spread between 10 and 2 year bonds rose to 100 basis points, signaling that the economy was headed for a major recession. Hence, the BOC is likely to deliver a dovish rate hike. Since the October meeting, data releases have been on the positive side. GDP growth surprisingly reversed in Q3 with an annualized rate of 2.9% q/q, while the latest inflation figures show signs of stabilizing at what could be called a very high level. Meanwhile, labor market data came in stronger than anticipated for October, but retail sales for September painted a bleaker picture.

Technical Analysis

The recent weakening of the Canadian Dollar has been distorted by the decline in world crude oil prices. Currently, USDCAD is trading at 1.3655, strengthening by 1.5% this week. The price is above the 26-day exponential moving average and is trying to catch up to the price on the resistance’s right shoulder at 1.3807. The RSI is above the 50 level, the MACD histogram is just shy of crossing the zero line. On the downside, the neckline of the head and shoulder pattern will still function as minor support at 1.3502.

USDCAD, H8

Intraday bias remains neutral, while with immediate focus on the 1.3807 resistance, a strong break there would confirm the case that correction from 1.3976 has been completed at 1.3225. Further gains should be seen to the head of 1.3976. On the downside, a follow-through break of 1.3225 could see a second attempt to reverse the trend towards the 1.3000 round figure. The RSI at 66 is of course not saturated yet while MACD is still in the buy zone, trying to thwart the head and shoulder pattern that has been formed. Further movement will be influenced by the BOC interest rate decision as well as statements from Bank officials.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

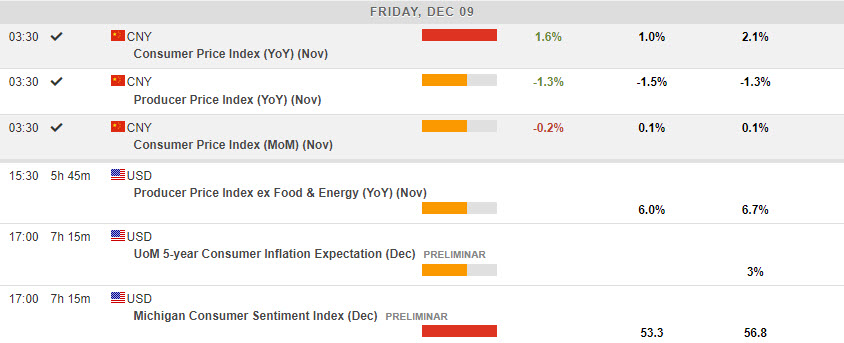

Market Update – December 9 – Stocks Recover, USD Weaker, PPI Data Ahead.

Trading Leveraged Products is risky

*The USD Index is down at 104.55 for a 3rd day in a row. Wall Street rebounded with the US500 +0.75% (3963) gain breaking a string of five straight losses. Treasury yields rose slightly following the deceleration in unit labour costs & rise in jobless claims. However, the 2/10yr yields are still shouting Recession – the curve remains -83bps. China confirms weak activity once again (Nov. CPI -0.2% m/m from 0.1% m/m). UK regulators fine Santander £107mn for anti-money laundering failures

*The US is set to levy fresh sanctions against Russia and China.

*EUR – retests 1.0600 amid USD weakness and trades at 1.0575 now.

*JPY – slight pull back over 136.00, to 136.30 from 135.80 lows.

*GBP – holds over 1.2200, and trades at 1.2260. Monday’s high touched 1.2345. The UK Chancellor Hunt is to announce plans to relax regulation for UK’s financial services sector, rolling back 2008 rules.

*Stocks – Dip buying and short covering helped the rally and sentiment along with signs China is moving further to ease covid restrictions. JPN225 surged 1.2% and Hang Seng index rose by 1.6% as China’s Premier stated that the shift in COVID policy would allow the economy to pick up pace. The US100 climbed 1.13% and the US30 was up 0.55%, while the rise in jobless claims yesterday (230k) helped limit the selloff, though rates were still cheaper at the end of the session.

*The US Federal Trade Commission blocks the biggest ever gaming industry deal. FTC sued Microsoft Corp MSFT +1.24% to block its planned $75 billion acquisition of Activision Blizzard Inc ATVI -1.54%

*USOil – holds at 1-year lows, below $72.00 at $71.70. USOil found some slight support (a rally to $75.00) after news that the Keystone pipeline in the US was shut down after more than 14,000 barrels of crude oil spilled into a creek in Kansas.

*Gold – extends to $1795 – 4th bullish day away from 200-day SMA.

Today – Caution prevails ahead of today’s PPI and consumer sentiment data, and next week’s CPI, and then the FOMC on Wednesday.

The recent weakening of the Canadian Dollar has been distorted by the decline in world crude oil prices. Currently, USDCAD is trading at 1.3655, strengthening by 1.5% this week. The price is above the 26-day exponential moving average and is trying to catch up to the price on the resistance’s right shoulder at 1.3807. The RSI is above the 50 level, the MACD histogram is just shy of crossing the zero line. On the downside, the neckline of the head and shoulder pattern will still function as minor support at 1.3502.

