Market Update – June 14 – Is the ugly Monday over?

Trading Leveraged Products is risky

USD spiked (USDIndex 105.10), Stocks plummeted once again (NASDAQ -4.68%, Dow -800pts & S&P close to -151pts). Friday’s hot CPI report; low consumer sentiment; stagflation worries continued; and global uncertainty over how hard the FOMC will have to slam on the brakes to slow demand and bring down inflation. Yields higher on fears of aggressive interest rate hikes would push the world’s largest economy into recession (US 5yr & 10yr back over 3.57% & 3.48%, 2yr at 3.33%). Asian markets have sold off in catch up trade, (Nikkei -1.30%). Oil up, Gold remains pressured by rising yields.

* USDIndex rallied to 105.10.

* Equities – Hang Seng and CSI 300 are up 0.3% and 0.4% respectively. GER40 and UK100 futures are posting gains of 1.0% and 0.8%, while a 1.6% rise in the USA100 is leading US futures higher.

* Oil & Gold had weaker sessions – USOil struggles to break $122.00 handle, Gold is slumped on the Fed outlook and the strength in the USD, to $1809.

* Bitcoin TANKED to $20,796. – Major cryptocurrency lending company Celsius Network’s freezing of withdrawals delivered the latest jolt to investors in the asset-class.

* FX markets – EURUSD down at 1.0458, USDJPY tested 135 zone, Cable trades up at 1.2200, from 1.2120.

Overnight – ILO unemployment rate jumped to 3.8%. German HICP inflation was confirmed at 8.7% y/y, in line with the preliminary number. The national CPI rate stood at 7.9% and inflation is at the highest level since 1973, during the first oil price crisis. Chaoyang kicked off a three-day mass testing campaign among its roughly 3.5 million residents.

Today German ZEW, US PPI and ECB’s Schnabel speech.

Biggest FX Mover @ (06:30 GMT) BTCUSD (-7.02%). Drifts to 20781. Next key resistance is at 2017 peak, 19470. Intraday, MAs flattened, MACD histogram negative, RSI 23 but rising, indicating some temporary bounce but overall downtrend.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

USD down (USDIndex 104.70), Stocks mixed (NASDAQ +0.18%, Dow -0.5% & S&P -0.38%). A boost to Australia’s minimum wage and RBA pledge to do what is necessary to meet the inflation target fueled the jump in yields. Expectations are now for 50 bp hikes in July as well as September and Australia’s curve shifted more than 20 bp higher today. – Yields extended higher as dip buyers have thrown in the towel for now, leaving sellers in control as the market adjusts to the potential for a very hawkish FOMC. (US 5yr & 7yr rates up to 3.606% and 3.59%, 2yr at 3.43%). US PPI increased 0.8% in May and the core rose 0.5% – bearish for the markets. ECB to hold emergency meeting “to discuss current market conditions”. A Bloomberg source story yesterday suggested that the ECB remains tight lipped on new plan to keep spreads in.

“Against a backdrop of sky-high inflation, rising rates, and growing recession concerns, the S&P 500 has had its worst start to the year since 1962,” noted analysts at Goldman Sachs.

* USDIndex pulled back to 104.78.

* Υields have extended higher, at the highest rates in well over a decade. The 10-year cheapened over 12 bp to 3.488%, not seen since the spring of 2011.

* Equities – Nikkei and ASX lost a further 0.9% and 1.3% respectively. Hang Seng and CSI 300 are currently up 1.6% and 2.7%.

* Oil drifted to 116.55 before settling at 119.58 – amid FED and reports that US Senate Finance Committee chair Ron Wyden plans to introduce legislation setting a 21% surtax on oil company profits considered excessive.

* Golds near its lowest area in a month, now at $1,820.

* Bitcoin steady above $20K.

* BOJ offers to buy unlimited sum of JGBs with 7 years left until maturity.

* FX markets – EURUSD rebounded to 1.0498 from 1.0396, USDJPY back below 135 zone, Cable settled at 1.2040.

Today The focus will be on the ECB meeting but also on the dot plot and the terminal rate, as well as how Chair Powell assesses the outlooks of inflation, growth, and the labor market.

