Dollar pulls back off fresh 20-year highs as market prices in a more hawkish ECB.

Dollar Index

Monday’s London session proved to be a battleground won by the Dollar as it added to Friday’s gains, hitting levels last traded in September 2002. A Key driver in this exuberance is the ever-increasing probability of a 75-basis point rate hike as opposed to a 50-basis point rate hike at the next FED meeting in September. This in turn has caused yields to rise, with the 2-year yield hitting fresh 5-year highs near 3.5% and ultimately gave the dollar its appeal to continue its upward trajectory.

Technical Analysis: H4

In terms of market structure, last week saw the completion of the larger bullish continuation pattern in the form of the falling wedge type structure that found support from the 104.00 level and produced an impulsive wave that went on to revisit the 109.00 area last week Friday before setting a new high just under 109.50.

Intra-day Overview: Current price action in Monday’s trading session broke through the previous high and created fresh 20-year highs before retreating into the range finding support within the 108.00 range. Henceforth buyers could push the index to continue its bull run, or on the flipside, sellers could be well positioned at the fresh 20-year highs set in Monday morning’s London session and could challenge buy pressure.

Stocks At the time of writing, US Stocks have continued to sell off since Friday’s hawkish comments signalled a longer period of sustained higher interest rates.

*Dow Jones: Reacted by adding to the losses from last week by 0.07%.

*S&P 500: Pressure continued and added to losses from last week by 0.11%.

*Nasdaq: Was down on Monday by 0.49%.

Currencies

*Euro: Intraday overview: Price was buoyed by a pullback in the Dollar on Monday morning, which gave the Euro some impetus to claw back some of the losses made on Friday, retesting the upper end of the range at the 1.00291 area in the current bearish continuation structure.

*Pound: Intraday overview: The 1.16481 area was the floor that supported a pullback on Monday morning, as the Pound clawed back some of the losses from Friday. The Intraday high was set around the 1.17432 area.

Commodities

*Gold: Intraday overview: The $1 720 area was the floor that supported a pullback on Monday morning, helping Gold claw back some of the losses seen on Friday. The intraday high was set around $1 745.

*Oil: On the back of the Saudis’ comments around their inclination towards slowing down production, the price of Brent hit $100 and shows the possibility of geopolitical factors supporting the bullish momentum for now, while the current economic outlook, and central banks’ monetary policies, are supporting a bearish sentiment.

Bitcoin

In the wake of Bitcoin falling below the psychological $20 000 level, there could be more support around the corner as crypto adoption seems to be getting “a shot in the arm” with the Monetary Authority of Singapore considering implementing certain regulations around leverage when it comes to cryptocurrencies. This initiative is aimed to protect inexperienced consumers as opposed to banning the crypto market altogether.

Biggest FX Mover @ (06:30 GMT) NASDAQ (-3.9%). Dropped to 12387$ from 13206$.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – remains capped at 109.00 with support at 108.20 today. Tight JOLTS report adds to pressure for 75 bp next month; Fed Fund Futures now sit at 68.5%. 2yr yields traded to 15 yr highs. AUD outperformed overnight.

*EUR – German Inflation at near 50-yr highs, pressures ECB action and lifts EUR to 1.0033

*JPY holds between 139.00 & 138.00 having breached 138.00 Monday.

*GBP hit pandemic era lows (March 2020) yesterday at 1.1620. Recovered to 1.1675 now.

*Stocks US stocks weak again (S&P500 -44.00pts (-1.10%) 3986). Under 4k & 24-day low & under 50-day MA. Energy & Tech stocks led the decline. Futs. 4014 now.

*Oil lost over 5% yesterday but has recovered; API inventories better than expected. Touched $90.50 yesterday up to $92.50 now.

*Gold – crashed from resistance at $1736 and trades at support ($1724) now.

*BTC – tested Monday’s 33-day low ($19.5k) again yesterday, back over 20k now at 20.3k.

Overnight – Asian equity markets squeezed lower following weak Wall Street, European FUTS tick higher. NZD Strong Building Permits JPY Retail data also better than expected CNY PMI data beat but weaker than last month. Manufacturing (49.4) remains in contraction. German Import Prices and French CPI (m/m) weaker than expected. (1.4% & 0.4% respectively).

Today – German Import Prices & Unemployment, EZ CPI, Canadian GDP, US ADP & Chicago PMI, Speeches from Fed’s Mester & Bostic.

Biggest FX Mover @ (06:30 GMT) AUDUSD (+0.68%). Remains volatile, (100+ pip mover yesterday). Latest move; a rally from 0.6850 support to trade at 0.6900 resistance. MAs aligning higher, MACD histogram negative but signal line rising, RSI 56.00, H1 ATR 0.00128, Daily ATR 0.00823.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 1 – New Month Same Story – Dollar Bid.

Trading Leveraged Products is risky

*USDIndex – holds at 109.00 highs from a test of 108.50 support. Yields rallied again, Dollar on the frontfoot ahead of NFP & Labor Day Holiday, ADP (following revisions to calculation) big miss 132k vs 300k). Chengdu (120 million) in new lockdown.

*EUR – Record Inflation (9.1%) pressures ECB action (40% chance of 75bp rise next week) – EUR holds at 1.0018.

*JPY rallies again (new 24 yr highs) eyes key 140.00 & trades; 139.50 BOJ holding accommodative policy line.

*GBP new pandemic era lows under 1.1600 now, to 1.1568 lows.

*Stocks US stocks weak again (S&P500 -31.00pts (-0.78%) 3955). Energy & Tech stocks led the decline again as weak news from Nvidia, Tencent & AMD weighed. Futs. -1% at 3930 now.

*Oil down again on weake outlook, under $90.00 and trades at $88.90 now.

*Gold – also down and within $1.50 of $1700 earlier, trades at $1707 now.

*BTC – under 20k again today.

Overnight – CNY Manufacturing PMI data missed (49.5) and returns to contraction. German Retail Sales better than expected (1.9% vs. 0.0%).

Today – EZ, UK & US Manufacturing PMIs, German Retail Sales, Swiss CPI, EZ Unemployment, US ISM Manufacturing, Construction Spending, Speech from Fed’s Bostic.

Biggest FX Mover (06:30 GMT) EURCHF (-0.48%). Rejected 0.9830 today following 5-day rally from 0.9559, trades at 0.9786. MAs aligning higher, MACD histogram positive but signal line falling, RSI 43.00, H1 ATR 0.00132, Daily ATR 0.000723.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 2 – USD Holds at Highs, Stocks stem losses.

Trading Leveraged Products is risky

*USDIndex – spiked to 109.95 highs yesterday and holds the BID @109.50 now. A strong NFP could lift the USD even higher. A weak number could prick the USD bubble from 20-yr highs. Strong Weekly Claims and PMI’s added to USD demand. Fed Fund Futures now at 74%/26% for 75bp vs. 50 bp at next Fed meeting.