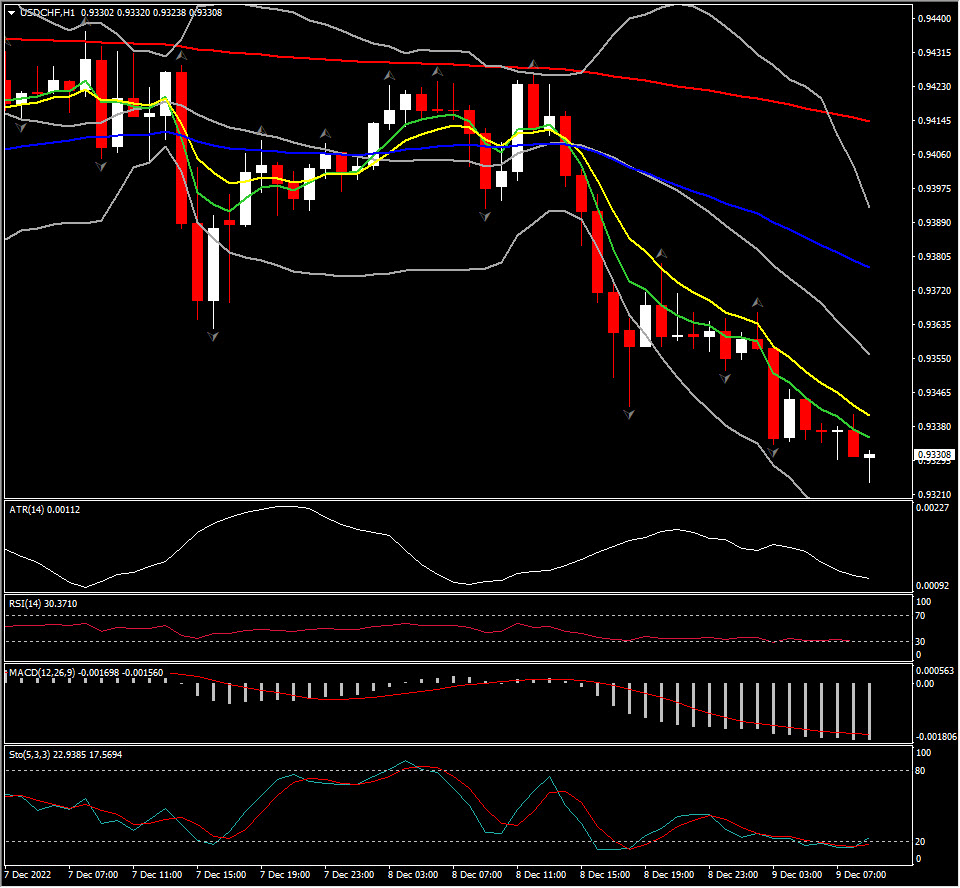

Biggest FX Mover @ (07:30 GMT) USDCHF (-0.41%). MAs aligned lower indicating the continuation of the downtrend, MACD lines are negatively configured, RSI 31 but flat, H1 ATR 0.00113, Daily ATR 0.00872.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 12 – USD lifts, Stocks Slip Ahead of a Key Week.

Trading Leveraged Products is risky

*The USD Index holds at 105.00 from lows on Friday at 104.50, following hot PPI data and strong consumer sentiment. Stocks fell into close on Friday (Dow the weakest -0.9%) and down 2.85-4.0% last week (Nasdaq weakest) threatening the Santa Rally. Yields rallied over 2% on Friday, 10yr closed at 3.567% trades at 3.55% today. Asian markets & European FUTS are also lower as Chinese Covid infections rise as restrictions are eased. BIG week ahead.

Week Ahead – US CPI and the FOMC dominate matters but 10 other Central Banks update markets this week including ECB and BOE. 50 bp hike from the FED now at 77% from Fed Funds Futures, following Friday’s data.

*EUR – tested the 1.0600 zone on Friday – trades down at 1.0530 now.

*JPY – rallied from post PPI low at 135.60 on Friday to test 137.00 again today.

*GBP – Sterling rallied again to breach 1.2300, briefly and post 5-month highs on Friday. Trades at 1.2228 now.

*Stocks – Wall Street dived on Friday – US500 -29.13 (-0.73%) 3934, Big movers included LULU -12.85%, COIN -6.00%, & TSLA +3.23%, NFLX +3.14%. FUTS trades at 3933 now too.

*USOil – Slipped to new 12-month+ lows at $70.05 on Friday on a weak global outlook, trades at $71.40 now.

*Gold – Rallied to and broke the key $1800 again, but could not hold it. Trades at $1788 support now.

*BTC – Sentiment woes continue, rallied to $17.3k on Friday but trades below 17k today at 16.9K

Today – UK GDP (m/m) beats (0.5% vs. 0.4%) & better Production data. UK NIESR – Speech from BOC’s Macklem.

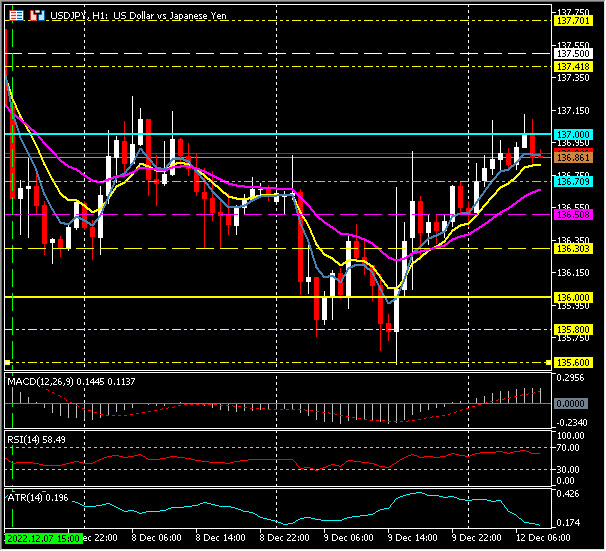

Biggest FX Mover @ (07:30 GMT) USDJPY (+0.47%) rallied from post PPI low at 135.60 on Friday to test 137.00 again today. MAs aligning higher, MACD histogram & signal line positive but falling, RSI 58.50 & rising, H1 ATR 0.196, Daily ATR 1.783.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 13 – Markets Await US CPI.