Biggest FX Mover @ (06:30 GMT) USDIndex (-0.35%) down to 50-hour SMA, 104.72. Intraday, MAs aligned lower, MACD histogram neutral, RSI 41 & sloping. H1 ATR at 0.14 & Daily ATR at 0.79.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – June 16 – Its all about the Banks.

Trading Leveraged Products is risky

FOMC hiked rates 75 bps, 10-1 vote; further increases likely appropriate. USD supported (USDIndex 104.80), Stocks higher despite Fed (NASDAQ +2.5%, Dow 1.4% & S&P +2%). Despite the Fed effecting the biggest increase in interest rates in 28 years, bonds and stocks rallied hard, underpinned by the fact Chair Powell said the 75 bps was an unusual move and would not be a common action, noting further hikes would be 50 bps or 75 bps. After hitting multi-month lows earlier this week, most regional currencies firmed on Thursday after US Bond Yields and the USD retreated from multi-year highs a day earlier as investors welcomed the Fed’s decision. It is clear that the Fed’s move will keep stagflation concerns alive. Asian markets traded mixed and US futures have pared earlier gains.

“Against a backdrop of sky-high inflation, rising rates, and growing recession concerns, the S&P 500 has had its worst start to the year since 1962,” noted analysts at Goldman Sachs.

* USDIndex held above 104.40.

* Υields 10-year Treasury yield climbed 1.5 bp to 3.3% while Australia’s bonds also moved up.

* Equities – GER40 and UK100 futures are mixed with the UK100 down -0.2% ahead of the BoE decision, the GER40 up 0.3%.

* Oil settled to 115.76 after a steep drop, supported by tight oil supply (100k b/d highest since April 2020) and peak summer consumption, after the Fed sparked fears of slower economic growth and less fuel demand.

* Golds at $1830 – safe-haven demand & inflationary hedge buying VS a higher interest rate.

* Bitcoin down to $20,157.

* FX markets – EURUSD at 1.0409, USDJPY back above 134, Cable down at 1.2100 ahead of BoE.

BoE Preview: The BoE is still set to deliver another 25 bps rate hike this week, but stagflation risks are looking nowhere as serious as in the UK That should prevent the central bank from joining the “50 bp club” of central banks, but for now is unlikely to stop the BoE from sticking to the tightening path. The statement may sound somewhat more cautious now. Even the BoE’s own scenario suggests a technical recession next year and the latest batch of forecasts from the OECD and others highlight that the economy is under-performing, with the fallout from Brexit, the sanctions against Russia, and political turmoil all weighing on the growth outlook. PM Johnson managed to survive a confidence vote last week, but many feel that his days are numbered. Even within his own party the threat to unilaterally step back from the Northern Ireland protocol is not very popular and rather than uniting the nation behind Brexit, the government is facing an increasingly fragmented union. Nevertheless, with inflation running far above target, the BoE has little choice but to lift rates further for now, especially as house price inflation is also still running at double digits, and wage growth is picking up in tight markets.

Biggest FX Mover @ (06:30 GMT) GBPUSD (-0.84%) down to 1.20 area again. Intraday, MAs bearishly crossed, MACD histogram declines but holds above 0, RSI 40 & sloping. H1 ATR at 0.00377 & Daily ATR at 0.01434.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

USD drifted (USDIndex 103.15) thanks to the hawkish SNB and BoE, and the potential for a shift from the BoJ. However, the BoJ eventually left policy on hold & maintained its ultra-low rate settings today, despite looking increasingly like the odd one out. Yen sinks. Stocks were crushed, hit by the surge in yields (NASDAQ -4.4%, Dow -2.4% & S&P -3.25%). Weakness in tech also weighed on USA100. VIX rose to an intraday high of 34.43, but dipped to 33.44 late in the day, versus Wednesday’s 29.62. Treasuries are rallying and yields are now richer (2-year declined to 3.10%, 10-year at 3.25%. They were as high as 3.39% and 3.49% on the day). European leaders back Ukraine’s bid to apply for EU membership.

*US mortgage rate surged 55 bps to 5.78%, the biggest weekly jump since 1987.

*US housing starts plunged -14.4% to 1.549 mln in May, permits fell to 1.695 mln.

*US Philly Fed index dropped to -3.3 in June, 6-month outlook fell to -6.8.

*US initial jobless claims slid -3k to 229k in June 11 week.