*EUR – ECB action expected next week, but EUR remains under Parity lows of 0.9910, trades at 0.9970 now.

*JPY rallies again (new 24 yr highs) broke 140.00 & holds at 140.30 BOJ holding accommodative policy line, & yield differentials driving trend.

*GBP new multi-year lows under 1.1500 yesterday, back to 1.1550 now. New PM next week.

*Stocks US stocks halted 4-day slide (S&P500 3966). Nvidia -7.67%, AMD -3% weighed again. Futs. flat at 3968 now.

*Oil down again on weak outlook, lows at $86.25 and trades at $88.20 now.

*Gold – also down under $1700 to $1688 lows, back to $1702 now.

*BTC – recovers 20k again today, from 19.5k lows yesterday.

Overnight – NZD Trade Balance missed (-2.4% vs 0.6%) German Trade Balance better than expected (see below).

Today – US NFP & Factory Orders, EZ Producer Prices.

Biggest FX Mover @ (06:30 GMT) EURNZD (+0.68%). Continued to recover from weekly lows at 1.6185 on Tuesday to 1.6450 today, next resistance 1.6485. MAs aligning higher, MACD histogram positive & signal line rising, RSI 63.62, H1 ATR 0.00238, Daily ATR 0.01615.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – holds at 110.25 highs. Yields plunged after NFP and as the curve bull steepened. Asian markets struggled after Wall Street closed in negative territory following news that Russia won’t be re-opening gas deliveries to Europe via Nord Stream 1 as scheduled.

*EUR – 20-year lows – tumbled back below parity, today’s low at 0.9876 as the standoff with Russia continues.

*JPY holds at 140 area.

*GBP fell to 1.1442, the weakest since March 1985.

*Stocks – US closed for Labour Day today. GER40 & UK100 are down -3% and -1% respectively this morning, with recession concerns deepening. ASX and Nikkei closed narrowly mixed. Major stock markets are posting 1-month declines from nearly -2% (TSX) to over -8% (NASDAQ).

*Oil got a boost from the jump in gas prices as traders look ahead to the OPEC+ meeting. USOIL is at $88.45 from $85.70.

*Gold – also down and within $1.50 of $1700 earlier, trades at $1707 now.

*BTC – 19.4K-20.5K.

Weekend – Gazprom announced on Friday that the main pipeline to Germany would remain closed indefinitely, against expectations of a restart on Saturday after three days of maintenance work.

Today - Today – All eyes will be on the monetary policy decisions from the ECB, BoC, RBA.Final readings for Eurozone and UK Services and Composite PMs are due today. In the UK the Conservative Party is set to announce that Liz Truss won the leadership contest and will succeed Boris Johnson as the next Prime Minister for the UK.

Biggest FX Mover @ (06:30 GMT) EURUSD(-0.48%) found a near term support at 0.9877. MAs aligning lower, MACD lines extend southwards, RSI 38, H1 ATR 0.00199, Daily ATR 0.00996.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 6 – Eyes on the deepening EU energy crisis.

Trading Leveraged Products is risky

*USDIndex – pulled back to 109.60 but still highlighting that the USD remains the haven asset of choice for now. Yields are on the rise again and stocks are struggling as the US returns from the holiday and markets keep a close eye on the deepening energy crisis in Europe and China’s Covid situation as the ECB meeting on Thursday comes into view. US 10-year rate at 3.24% 5.3 bp higher than on Friday.

*EUR – weaker than expected German orders numbers at the start of the session, only added to signs that Europe is heading for a recession but EUR trades at 0.9957 now.

*JPY remained under pressure and USDJPY lifted to 24-year highs at 141.20.

*GBP at 1.1587 after on Monday near its weakest level in decades in a sign of faltering investor sentiment in UK markets as Liz Truss prepares to take the reins as prime minister.

*AUD -RBA raised rates by 50 bp and signalled further rate hikes to come but noted that it is not on a pre-set path. AUDUSD is below 0.68 following a spike to 0.6832.

*Stocks – GER40 & UK100 futures are down -0.2% and -0.3% respectively. Asian markets traded narrowly mixed.

*Oil at $88.75. OPEC+ announced an output cut of 100K barrels per day and amid signs that a revival of Iran’s nuclear deal has run into difficulties.

*Gold – rose to $1726.80.

Overnight – RBA raised rates by 50 bp & weaker than expected German factory orders.

Today - UK Industrial and Manufacturing Production and Trade Balance, US ISM Services PMI.

Biggest FX Mover @ (06:30 GMT) GBPJPY(+1.14%). Spiked to 1-month peak at 163.80. MAs aligning higher, MACD histogram positive & signal line rising, RSI 83, H1 ATR 0.3130, Daily ATR 1.28.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 7 – King Dollar; Yen crushed.

Trading Leveraged Products is risky

*USDIndex – remains above 110 and the ongoing strength of the dollar, fueled by aggressive Fed hikes and the firm push back against inflation continues to weigh on stock markets, as traders assess recession risks amid Europe the escalating energy crisis in Europe.

*Bonds sold off hard with yields surging double digits and Wall Street stumbled amid renewed concerns over inflation, the FOMC’s hawkish response, and the concomitant threat to growth – amid a deluge of corporate debt offerings and as ISM services index increase to 56.9 further presser yields higher.

*20 companies slated bond offerings totaling an estimated $30 billion to $40 billion.

*EUR – break 0.9900 area than expected German orders numbers at the start of the session, only added to signs that Europe is heading for a recession but EUR trades at 0.9957 now. – German industrial production contracted – less than feared and at the same time the June number was revised up.

*JPY crushed! USDJPY at 144.35.

*GBP – 1.1490. Eyes to parliamentary testimony from the Bank of England governor.

*Stocks – Asian stocks fell to 2-year low on the back of disappointing Chinese trade number (China’s exports slowed in August). US100 fell -0.74% and the US30 and US500 slid -0.55% and -0.41%, respectively.

*Oil at $85.60

*Gold – extends for a 2nd day below $1700

Corporate bond update: there has been a flood of issuance to kick off September. It looks like corporations are jumping in while the going still looks relatively good and before rates go up further. Nestle plans a hefty 5-part sale with 3-, 5-, 7-, 10-, and 30-year coupons. Walmart announced a $5 bln 4-part deal to include a $1.75 bln 3-year, a $1 bln 5-year, a $1.25 bln 10-year and a $1 bln 30-year. Lowe’s plans a $4.75 bln 4-tranche deal with 3-, 10-, 30-, and 40-year tranches. MUFG has a $4.4 bln 4-parter including 3NC2 fixed and FRN, a 6NC5, and an 11NC10. John Deere Capital is selling $2.25 bln in 3-, 5-, and 10-year notes. There is a $2.3 bln 4-parter from Dollar General with 2-, 4-, 10-, and 30-year tranches. McDonald’s announced a $1.5 bln 10- and 30-year. Target has a $1 bln 10-year. ORIX has a $1 bln 2-oarter. And this is not even the full list. The explosion of offerings has added to the selling pressures on Treasuries. Rates are up double digits with the 10-year 15 bps cheaper at 3.34%.