Trading Leveraged Products is risky

*The USD Index holds under 105.00, currently at 104.80 as the USD consolidates ahead of today’s CPI data. US Stocks rallied on Monday (Dow the strongest +1.58%). Yields rallied over 1.23% with the 10yr closing at and holds today at 3.611%. Asian markets mixed & European FUTS are also lower as Chinese Covid infections continue to rise. Former FTX CEO Bankman-Fried has been in the Bahamas at the “behest of U.S. prosecutors” a day before he was due to testify to Congress. Reuters also reported that Binance is under investigation for possible money laundering and criminal sanctions violations by DOJ, with possible proceedings against executives including CEO Zhao.

*EUR – rotates over 1.0500 at 1.0560 now, ahead of German ZEW data later and ECB on Thursday.

*JPY – rallied from 136.50 lows over 137.00 and trades at 137.70 today.

*GBP – Sterling rallied again to test 1.2300, consistently yesterday, but trades at 1.2285 following mixed UK jobs data and as multiple strikes hit the UK.

*Stocks – Wall Street rallied yesterday (1.26-1.58%) – US500 +56.18 (+1.43%) 3990, Big movers included MRNA -6.89%, TSLA -6.27%, MSFT +2.89%. FUTS trades at 3997 now.

*USOil – SRallied over 6% from 12-month+ lows at $70.05 again on Monday to trade at $74.30 now on supply concerns.

*Gold – Declined to $1780 again, from key support at $1788.

*BTC – Sentiment woes continue, but talk of “rapid rollout of global crypto standards” led by FSB keeps trades over 17k at 17.1k.

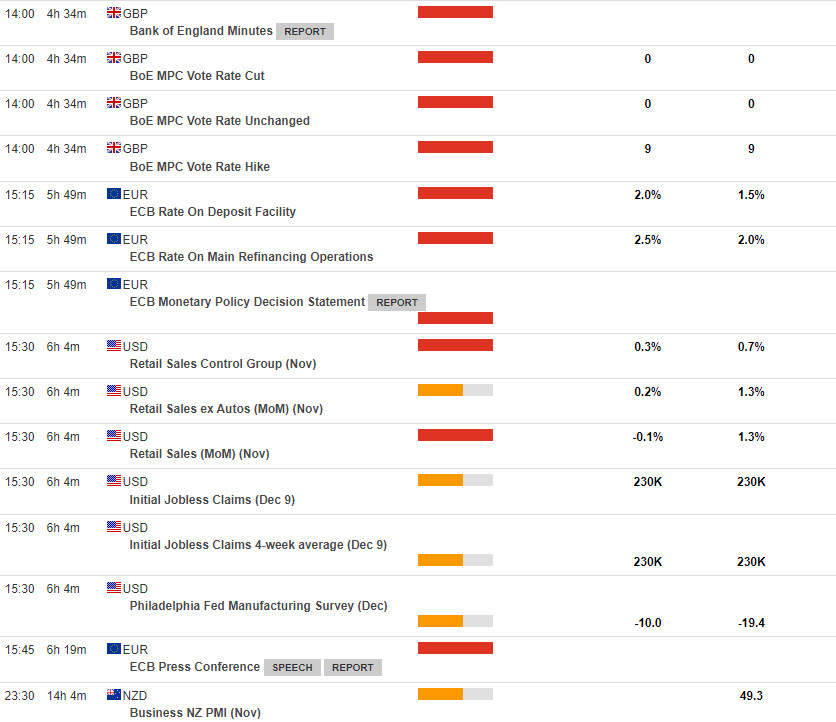

Today – UK Unemployment, German ZEW, US CPI, Japanese Tankan.

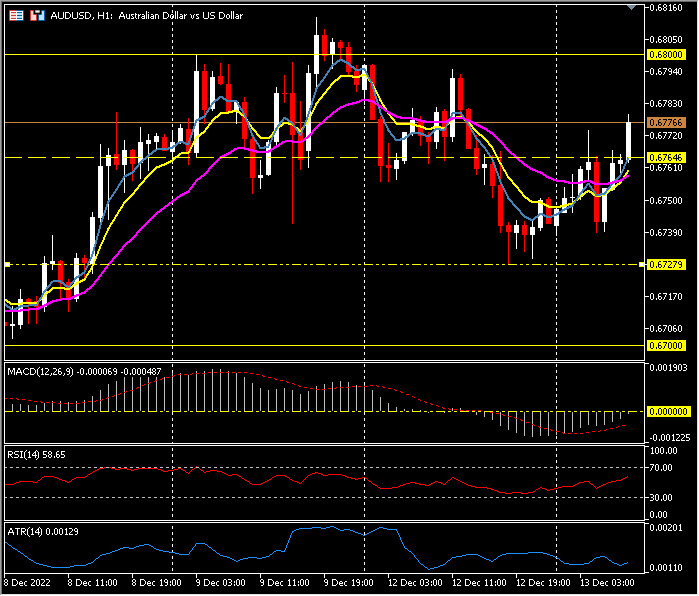

Biggest FX Mover @ (07:30 GMT) AUDUSD (+0.53%) rallied from lows on Monday at 0.6728 to test 0.6775 today. MAs aligning higher, MACD histogram & signal line negative but rising and testing 0 line. RSI 58.10 & rising, H1 ATR 0.00129, Daily ATR 0.00845.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 14 – FOMC Day after Inflation weakens again.

Trading Leveraged Products is risky

*The USD Index dived to a six-month low of 103.50, from 105.00 following the cooler CPI data and trades at 104.00 now. US Stocks rallied on open as high as +3.85% but lost most of their gains by close (+0.30-1.01%). Yields tanked (10-yr lost 11 bp) as Treasuries rallied but closed at 3.501%. Commodities rallied (Gold & Copper hit 6-mth highs and Asian markets remain bid and the USD down 1.5% vs Yen, and 6-mth lows vs Euro, Sterling & Kiwi and 3-mths lows vs. Aussie. BTC spiked to 18k before, news that Binance withdrawals had hit $1.9 bln in 24 hours.