* USDIndex rebounded to 104.25 from 103.15.

* Υields 10-year climbed 5.5 bp to 3.25%.

* Equities – Nikkei and ASX lost -1.8% today. Elon Musk hints at layoffs in first meeting with Twitter employees.

* Oil settled at 117.50 – Oil set for weekly loss as traders weigh monetary tightening, although persisting supply tightness and new sanctions on Iran limited the downside.

* Gold retested $1856, currently lower at $1845. Platinum and palladium also set for weekly drops.

* Bitcoin steadily lower at $20k area.

Interest rate differentials between Japan and the US will continue to widen, which will keep pressure on the Yen, which at the start of the week was at the lowest level since 1998.

* FX markets – EURUSD at 1.0505, USDJPY back above 134.67, Cable at 1.2257 from 1.2405 highs.

Biggest FX Mover @ (06:30 GMT) CHFJPY (+1.54%) breaks 2013 peak. Intraday, MAs aligned higher, MACD lines extending northwards, RSI 76 & rising. ATR(H1) 0.0524 & ATR(D) at 1.506.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – Stocks & Yields Lift for Summer Solstice.

Trading Leveraged Products is risky

USD holds at highs (USDIndex 104.16), Stocks closed higher in Europe (DAX +1.01%, FTSE100 +1.50%) & Asian shares opened over 1% higher and closed positively (Nikkei +2.09%) US Futures +1.15%. Yields rallied (US 10yr 3.2976%). Oil ticks 2% higher, lifting CAD pairs, after Fridays sell-off and Gold & BTC slide sideways. Yellen talks of a “price cap” and “tax” for Russian oil exports and a tax “holiday” for gasoline in US to ease inflation. (Ruble @ 15 mth high). Japan PM Kishida & FM Suzuki: Rapid yen weakening is a source of concern. RBA’s Lowe rates need to go higher in low unemployment high inflation Australia.

Week Ahead – Will be dominated by Central Bank Speak topped by FED Chair Powell’s 2-day testimony to Congress. CPI & PMI data also due this week.

*USDIndex tested 104.00 on Monday and holds at 104.15 today.

*Equities – USA500 closed yesterday (Friday 3674), US500FUTS at 3725 now.

*Yields 10-year yield higher , trades at 3.29% now.

*Oil & Gold had mixed sessions – USOil recovered over 2% to trade at $110.20. Gold could not hold $1840 and trades at $1835 now.

*Bitcoin pivots off $20K, to test $21K now.

*FX markets – EURUSD holds at 1.0525, USDJPY holds over 135.00 zone shy of 24-yr high 135.50 and Cable trades up 20 pips to 1.2260.

Today - Canadian Retail Sales, US Existing Home Sales, New Zealand Trade Balance, Speeches from ECB’s Rehn, Fed’s Barkin & Mester.

Biggest FX Mover @ (06:30 GMT) CADJPY (+0.30%). Continues to move higher from 101.65 test on Thursday to 104.50, as Oil recovers from sell-off. Next key resistance 104.75 & 105.00. MAs aligning higher, MACD histogram positive & turning higher, RSI 71 ,OB but still rising, H1 ATR 0.139, Daily ATR 1.343.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – June 22 – Stocks rally, USD & Yields hold, Oil & Yen sink.

Trading Leveraged Products is risky

USD holds at highs (USDIndex 104.51), Stocks closed up over 2% (NASDAQ +2.51%) – (1) dead cat bounce & another bear market rally or (2) signs of peak inflation and peak Fed bearishness ? (Technicals & Fundamentals still say 1). Asian shares closed lower on rapid spread of new Omicron (Hang Seng -1.49%) Yields rheld their gains. Oil also slumped (Brent -3.42%) Gold & BTC slide sideways. Biden expected to announce temp. tax reprieve on gasoline, BOJ Mins confirmed they will ease further if necessary “without hesitation” USDJPY hits new 24-year high. NZD hit by weak trade data.

*USDIndex tested 103.72 on Tuesday before rallying to 104.55 now.

*Equities – USA500 closed +2.45% (3764), US500FUTS slumped to 3719 now.

*Yields 10-year yield higher, closed at 3.26% , trades at 3.29% now.