Today - Attention will be on the BOC’s rate decision and BOE Monetary Policy Report Hearings along with BOE Governor Bailey testimony. Of importance will be remarks from VC Brainard, Michael Barr who will discuss financial systems. Barkin and Mester speak at an MIT event and the US trade deficit will also be important for what it says about global activity.

Biggest FX Mover @ (06:30 GMT) CHFJPY (+0.97%) at record highs, 146.48. MAs aligning higher, MACD histogram positive & signal line rising, RSI 83, H1 ATR 0.284, Daily ATR 1.116.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – spiked to 110.75, before slipping below 110.00 yesterday, but still holds the bid close to 20-year highs and trades at 109.50 now. Yields also slipped, but the curve remains inverted. Fed Fund Futures now at 79%/21% for 75bp vs. 50 bp September 21. Fedspeak Collins – inflation at 2% is the Fed’s “Job One,” Vice Chair Brainard said tight monetary policy will continue “for as long as it takes to get inflation down.”

*EUR – ECB action today and 75bp also in the frame. EUR rallied back to Parity yesterday and trades at 1.0093 now. EU plans a price cap on Russian gas prices – Putin warns of “winter freeze”.

*JPY rallies again (yet more new 24-year highs) tested to 145.00 & holds at 143.50. Japan MOF, FSA, and BOJ to hold meeting at 0745 GMT today.

*GBP new 37-year lows tested 1.1400 yesterday, back to 1.1515 now. New PM Truss set to announce £100bln emergency energy plan, via massive increase in government borrowing.

*Stocks US stocks rallied as Dollar & Yields cooled (S&P500 3979). Nasdaq best performer (+2.14%). TWTR +6.6%, TSLA +3.38%, Globalstar +21% (new satellite partner for APPLE’s new iPhone 14, Watch 8 Ultra and new AirPods (no news on new services). Share price unmoved after hours.

*USOil tanked (-5%+) on Russia/EU situation; and global outlook. Trades at $82.65 now from overnight lows at $81.40 now. Summer highs were north of $123.50.

*Gold – also rallied from lows under $1700 at $1691, to $1718.60 now.

*BTC – plunged to 18.5k lows yesterday and remains under 20k at 19.3k now.

Overnight & Today – US Weekly Claims, ECB Announcement, Speeches from ECB’s Lagarde, Fed’s Powell, Evans, Kashkari & BoC’s Rogers.

Biggest FX Mover @ (06:30 GMT) GBPCHF (-0.31%). Continues to decline, yesterday breaking under 1.1300 to 1.1220 lows which are being re-tested now. MAs aligning lower, MACD histogram negative & signal line neutral, RSI 39.90, H1 ATR 0.00137, Daily ATR 0.00814.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 9 – USD Sinks, Yen & BTC Rally.

Trading Leveraged Products is risky

*USDIndex – Slumps as YEN & EUR spike. A brief rally back to 110.00, faded following ECB’s hawkish 75bp hike and similarly Hawkish comments from both Lagarde and Powell. Trades at 108.90. Comments from Japanese officials lift the YEN and weak Chinese inflation data exposes demand weakness.

*EUR – ECB moved by 75bp and suggested more significant hikes to come. EUR rallied back to through Parity and trades at 1.0065 now.

*JPY having rejected 145.00, combined comments from Suzuki, Matsuno & Kuroda lifts the YEN and the pair trades at 142.90.

*GBP 1.1500 support held yesterday and a follow through move today takes Cable to 1.1600 resistance.

*Stocks US stocks moved higher again as Dollar & Yields cooled (S&P500 4006) FUTS trade at 4011. Asian stock markets have rallied, and European FUTS are little changed, the FTSE100 up 0.3%.

*USOil recovered from $81.40 lows to $83.50 now on chatter of more supply issues. 20-day moving average sits at $90.00.

*Gold – also rallied to $1725 and holds the key $1700 at $1721 now.

*BTC – rallied higher as the ETH merge (offering a 99.9% reduction in power consumption!!). Spiked from $18.5k on Wednesday to $20.6k now.

Overnight & Today – Canadian jobs report, EU energy meeting, Speeches from ECB’s Lagarde, Fed’s Evans, Waller & George.

Biggest FX Mover @ (06:30 GMT) AUDUSD (+1.31%). Continues to rally from a test of 0.6700 on Wednesday, trades at 0.6850 now. MAs aligning higher, MACD histogram negative & signal line positive & rising, RSI 79.22 & OB, H1 ATR 0.00142, Daily ATR 0.00850.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – Slips again as EUR and YEN see demand. Final FedSpeak remained Hawkish as news blackout starts. 88-90% chance of 75 bp hike up from 57% last week.

*EUR – ECB looking at 2% interest rates (currently 0.75%) to bring inflation to 2% target (currently 9.1%). 2024 exceptions 2.4% and 2% by 2025. Market expects 2-3 more rate hikes into December. Trades at 1.0100 now.

*JPY Govt spokesman (Kihara) – need to take steps to curb “excessive” Yen declines, stopped short of calling for BOJ intervention. However, USDJPY rallied from test of 142.00 Friday to 143.25 now.

*GBP Trades at 1.1643 despite miss for GDP earlier. London remains muted (politics suspended) but open ahead of Queen’s funeral next Monday (bank holiday).

*Stocks US stocks moved higher again as Dollar & Yields cooled (S&P500 4067) FUTS trade at 4076. Asian stock markets have rallied too, and European FUTS are higher pre-open.

*USOil topped at $87.50 on Friday on more chatter of supply issues. Trades at 86.30 now. 20-day moving average sits at $90.00.

*Gold – also rallied to $1728 and holds the key $1700 at $1720 now.

*BTC – rallied higher again, touching $22.2k earlier from $18.5k lows last week. Trades at 21.7k now.

Overnight & Today – UK Monthly GDP missed (0.25 vs 0.5%), ECB Survey of Analysts, Speeches from ECB’s Schnabel & de Guindos.

Biggest FX Mover @ (06:30 GMT) EURJPY (+1.01%). Continues to rally from a test of 142.75 on Friday, trades at 144.80 now. MAs aligning higher, MACD histogram & signal line positive & rising, RSI 72.56 & OB, H1 ATR 0.00142, Daily ATR 0.00850.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 13 – Cooler USD & Stocks Higher Ahead of CPI.