UK CPI also weakens (10.7% vs 10.9% & 11.1% last month) more than expected but the wider RPI (which is what many wage settlements use and a cause of the wide spread strike action) dipped but was hotter than expected at 14%.

*EUR – rotates over 1.0600 at 1.0625 now, ahead of ECB on Thursday.

*JPY – sank to 134.60 lows from over 137.70 yesterday and 150.00 in late October. Strong Tankan data and Machinery Orders help JPY strength.

*GBP – Sterling rallied over 1.2400, and traes at 1.2350 following good Inflation data and ahead of an expected 50 bp rate hike from the BoE tomorrow.

*Stocks – Wall Street rallied closed higher again yesterday but gave up most of their opening gains. – US500 +29 (+0.73%) 4019, and retakes 4000. Big movers included MRNA +19.63%, META +4.74%, GooG & AMZN +2.5%. FUTS trades at 4029 now.

*USOil – Rallied to $76.00 and trades at the key $75.00 now after a surprise build in US crude inventories against forecasts of a decline.

*Gold – Spiked as high as $1824.45 and trades at $1808. Can the $1800 handle hold?

*BTC – Sentiment woes continue from Binance & SBF but the weaker USD saw a peak over $18k, before a crash to 17.3k and bounce to 17.7k now. More FTX collapse fallout – Canada bans crypto leverage, crypto margin trading.

Today – “nothing else matters” FOMC Policy Decision & Press Conference. Before that – EZ Ind. Prod., US Export/Import Prices, NZD GDP. Speech from ECB’s Elderson.

Biggest FX Mover @ (07:30 GMT) NZDJPY (-0.37%) fell from highs over 88.00 yesterday to test the 87.00 tzone today. MAs aligned lower, MACD histogram & signal line negative and falling. RSI 38.10 & falling, H1 ATR 0.163, Daily ATR 0.879.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 15 – FED: Inflation Remains Public Enemy No. 1.

Trading Leveraged Products is risky

The FED, as expected, announced a 50 bp increase in the federal funds rate to place it in a target range of 4.25%-4.50% (the highest level in 15 years – since 2007). Powell pointed out that “We have more work to do” and that “there is a long way to go” expecting “continued increases”. The first is expected to be 25bp in February, which “will depend on incoming data” and from there the pace will be set taking into account “the cumulative tightening of monetary policy”. 17 of 19 members expect the terminal rate to be over 5.1% during 2023, and “there are no rate cuts in the projections for 2023” and that there will not be until the Fed “has full confidence that inflation is continually falling to the target” , for which it will have to“maintain restrictive rates for a sustained period of time”.

The higher for longer mantra continues – its not the rate of increase but how long it remains elevated. Sounded Hawkish but markets not convinced.

*The USD Index gyrated on the FED announcement moving north of 104.00 but dipped to new 6-mth lows at 103.33 before recovering to 103.85 now. US Stocks rallied on open again but fell post FED and by close were lower (-0.42-0.76%). Yields held at lows too as Treasuries held on to Tuesday’s gains, 10yr closed at 3.503%. Commodities were mixed (Gold under $1800 but USOil holds over $76.50, from $77.50). Asian stocks are mostly lower in the aftermath of the FOMC and disappointing Chinese activity data.

*EUR – rotates 50 bps higher over 1.0600 at 1.0650 now, ahead of ECB later today.

*JPY – sank to 134.50 lows, ahead of the FED, spiked to 136.00 then dipped to 134.80 as Powell spoke and is back to 135.80 now. – Weak JPY (Trade) & Chinese (Ind. Production & Retail Sales) data and strong AUD jobs numbers.

*GBP – Sterling rotated a whole big number from 1.2445 to 1.2345 and trades at 1.2388 ahead of an expected 50 bp rate hike from the BoE today.

*Stocks – Wall Street rallied but then closed lower – US500 -24.33 (-0.61%) 3995, and slips below 4000 again. Big movers included TSLA -2.58%, COIN -3.88%, AMD -3.80%. FUTS trades at 4012 now.

*USOil – Rallied to $77.54, post FED having touched $75.50 following huge inventory gains of 10.2 million barrels, trades at the key $76.50 now.

*Gold – Spiked down to $1795, rallied to $1815 and trades at $1788 now, unable to hold the $1800 handle.

*BTC – Sentiment woes continue from Binance & SBF but the weaker USD saw a peak over $18.3k, before a crash to $17.7k now. – FTX bankruptcy lawyers say they -“do not trust” – Bahamas government.

Today – US Weekly Claims, Retail Sales & Industrial Production, BoE, ECB, Norges Bank, SNB & Banxico Policy Announcements, European Council Meeting, Press Conferences with ECB’s Lagarde, Norges Bank’s Bache & SNB’s Jordan.

Biggest FX Mover@ (07:30 GMT) AUDUSD (-0.59%) fell from highs over 0.6885 yesterday to test 0.6825 today. MAs aligned lower, MACD histogram & signal line negative and falling. RSI 39.22 & falling, H1 ATR 0.00183, Daily ATR 0.00935.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 16 – Ms Lagarde the Most Hawkish of All.

Trading Leveraged Products is risky

Following the FED’s hawkishness on Wednesday, the ECB took it a step further. The central bank may have slowed down the pace of tightening moves, but the statement made very clear that this is not a sign that rates are anywhere close to the peak and that there will have to be further “significant” tightening to bring rates to restrictive level, in order to dampen demand and thus help to bring inflation down. “This is not a pivot, we are in it for the long game”. EUR rallied & Yields on short term credit erupted (2yr German yields moved 24.2bp – the most in a single day since 2008) and the DAX lost –3.28%. 7 other central banks (including BOE) also rose rates yesterday all commenting on the scourge of inflation. A big Risk-Off day. The AUD tanked 2.4%, the Yen lost 1.7%, Gold was down 1.7% and USOil was off 1.8%.

*The USD Index rallied from 104.80 blows to retake the key 105.00 band trades at 105.30 now. US Stocks tanked (-2.25%-3.2%) Yields held at lows too as Treasuries held on to gains, 10yr closed at 3.47% and are lower no at 3.45%. Asian stocks are also lower in the aftermath of CB week (Nikkei -1.87%) and more grim Chinese covid narratives…”Beijing death toll mounts as Covid sweeps through Chinese capital”, “Beijing urged to roll out Covid boosters to avoid 1mn deaths”.

*EUR – rotates over 1.0600 at 1.0650 now, having spiked to 1.0720 post ECB.

*JPY – rallied from 135.25 lows, to spike over 138.00 and now trades at 137.30. This week’s low was 134.50.

*GBP – Sterling collapsed from 1.2425 to 1.2150 as the BOE vote was split with 6 members agreeing on the 50bp hike and one voter wanting to go with 75bp, however 2 voted and will have argued strongly for no change. Markets hate uncertainty, but conversely, they also hate “group think”. The FTSE100 also closed -0.93%. UK Retail Sales today missed significantly (-0.4% decline vs a 0.3% gain).

*Stocks – Wall Street collapsed (NASDAQ worst performer -3.2%) – US500 -99.57 (-2.5%) 3895, and slips below the key pivot at 3900 again. Big movers included the biggest of all APPL -4.69%, META -4.47%, NVAX -34.30%. FUTS trades at 3895 now.

However poor the prospects of a Santa Rally may appear, history is still on its side.

*USOil – Rallied to $77.54, again before falling to $75.25 and trades at $75.70 now.

*[/bGold – Collapsed into the key $1780 and cannot hold that level today, trading at $1775.

*[/bBTC – Sentiment woes continue the biggest coin trades at $17.4k today.

Today – EZ, UK & US Flash PMIs, EZ HICP (Final), Quadruple Witching.

Biggest FX Mover@ (07:30 GMT) AUDJPY (-0.40%) muted moves in FX following yesterday’s huge moves. Fell from highs on Tuesday at 93.35 to test 91.80 today. MAs aligned lower, MACD histogram & signal line negative and falling. RSI 35.45 & falling, H1 ATR 0.177, Daily ATR 0.935.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 19 – Covid outweighs Reopening.

Trading Leveraged Products is risky

*The USD Index is hovering around 104.00 bottom, despite the renewed rise in the Treasury yield. Global stock markets made a wobbly start to the final full trading week of 2022, with the prospect of interest rates rising further next year taking the edge off festive cheer, and with concerns over China Covid Outbreak. Asian yields dipped, while US Yields also held at lows as Treasuries continued to rise, 10yr is up 3.1 bp at 3.51%. Asian stocks have remained under pressure, with concern over China’s Covid count also weighing.

*China officially reported its first coronavirus-related deaths since the unwinding of some of the strictest pandemic control measures earlier this month.

Chinese authorities have warned of three successive waves of Covid infections over the coming months, as cases continue to surge after the lifting of restrictions earlier this month. Only 42.3% for people aged 80 and above got the booster.

*EUR – up at 1.0640 now & GBP stuck at 1.2160-1.22 area.

*JPY – extends lower to 135.80, with Yen be the biggest gainer of the day as speculation building that the Bank of Japan, which meets on Monday and Tuesday, is eying a shift in its ultra-dovish stance in future.

*Elon Musk asked Twitter users to vote Sunday on whether he should step down as head of the social-media platform and pledged to abide by the results. Plus Twitter said it would no longer allow “free promotion of certain social media platforms” like Meta Platforms Inc’s META.O Facebook and Instagram, Mastodon etc. on its sites.

*Stocks – The JPN225 declined more than -1%. Hang Seng and CSI 300 are down -0.9% and -1.5% respectively. US500 dropped 2% last week (-20% for the year) while today US & European indixes are managing slight gains, US500 rose 0.1%.

*USOil – drifts to $74.65

*Gold – was steady at $1,793

*BTC – remained trading below $17,000.

Today – There is a heavy calendar ahead as releases are condensed ahead of Christmas on Sunday. Housing reports will highlight as that has been one of the sectors most impacted by the Fed’s tightening. China is expected to deliver a key interest rate decision on Tuesday morning, after keeping the rate steady for three straight months. Japan as well.

Today – Germany Dec .Ifo survey, Eurozone Q3 labour market!

Biggest FX Mover@ (07:30 GMT) USDJPY (-0.59%). MAs aligned lower, MACD histogram & signal line negative and falling. RSI 37 & falling, H1 ATR 0.33, Daily ATR 1.93.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – December 20 – Pre-Christmas Surprise from BOJ.

Trading Leveraged Products is risky

*The USD Index is betwixt and between amid various drivers. It closed at 104.706, inside the day’s 104.931 to 103.50 range. The advent of the holidays and year end have lightened volume measurably too, exacerbating some of the moves in the markets. Stocks are in red against Decembers’ seasonality. Treasuries fell today, especially at longer tenors, after the Bank of Japan unexpectedly lifted a cap on 10-year yields and unleashed a sell-off across global bond markets.

*Yields: 10yr rose to 3.71% and 30-yr to 3.72%.

*The S&P 500 has risen in 73% of December since 1928, according to Dow Jones Market Data. As of Monday’s close, the S&P 500 had fallen 6.4% in December.