Trading Leveraged Products is risky

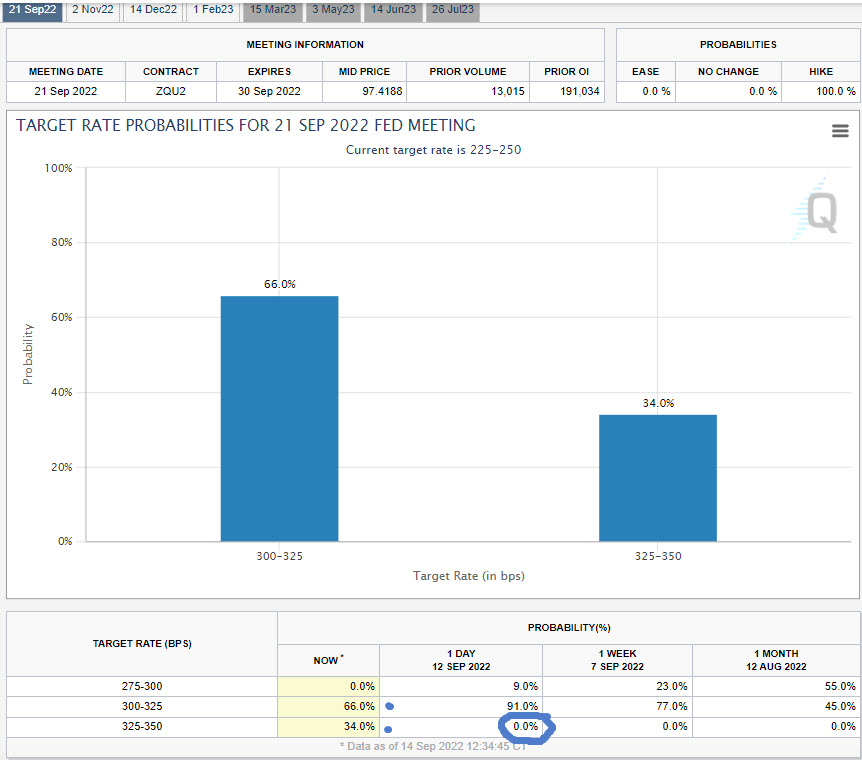

*USDIndex – Slips (108.00 tested) for a 5th straight day, lifting EUR & GBP. Fed Funds Futures back to 90% chance of 75 bp (third consecutive) hike. 10-yr Bond Auction was weak, only filled after it hit 3.33% (2.76% last time). “Higher for longer” mantra from Reuters Poll¹. Has Inflation peaked ?

*EUR – Trades at 1.0135 now from a test of 1.0200 yesterday.

*JPY markets not convinced BOJ intervention is imminent. Although Yen up today against others still weak vs. USD, touched 143.50 yesterday and holds 142.30 now.

*GBP traded over 1.1700 yesterday and holds 1.1723 now, following good jobs data. London remains muted (politics suspended) but open ahead of Queen’s funeral September 19 (Bank Holiday).

*Stocks US stocks moved higher again as Dollar & Yields cooled (S&P500 +1.06% 4110) FUTS trade at 4121. Nasdaq best performer (APPL +3.85%, PTON +7.18%). Asian stock markets have rallied too, and European FUTS are higher pre-open.

*USOil topped at $89.00 on Monday on more chatter of supply issues and possible easing of geopolitical tensions. Trades at $86.75 now. 20-day moving average sits at $89.00.

*Gold – also rallied to $1735 and holds over $1720 now.

*BTC – rallied higher too and holds at $22.3k.

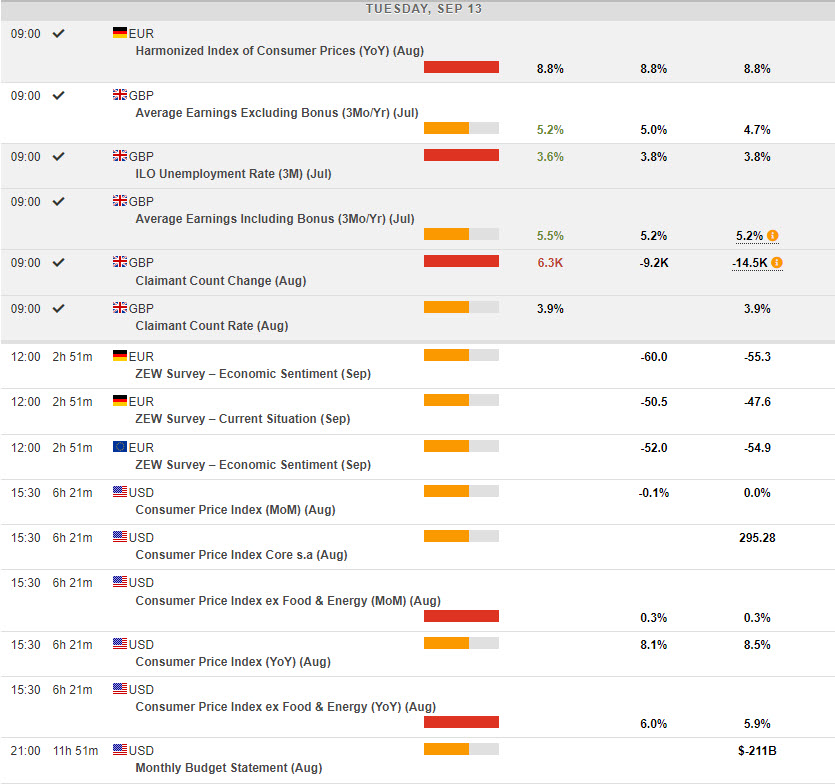

Overnight & Today – UK Jobs, (Wages beat & Unemployment Rate fell back, Claimant Count reversed sharply (+20.8k) German HICP (steady at 8.8%). To come German ZEW and US CPI.

Biggest FX Mover @ (06:30 GMT) AUDJPY (-0.51%) Signs the 6-week rally from 90.00, maybe cooling. Topped at 98.45 earlier back under 98.00 to 97.76 now. MAs aligning lower, MACD histogram & signal line positive but falling, RSI neutral 43.20, H1 ATR 0.174, Daily ATR 0.972.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 14 – Inflation IS Sticky – Risk Off.

Trading Leveraged Products is risky

*USDIndex – Exploded higher (to110)ending a 4-day dip. US CPI much hotter than expected. Fed Funds Futures – a 34% chance of 100bp – from 0% this time yesterday. Inflation may still have peaked but it is NOT receding as quickly as some expected, Inflation is ALWAYS sticky and often takes longer to get under control.

*EUR – Trades at 0.9980 now from a test of 0.9950 yesterday, 1.0000 resistance.

*JPY BOJ apparently conducting rate checks ahead of intervention. USDJPY hit 145.00 yesterday from 142.00 and trades at 143.75 now following the BOJ chatter.

*GBP traded over 1.1700 yesterday ahead of the US data, but tanked under 1.1500 to 1.1485 and holds at 1.1500 now.