*EUR – tumbling between 1.0575-1.0650.

*JPY – surged to 132.66 after the BOJ said it would review its yield curve control policy and widened the trading band for the 10-year government bond yield in an unexpected tweak. (Policy is unchanged)

*AUD & NZD drifted also after BOJ announcement.

*Stocks – The NASDAQ tumbled -1.49%, with the S&P 500 falling -0.90%, while the Dow slid -0.49%. Nikkei closed with a -2.5% loss.

*SUSOil – drifts to $75.20 from $76.55.

*SGold – higher but still struggling to break the $1,800.

*SBTC – retested again the $16,200 floor. – Sam Bankman-Fried to agree to US extradition after Bahamas court hearing.

Today – US Housing Starts & Building Permits, Canadian Retail Sales, EU Consumer Confidence and NZ Trade data.

Biggest FX Mover@ (07:30 GMT) AUDJPY (-3.32%). Broke 8-month support extending to 88.30, below 50-week EMA. Intraday MAs keep pointing lower, MACD histogram & signal line negative and falling. RSI 22 & flat, H1 ATR 0.4920, Daily ATR 1.1611.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*The USD Index stuck at 103.50 bottom. Stocks pick up overnight, after were pummeled Tuesday by the BoJ’s surprise hawkish tweak in its yield curve control. Yields: JGB 2-year rose above zero for the first time since 2015. 10-year Treasury yield cheapened 11 bps to hit 3.706%. The curve inversion unwound another 10 bps on the day to -57.9 bps and compares to the -84 bps two weeks ago.

*EUR -jumps 20 pips at the EU open higher to 1.0630. German GfK consumer confidence improved to -37.8, a tad better than anticipated. All in all a number that ties in with expectations for a shallow and short lived recession, rather than a protracted slowdown.

*JPY – trimmed -4% to 130.55. – Higher yields at home could make it more attractive for Japanese investors to repatriate some funds.

*Stocks – Nikkei lost a further -0.7% after the BoJ’s curve ball yesterday. The ASX bounced 1.3%, and China bourses are also higher – as are stock futures across Europe and the US. The NASDAQ flat at 33,230, with the S&P 500 at 3,868, & the Dow up by 0.25%. #TSLA collapse continues -8% yesterday.

*USOil – flat at $75, with Brent trading at $80.01 per barrel.

*Gold – higher held at $1,815.

Today – Canadian Inflation & US Consumer Confidence. Ukrainian President Volodymyr Zelenskiy is expected to travel to Washington to meet President Joe Biden.

Biggest FX Mover@ (07:30 GMT) NZDUSD (-0.67%). Turned below 20-DMA. Intraday MAs flattened, MACD histogram & signal line negative and falling. RSI 40 & rising indicating a possible recovery or steadiness, H1 ATR 0.00151, Daily ATR 0.0084.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – January 2 – Markets drift on weak Chinese data & IMF Outlook.

Trading Leveraged Products is risky

With markets in Europe and North America closed today and only a few Asian markets open there was little direction on very limited volume. Weak PMI and Housing data from China on Saturday and a poor global outlook from the IMF yesterday start the New Year in the same down-beat way 2022 concluded. The Yen is the biggest gainer today.

China’s official Services PMI cratered -5.1 points to 41.6 in December after falling -2.0 ticks to 48.7 in November. This is a sixth consecutive monthly decline, a third straight month in contraction, and the lowest level since February 2020. It was at 52.7 a year ago. The December manufacturing index slid -1 point to 47.0 after falling -1.2 points to 48.0 previously. It too is a third month below the 50 expansion-contraction mark, and is the eighth month in 2022 below 50. It is also the weakest since February 2020s 35.7.

2023 is going to be a tough year as the main engines of global growth – the United States, Europe and China – all experience weakening activity. – IMF “tougher than the year we leave behind…China’s chaotic reopening is proving problematic”.

*The USD Index down at 103.00 levels, but in 2022 the USD was King once again.

*EUR – rotates back to 1.0700 levels today but tested 1.1500 highs and 0.9530 lows in 2022.

*JPY – the strongest today and trades at 131.00 and 10-day lows, 2022 saw a breach of 150.00 form 113.00 lows.

*GBP – Sterling traded over 1.4200 and under 1.0400 in a volatile (3 x Prime Minister, 5 x Finance Minister) 2022 for the UK. Today Cable holds over the key 1.2000 level at 1.2060.

*Stocks – Wall Street collapsed during 2022 into Bear market territory once more (NASDAQ -33.10%) and the US500 lost over 900 points (-19.44%) its worst year since 2008. The MSCI Global equity index lost 18.7%.

*USOil – Trades over $80.00, to start 2023. Russia’s invasion of Ukraine caused a spike to over $123.00 in February before falling to test $70.00 in December on weak global demand expectations.

*Gold – Trades at $1830 levels today. Rising Inflation and interest rates in 2022 had a rather muted impact on the precious metal. The war-inspired February spike to $2070 was followed during the rest of the year to October lows under $1620, before recovering $1800 in December.

*BTC – Sentiment woes continue. The biggest coin trades at $16,700 today after a tumultuous year which saw prices collapse from the $50,000 to the $15,000 level as the FTX saga broke.

Today – No Economic data due.

Biggest FX Mover@ (07:30 GMT) NZDJPY (-0.40%) muted moves in low volume FX markets. Continues to decline from last week’s rejection of 85.00, trades at 82.85 now, resistance at 83.00 and support at 82.50. MAs aligned lower, MACD histogram & signal line negative and falling. RSI 38.33 & falling, H1 ATR 0.173, Daily ATR 0.935.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – January 3 – JPY & Gold add to gains.