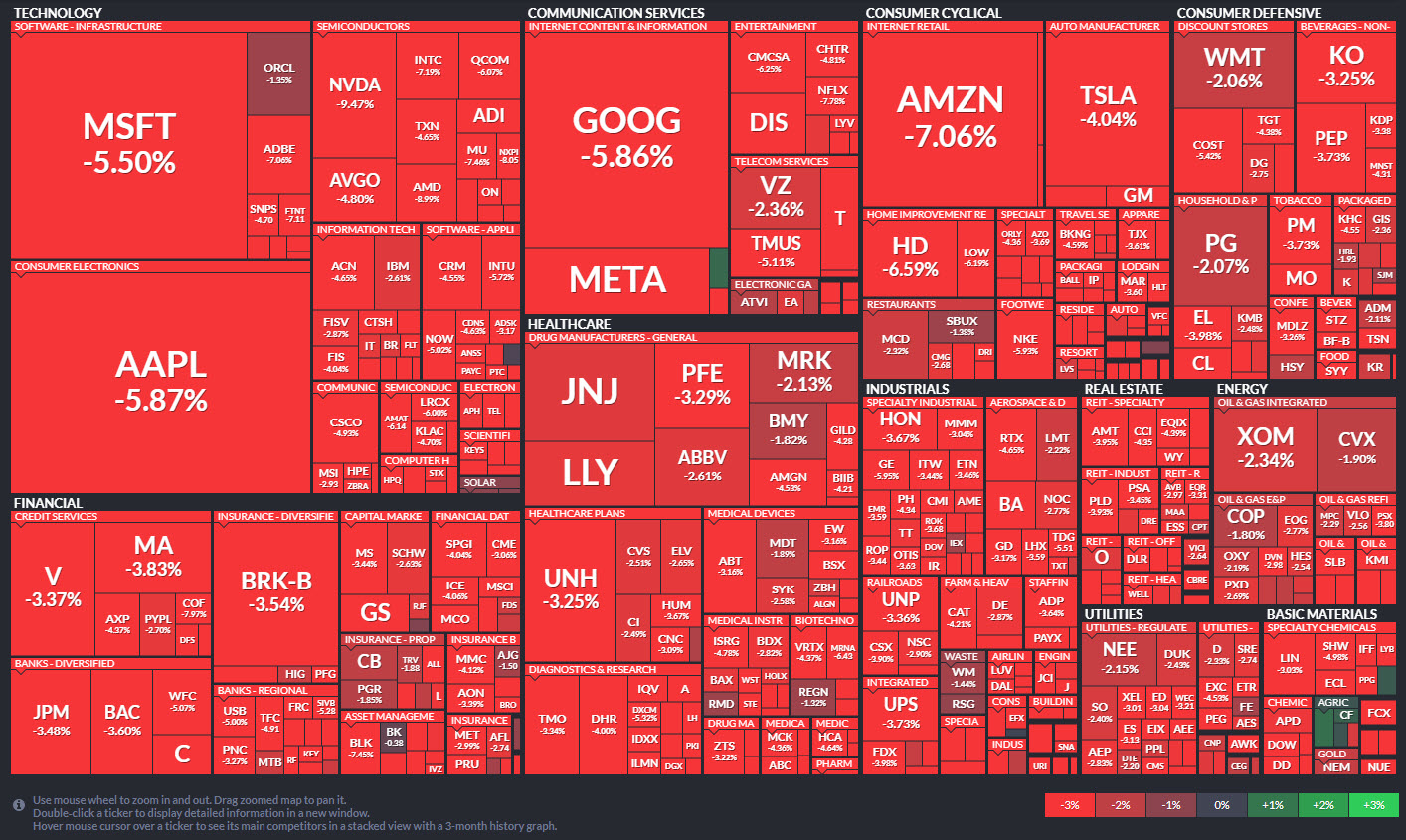

*Stocks US stocks had their worst day since June 2020 (S&P500 -4.32% 177pts 3932) FUTS trade at 3940. NASDAQ worst performer (-5.16%) Asian stock markets down over -2.5%, with European FUTS showing some resilience (-0.4%).

*USOil topped at $89.00 again on Tuesday, crashing to the key $85.00 level before recovering to $87.00 now. 20-day moving average sits at $89.00.

*Gold – also tested lower under $1700 from $1730 and holds at $1700 now.

*BTC – slumped from $22.7 highs to $19.8k and holds at $20.2k now.

Overnight & Today – UK inflation a tick lighter at 9.9% vs 10.0% & 10.1% last month, US PPI, New Zealand GDP, Speeches from European Commission State of Union Address & ECB’s Lane.

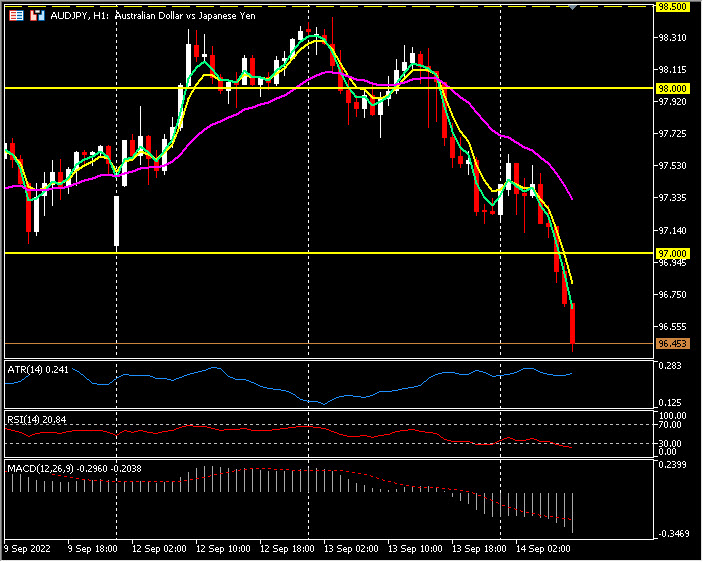

Biggest FX Mover @ (06:30 GMT) AUDJPY (-0.87%) The BOJ gossip and risk off mood has lifted safe haven YEN. Collapsed under 98.00, 97.00 & 96.50. MAs aligning lower, MACD histogram & signal line negative & falling, RSI 20.85 & OB, H1 ATR 0.241, Daily ATR 0.972.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 15 – USD Holds at Highs, Stocks Flat.

Trading Leveraged Products is risky

*USDIndex – Remains bid and back to test 109.85. US Mortgages over 6%, (Highest since 2008), 2/30yr. yields most inverted since 2000. 2/10’s 45 pts inverted. INFLATION the only story in town. Key next week will be the Fed’s new forecasts, and especially the dot plot and what it suggests about the terminal rate. Fed funds futures point to about a 4.4% rate in early spring.