Trading Leveraged Products is risky

Markets are back to full-time today to kick-start 2023 with a key week topped by NFP data on Friday and undermined by the ongoing rise in Covid cases and deaths in China. Japan and New Zealand remain closed today, but in Asia the ASX (-1.3%) is the laggard whilst Chinese bourses are on a firmer footing (Shanghai Comp +0.8%, Hang Seng +2.1%), despite weaker manufacturing PMI data from Caixin (49.0 vs 49.4). In FX markets JPY is the notable gainer across the majors (USDJPY -0.77% @ 129.50 and 6-mth lows earlier) and the USD is receiving a bid as European markets get into full swing (EURUSD at 1.0570 from 1.0675).

*The USD Index remains capped by 103.50 today as the USD softens in early new year trading.

*EUR – rotates at 1.0570 now, having spiked to 1.0710 on Monday but unable to hold this key round number.

*JPY – moved lower again as the pivot from the BOJ becomes more baked-in to market thinking, the key 130.00 was breached earlier for the first time since June 2022.

*GBP – Sterling holds significantly over 1.2000 at 1.2070 in the first London trades of the year.

*Stocks – European and UK FUTS are higher and the US500.F trades at 3872 now, up from the 2022 close for the cash market at 3839.50.

*USOil – Rallied to breach and hold $80.00 yesterday and trades at $80.70 now.

*Gold – Has taken another leg higher today on USD weakness, continued CB rate hikes and subdued economic outlook. Breached $1830 in early trades and is testing the next resistance at $1850 now.

*BTC – Sentiment woes continue – the biggest coin trades at $16.7k today.

Today – German CPIs, Turkish CPI, UK & US final MFG PMI, US Construction Spending.

Biggest FX Mover[/b@ (07:30 GMT) EURJPY (-0.79%) into fourth consecutive day lower from 143.00 thighs last week to 138.30 today. MAs aligned lower, MACD histogram & signal line negative and falling. RSI 24.10 OS and still falling, H1 ATR 0.350, Daily ATR 1.823.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – January 4 – USD & JPY hold gains, Stocks flat & Oil tanks.

Trading Leveraged Products is risky

The first full day of 2023 saw stocks flat, a bid for the Greenback & Yen, weaker EUR following softer German CPI data and Oil markets collapse on global growth worries. Treasuries are firmer with US10yr yields losing -2.61%. Overnight Asian stocks have traded mostly firmer despite the negative handover from Wall Street; Hang Seng outperformed whilst Nikkei lagged (-1.45%). AUD outperforms. “China pledges ‘final victory’ over COVID as outbreak raises global alarm” – RTS lead story.

*The USD Index rallied to 104.50 yesterday as the USD got a significant New Year bid in early European trades on increased volumes. Softer at 104.10 now.

*EUR – tanked to test 1.0520 after the German CPI and USD bid, back to 1.0580 now.

JPY – hit new 7-mth lows under 130.00 at 129.50 on Tuesday before recovering to 131.40 highs today and trades at 130.40 now.

*GBP – Sterling sank to 1.1900 as USD rallied before recovering to the key 1.2000 today.

*Stocks – The US markets closed down (-0.40-0.76%). US500 -15.36 (-0.40%) at 3824 #TSLA -12.24% the worst performer. #APPL fell -3.74% and its market cap is now below $2 trillion level. XOM & CVX hit from a -4% collapse in Oil prices. US500.F trades at 3853 now.

*USOil – Tanked from $81.50 highs in early trades yesterday over 4% its biggest 1-day fall in over 3 mths on global demand concerns and China Covid cases. Trades at $76.45 now.

*Gold – Has taken another leg higher today on USD weakness, continued CB rate hikes and subdued economic outlook. Breached $1830 in early trades, is over the next resistance at $1850 and trades at $1858 now.

*BTC – Sentiment woes continue – the biggest coin trades at $16.8k today. Sam Bankman-Fried pleads not guilty in FTX fraud case; October trial set.

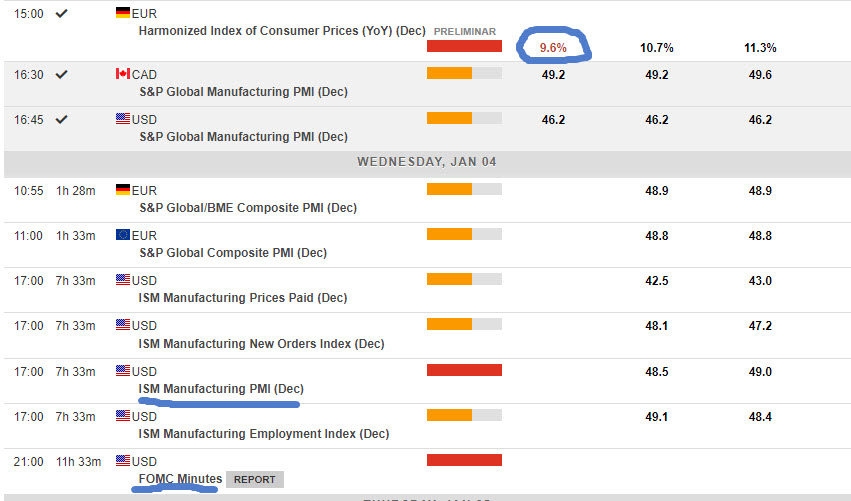

Today – German Import Prices, Swiss CPI, EZ Services and Composite Final PMIs, US ISM Manufacturing PMI, FOMC Minutes, Crude Private Inventories.

Biggest FX Mover@ (07:30 GMT) AUDUSD (+1.08%). A volatile day yesterday took the pair down to under 0.6700 and today its has tested all the way back to 0.6850. MAs aligned higher, MACD histogram & signal line positive and rising. RSI 72.30 OB and still rising, H1 ATR 0.00198, Daily ATR 0.0091.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – January 5 – FOMC: Inflation still Public Enemy No. 1.