*EUR – Trades at 0.9964 now and remains capped by Parity 1.0000 resistance. Lane yesterday suggested that another 75 bp rate hike is not a done deal. EU is looking for $140 billion for Winter Energy support.

*JPY BOJ intervention not imminent. Katayama: Japan lacks effective means to combat Yen’s sharp falls . USDJPY back to 143.75, 145.00 remains vital resistance.

*GBP back to key 1.1500 support zone now, having rejected 1.1600 yesterday.

*Stocks US stocks held at lows and remain subdued after Tuesdays bloodbath.(S&P500 +0.34% 13pts 3946) FUTS trade at 3965. Starbucks +5.53%, TSLA +3.59%. NASDAQ best performer (+0.74%) Asian stock markets also weak and European FUTS also flat.

*USOil topped at $90.00 yesterday and trades at $88.30 now. 20-day moving average sits at $89.00.

*Gold – remains anchored under $1700 trades at key $1688 now.

*BTC – slumped to $19.5k but holds at $20k now. Ethereum PARIS Merge successful this morning.

Overnight & Today – US Philly Fed, US Retail Sales, Speech from ECB’s de Guindos.

Biggest FX Mover @ (06:30 GMT) USDJPY (+0.39%) The BOJ intervention gossip & weak data not aiding the YEN yet. Rallied from 142.50 lows yesterday to 143.70 now 145.00 remains key resistance. MAs aligning higher, MACD histogram & signal line negative but rising, RSI 57.50, H1 ATR 0.227, Daily ATR 1.632.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

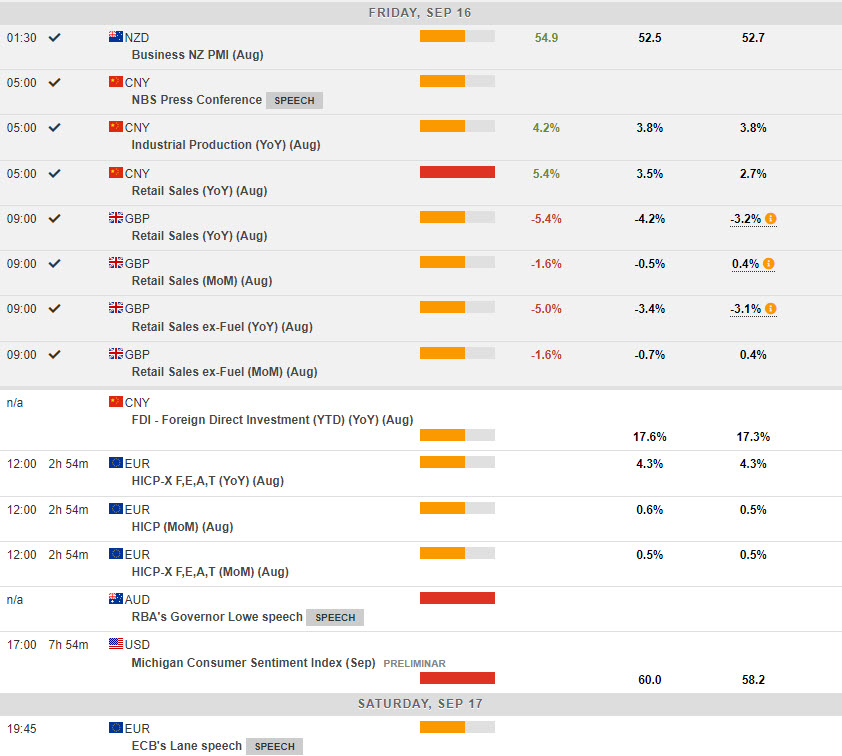

Market Update – September 16 – Dollar & Yields firmer, Stocks Gold & Oil weaker.

Trading Leveraged Products is risky

*USDIndex – Remains bid and back to test 109.60. Data released yesterday was mixed (positive Retail Sales and Claims, mixed Trade data and Manufacturing from Empire State & Philly Fed) but solid enough not to dissuade the Fed. A 75 bp boost is a done deal on Wednesday, with the risk for a 100 bp hike now 24%. And the Fed is likely to increase rates over the rest of the year to hit a 4.04% upper band in December and peak at 4.4% early 2023. In January the 10-yr yield was 1.77%, closed yesterday at 3.459%, just shy of June’s 3.47% high.

*EUR – Trades at 0.9978 now and remains capped by Parity 1.0000 resistance.

*JPY – More intervention chatter, Suzuki: concerned about one-sided yen weakening. USDJPY back to 143.60, 145.00 remains vital resistance.

*GBP broke below key 1.1500 support zone, 1.1420 now, as Retail Sales disappoint adding to the cost of living crisis.

*Stocks US stocks moved lower and remain pressured after Tuesdays bloodbath.(S&P500 -1.13% -44.66pts 3901) FUTS trade below key 3900 at 3892. Adobe -17%, MFST -2.70%, NFLX +5.02%. NASDAQ worst performer (-1.43%). Asian stock markets also sank (Nikkei -1.11% & Shanghai Comp. -1.97%) – Chinese property sector remains weak but strong Retails Sales and key August indicators were better-than-expected. European FUTS lower, FTSE100 FUTS – a tad higher on weaker sterling.

*USOil plunged over 4% to $84.35 lows, from a test of $90.00 on Wednesday. Trades at $85.40 now.

*Gold – also plunged below key support areas at $1688 and $1680, to $1658 (April 2020 lows) now.

*BTC – slumped to $19.4k and trades at $19.7k now. Ethereum PARIS Merge successful yesterday but he coin lost -5% and trades at $1468 today.

Overnight & Today – EU Final CPI, UoM Consumer Sentiment & Inflation Expectations, Quadruple Witching, Speeches from ECB’s Lagarde & Villeroy.

Biggest FX Mover @ (06:30 GMT) GBPUSD (-0.46%) Weak UK Retail Sales adds to Sterling’s woes. Sank under vital 1.1500 yesterday to 1.1418 now. MAs aligning lower, MACD histogram & signal line negative & falling, RSI 27.50 & OS, H1 ATR 0.00158, Daily ATR 0.01188.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 19 – Big central bank week; Risk of a super-sized hikes!

Trading Leveraged Products is risky

*USDIndex – Remains bid, holding above 109. The surprisingly hot August CPI report generated a sea-change in policy outlook, while housing starts and existing home sales will be tracked. The housing sector has been a major casualty of the FOMC’s tightening policies. Starts are seen rebounding slightly to a 1.450 mln clip after tumbling -9.6% to 1.446 mln in July. Existing home sales are projected dropping to a 4.685 mln rate following July’s decline to 4.810 mln. A 75 bp boost is a done deal on Wednesday.

*EUR – Trades at 0.9976. Recession risks are increasingly palpable in Europe.

*JPY – down 0.2% at 143.21 – verbal interventions effect in the yen has faded this week.Strong resistance at 145. Japan is on holiday today & Friday. BoJ is expected to maintain the accommodative stance & stick with massive stimulus .

*GBP just under the 1.14 mark. Markets are split on whether the BOE will raise rates by 50 or 75 bps on Thursday and to the government’s fiscal plans as Chancellor Kwarteng is set to unveil a “mini-budget” on September 23. The energy package aside, Kwarteng is expected to unveil cuts to National Insurance payments and the reversal of plans to increase corporation tax from 19% to 25%in April. PM Truss is also preparing a post-Brexit deregulation push and hopes that her measures will boost growth sufficiently to allow the financing of measures in the medium term.

*Stocks in red with ASX and Nikkei lost -0.3% and -1.1% respectively, while Hang Seng and CSI 300 are down -1.3% and -0.5% at the moment. Reports that the Chinese city of Chengdu reopened after lifting a two-week lockdown and a liquidity injection from the PBOC may have helped to put a floor under mainland China bourses at least. The GER40 future is fractionally lower, US futures underperforming, led by a –0.8% correction in the USA100. UK markets will remain closed today for the late Queen’s funeral.

*USOil – at $83.83 next support at $80.

*Gold – slipped on Monday, at $1661 pressured by a strong USD.

*BTC – retests 3-month low at mid $18500 area.

Overnight & Today - EU Construction Output & Japanese CPI.

Biggest FX Mover @ (06:30 GMT) BTCUSD (-4.72%) Sank to 3-month low at 18400 area. MAs aligning lower, MACD histogram & signal line negative & falling, RSI 21, H1 ATR 231.98, Daily ATR 1112.90.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – steadied at 109 – 109.30, as Treasuries were weaker on the day and closed near their lows as the market awaits an all-but-done 75 bp rate boost. The 2-year US Treasury yield , which is extremely sensitive to policy expectations, rose as high as 3.970% overnight for the first time since November 2007. The 10-year yield reached a high of 3.518%, a level not seen since April 2011.

*EUR – back to parity (1.0030) after it dropped as low as $0.9864 on Sept. 6 for the first time in two decades.

*JPY – at 143.40, in a week following consolidation. The BoJ decides policy on Thursday, and is widely expected to keep its ultra-easy stimulus settings unchanged — including pinning the 10-year yield near zero — to support a fragile economic recovery.

*GBP – at 1.1445, finding some ground after the 37-year low. Consensus expectations predict a 50 bp move from the BoE, although a 75 bp move is likely to be discussed.

*Stocks: A late-day rally left the US100 up 0.76% at 11,535, while the US30 and US500 rose 0.64% and 0.69%, respectively, to 31,019 and 3899. Nikkei was up 0.45% at the close, the ASX managed a 1.29% gain, while CSI and Hang Seng are currently up 0.2% and 1.1% respectively. GER40 and UK100 futures are up 0.3% and 0.6% respectively.

*Apple rallied by 2.51% yesterday. The company announced yesterday that prices of apps and in-app purchases on its App Store will increase in several countries including Japan, Malaysia and all territories that use the euro currency, from next month. Also in a statement to Bloomberg, Apple has acknowledged the iPhone 14 Pro’s camera shaking issue and has revealed that it will release a software update to fix this. This update should be out by next week.

*USOil – at $85 area after dipping to $82. US crude oil stocks are estimated to have risen last week by around 2 million barrels in the week to Sept. 16, a preliminary Reuters poll showed on Monday. European gas prices meanwhile continue to decline with Dutch TTF at EUR 170 per megawatt hour – the lowest since July 25. European governments are intensifying efforts to ease the reliance on Russian imports and there are also efforts underway to reform the energy market as governments move to reduce energy consumption in preparation for the winter. European inventories are almost 86% full, but if Russia doesn’t resume gas deliveries via Nordstream 1 it will still be a struggle to avoid power cuts.

Overnight & Today - US Building Permits & housing Starts, Canadian Inflation and the highlight is the ECB Lagarde speech, BoC Deputy Beaudry speech and RBA Assist Gov Bullock Speech.

Biggest FX Mover @ (06:30 GMT) GBPJPY (+0.42%) rallies to 164.35 (200-hour SMA). MAs aligning higher, MACD histogram & signal line turned positive and rising. RSI 69, H1 ATR 0.225, Daily ATR 1.557.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – September 21 – Riksbank spooked markets ahead of Fed, BoE, SNB & Norges Bank.

Trading Leveraged Products is risky

*USDIndex – extended gains to 110.26, stocks and bonds were down while the 10-year yield surged over 10 bps to hit 3.60%, but slid to finish at 3.555%. It is the first close over 3.5% since April 2011. The curve steepened to -39 bps from -45 bp.

*ECB’s Lagarde expects to raise rates further over the “next several meetings,” in her speech on Monetary Policy in the Euro Area. That and the surprisingly bold 100 bp rate boost from Sweden’s Riksbank kicked off a very heavy week of central bank decisions and got trading off on the back foot. The markets are repricing for the possibility other central banks will be in more of a rush to tighten policy.

*Putin declares partial military mobilisation to bolster Ukraine war effort.

*EUR – plummets below 0.9900.

*JPY – topped 144.00, before drifting by 60 pips on the EU open as Yen strengthened. The BoJ left its bond buying schedule unchanged and signalled ongoing focus on trying to cap yields which may have helped to soothen nerves.

*GBP – dipped to 1.1338, at 37-year lows.

*Stocks: US500 and the US30 were down just over -1%, with the US100 off -0.95%. European rates closed up over 10 bps, and bourses dropped over -1%. JPN225 and ASX closed with losses of -1.6% and -1.4% respectively yesterday, and Hang Seng and CSI 300 are currently down -1.2% and -0.3%. US and European equity futures are also in the red.

USOil – ticked up to $85.50.

Overnight – BoJ maintains bond buying program, with the focus on trying to keep a lid on yields, ahead of the policy decision later in the week. The BoJ plans to buy 150 billion yen of debt in the 5-10 year and 100 billion yen of securities with maturities of 10-25 years. That is on top of the offer of unlimited purchases of 10-year bonds at 0.25%. The 10-year rate climbed to the 0.25% upper limit of the BoJ’s tolerated range last week for the first time in three months, as officials tried to talk up the Yen.

Today – The FOMC began its 2-day meeting.

Biggest FX Mover @ (06:30 GMT) EURJPY (-0.80%) dipped to 142.00. MAs aligning lower, MACD histogram & signal line turned negative and falling. RSI 69, H1 ATR 0.271, Daily ATR 1.56.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – extended gains to 111.51, as the FOMC boosted rates by 75 bps, but it was a much more hawkish result than that. The SEP revisions were the focus and they did not disappoint, with the dots coming in much higher than expected, steepening the near-term trajectory and concluding with a higher than previously forecast terminal rate. Chair Powell also stated the policy path the Fed actually takes will be enough to get the job done.