Trading Leveraged Products is risky

The FOMC minutes continued to show inflation was the overriding concern. Participants generally noted that upside risks to the inflation outlook “remained a key factor” for policy. It was repeated that a restrictive stance would have to be maintained for a sustained period until inflation was “clearly” on a path toward 2%. US Data yesterday showed ISM Manufacturing PMI’s missing at 48.4, but Jobs Openings remaining very strong beating expectations at 10.46m. Kashkari called for 5.4% terminal rate.

*The USD Index held 104.00 yesterday as the USD steadied post FOMC mins. 104.20 now.

*EUR – back to test 1.0600. Germany November trade balance beats €10.8 billion vs €7.5 billion.

*JPY – rallied from new 7-mth lows under 130.00 yesterday to 132.50 now

*GBP – Sterling rallied to 1.2080 before sinking back to key 1.2000 today.

*Stocks – The US markets closed up (+0.40-0.76%). US500 -28.03 (0.75%) at 3853. TSLA +5.12%, BABA +13%, MSFT -4.37%.

*USOil – Tanked –9% Monday, Tuesday ($72.75 lows) and has recovered 1.1% today to trade at $73.50 ahead of inventories later

*Gold – Breached $1850 in early trades, rallied to $1860 and trades at $1850now.

*BTC – Sentiment woes continue – the biggest coin trades at $16.8k today. FTX’s former top lawyer aided US authorities in Bankman-Fried case.

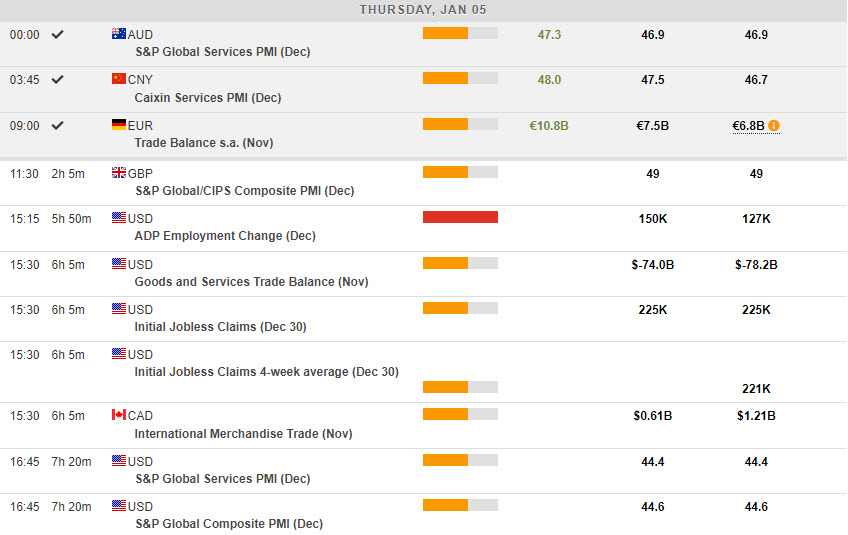

Today – EZ Construction PMI, UK and US Services and Composite Final PMIs, EZ PPI, US Challenger Layoffs, Canadian Trade Balance, US Claims, US EIA Inventories, speeches from Fed’s Bostic and Bullard.

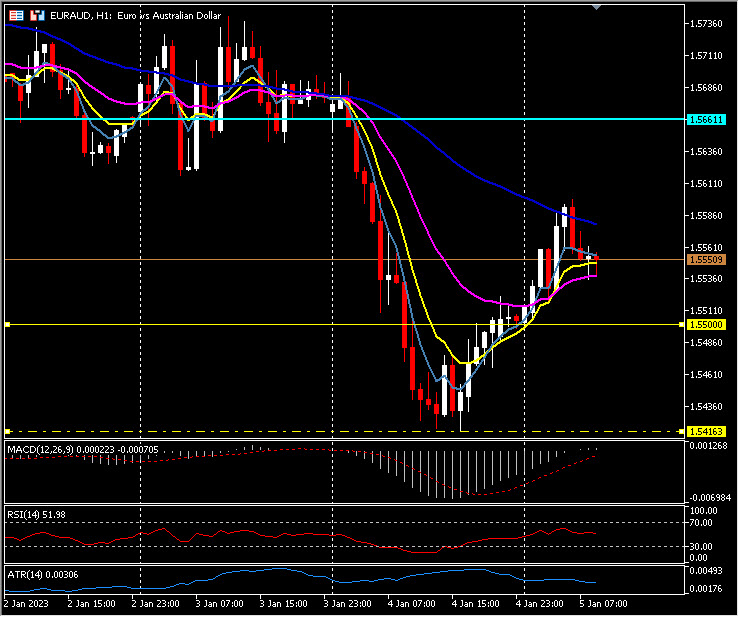

Biggest FX Mover@ (07:30 GMT) EURAUD (-0.45%). Declined from 1.5660 pivot yesterday to test 1.5400, before recovering and rallying to test 1.5600 today. MAs aligned higher, MACD histogram & signal line positive and rising. RSI 52.00 & neutral, H1 ATR 0.00306, Daily ATR 0.01388.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Новости

Новости Фотогалерея

Фотогалерея Клубы

Клубы Каталог

Каталог Оставить отзыв

Оставить отзыв Пользователи

Пользователи Объявления

Объявления Хостинг

Хостинг Технический анализ

Технический анализ Конкурсы фото

Конкурсы фото ПОЛНЫЙ СПИСОК

ПОЛНЫЙ СПИСОК Блоги

Блоги