*Yields: 2-year finally climbed through 4% to close at 4.03%, the first time with that handle since October 2007. The 10-year was 5 bps richer at 3.510% after surging to 3.624% just after the Fed’s release.

*EUR – lingering at 0.9820.

*JPY – lifted to 145.44, as Kuroda’s warning on the Yen may help to limit the move higher as it leaves markets speculating about direct intervention in forex markets, although most expect Japan to try and enlist support from the US and shy away from going it alone.

*GBP – dipped to 1.1220.

*Stocks in the red with losses of -1.79% on the US100, and -1.7% on the US30 and US500. GER40 and UK100 futures meanwhile are down -1.6% and -0.8% respectively.

*USOil – at $83.00, as supply concerns are counterbalanced by speculation that aggressive central bank action will hit the recovery.

Overnight – BoJ will continue with the easy policy settings until the 2% inflation goal is met, adding that the bank won’t hesitate to ease policy settings further if needed. FOMC boosted the rate band 75 bps as expected, from 3.0% to 3.50%. This makes a total of 300 bps in rate increases to the highest since 2008. And more hikes are on the way as the policy statement reiterated that the Committee “anticipates that ongoing increases in the target range will be appropriate.” Additionally, the dot plot showed a median funds rate at 4.4% for the end of 2022, or about 125 bps of hikes from here, keeping another 75 bp increase on the table. The median rate is at 4.6% for the end of 2023. The vote was unanimous. This is a hawkish 75 bp hike, and it’s a higher for longer stance through 2023.

Today – The SNB delivers 75 bp hike as expected. Hence focus turns to BOE announcement and US jobless claims.

Biggest FX Mover @ (06:30 GMT) CHFJPY (+1.03%) MAs aligning higher, MACD histogram & signal line turned positive and rising. RSI 78, H1 ATR 0.471, Daily ATR 1.599.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – holds above 111.

*Yields: 10-year surged 18 bps to hit 3.71% but finished at 3.69%. 2-year was 9 bps higher at 4.15% before easing off. It was an 11th straight session of losses, the longest on record (data going back to 1976), according to Bloomberg. The 10-year has sagged for 13 consecutive days. The curve inverted to -54 bps early on before rising to -42 bps late in the day.

*EUR – broke below 0.9800.

*JPY – remained supported after officials stepped in and intervened on forex markets yesterday. USDJPY is at 142.20.

*GBP – remains in the doldrums with Cable at 1.1200.

*Stocks were mired in the red, at 2 year lows, with weakness in consumer discretionary and financials. Some bargain hunting lifted the indexes off of their lows and saw the US30 edge fractionally higher temporarily, but dropped at the close to finish down -0.35%. The US100 lost -1.37%, and the US500 was off -0.85%.

*USOil – hovering at 80-82 area.

Overnight – Globally hot inflation rates have resulted in historically tough action from nearly every central bank around the world this week and over the month. Over the past 24 hours there has been a total of 250 bps in rate increases. Many emerging market central banks have been in action too, forced to keep pace with the Fed and to defend their currencies. South Africa lifted rates 75 bps, with Indonesia and the Philippines hiking 50 bps. The BoJ remained the odd man out, though it intervened in the currency market to support JPY. While the FOMC’s 75 bp hike was expected, the upward revisions in the dots to a 4.6% estimate for the terminal rate, and Chair Powell’s hawkish stance, caused much of the repricing in the markets. Additionally, Powell’s warning that there will be further pain in the housing market and that the risks for recession were on the rise exacerbated investor angst. That and the rise in yields knocked mega-tech sharply lower. Nevertheless, many doubt the FOMC will carry through with its projected policy path, while some found buying opportunities amid the downdraft in stocks.

Today – Preliminary PMIs from UK, Germany, EU, and US alongside Canadian Retail Sales and Fed’s Chair Powell.

Biggest FX Mover @ (06:30 GMT) GBPUSD (-0.63%) MAs aligning lower, MACD histogram & signal lines extend well below 0, RSI 30.62, H1 ATR 0.00175, Daily ATR 0.01282.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

*USDIndex – surged to 114.40 before settling at 113.64. 10-year yields jumped 5.5 bp in Australia and are currently 7.6 bp higher in the US. 2-year Treasury yields broke above 4.3% to a new 15-year high.

*EUR – The Eurozone and the wider EU are also facing the challenge of a new right-wing government in Italy, with Draghi’s likely successor not only the first woman, but one with far-right convictions that could bring her in conflict with Brussels and Frankfurt. EURUSD at 0.9635.

*JPY Japan’s Finance Minister threatened further intervention today, but the Yen was again under pressure and fell about 0.6% to the weaker side of 143.86.

*GBP dropped to an all-time low against the USD (at 1.033) as Friday’s mini-budget intensified concern about the fiscal situation. Speculation of an emergency response from the Bank of England, as confidence evaporated in Britain’s plan to borrow its way out of trouble, spooked investors piling into US Dollars. Currently settled at 1.0615.

*Stocks: Eurozone stock futures are selling off in tandem with US futures, while the UK100 future has found a footing as the slump in Sterling lends a helping hand. Across Asia the Nikkei closed -2.6% lower, the ASX declined -1.6% and Hang Seng and CSI 300 have lost -0.02% and -0.52% respectively so far.

*USOil plunged to $77.58 as recession concerns mount. Attention turns to OPEC+, on Oct. 5, after agreement to cut output modestly at their last meeting.

*Gold – drifted to $1636, with next floor at $1560.

*BTC – hovering around 2-month low at $18k area.

Overnight & Today – China steps up fight to support the Yuan. The PBOC announced today that it will impose a 20% risk reserve requirement on banks’ foreign-exchange forward sales to clients. The currency is heading for the lower end of the allowed trading band against the Dollar, despite stronger than expected fixings since August. Officials also reduced the banks’ foreign-currency reserve requirements earlier this month to boost the Yuan, but so far, the measures haven’t really halted the slide in the currency and today’s move is also not expected to do much more than slow the slide.

Biggest FX Mover @ (06:30 GMT) EURGBP (+2.19%). Topped at nearly 2-year highs at 0.9250, before correcting back to 0.9045. Intraday MAs aligning lower, MACD histogram & signal line hold positive, RSI declines to 61, H1 ATR 0.0065, Daily ATR 0.0094.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Новости

Новости Фотогалерея

Фотогалерея Клубы

Клубы Каталог

Каталог Оставить отзыв

Оставить отзыв Пользователи

Пользователи Объявления

Объявления Хостинг

Хостинг Технический анализ

Технический анализ Конкурсы фото

Конкурсы фото ПОЛНЫЙ СПИСОК

ПОЛНЫЙ СПИСОК Блоги

Блоги