*Oil & Gold had mixed sessions – USOil slumped 3% to trade at $104.90. Biden & Omicron news weighed & Gold could not hold $1830 and trades at $1825 now on higher Yields and stronger USD.

*Bitcoin continues to pivot around $20K, test $22K yesterday, back to $20K now.

*FX markets – EURUSD hback under 1.0500, USDJPY hit new 24-yr highs at 136.71 and Cable trades down to 1.2225 now, following Inflation news, from 1.2325 highs yesterday.

Overnight - UK CPI hits 9.1% inline but up from 9.0% last month, CORE a tick lighter at 5.9% vs 6.0% & 6.2%, PPI beat 2.1% vs 1.8% & 2.7% prior and RPI also hotter at 11.7% vs 11.4% & 11.1% last time. NZ Trade Balance less than 50% of forecast at . Reuters Poll Fed Path: 75bp July, 50bp Sept & Oct, and 25bp Nov. (at the earliest). Japanese official – FX moves against the Yen “not ideal”.

Today - Canadian CPI, EZ Consumer Confidence, Speeches from Fed’s Powell, Barkin, Evans & Harker, SNB’s Jordan ECB’s de Guindos & Elderson, BoC’s Rogers.

Biggest FX Mover @ (06:30 GMT) NZDUSD (-1.18%). Collapsed from test of 0.6360 on Monday & Tuesday to 0.6250, as NZD Trade Balance missed significantly. MAs aligning lower, MACD histogram negative turning lower, RSI 21.25, OS but still falling, H1 ATR 0.00124, Daily ATR 0.00850.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – June 23 – USD & Yields slip, Oil down post Powell.

Trading Leveraged Products is risky

USD slips from highs (USDIndex 103.80), Stocks closed flat (NASDAQ & DJIA -0.15%) Yields tanked (-4%) after Powell said FED were “strongly committed” to the inflation fight and that recession was “certainly possible”. Asian shares mixed (Hang Seng +1.64%, Nikkei +0.8%, Kospi -0.7%) Oil slumped another -2% and Gold & BTC slide sideways. Biden announced tax reprieve on gasoline, but is under increasing political pressure, Johnson faces two more by-election defeats today & national rail strikes on-going, (6th Anniversary of Brexit vote) and Scholz fears gas line shutdown and unable to speak with Putin. USDJPY cooled from new 24-year high as JPY outperformed in Asian session.

*USDIndex tested 103.60 yesterday before recovering to 104.00 now.

*Equities – USA500 closed -4.9 (3759), US500FUTS lower at 3756 now.

*Yields 10-year yield higher, closed down -479% at 3.156% , trades at 3.18% now.

*Oil & Gold had mixed sessions – USOil slumped 2.2% to trade under $102 yesterday following Biden & Powell, back to $104.80 now. Gold spiked to $1845 and trades at $1834 now on weaker Yields and USD.

*Bitcoin continues to pivot around $20K, trades at $20.5K now.

*FX markets – EURUSD tested 106.00 yesterday back to 1.0560, USDJPY cooled from 136.71 yesterday to test 135.00 earlier & back to 135.83 now. Cable trades down to 1.2230 now from rally to 1.2330 yesterday.

Overnight - Japanese Manu PMI – miss (52.7 vs 53.5) UK Public sector borrowing hit £14bn last month, the third-highest May since 1993, and worse than the expected £11.6bn.

Today - EZ, UK & US Flash PMIs, US Initial Claims, Policy Announcements from Norges Bank, CBRT & Banxico, US Bank Stress Test Results, Fed’s Chair Powell Speaks at the House Finance Committee.

Biggest FX Mover @ (06:30 GMT) AUDJPY (-0.68%). JPY out performs today with safe haven bid. Rallied from 93.20 earlier to 93.70, next resistance the significant 94.00. MAs aligning higher, MACD histogram negative & still turning lower, RSI 42.45, and rising, H1 ATR 0.278, Daily ATR 1.49.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

USD slips from highs (USDIndex 104.00), Stocks closed higher (NASDAQ +1.62%) Yields slipped again (-1.66%) after no new news from Powell. Asian shares stronger (Hang Seng +2.24%, Nikkei +1.23%) Oil holds at lows, Gold dipped & BTC picked up. Ukraine gained EU candidacy status. UK PM Johnson’s Conservatives lost the two by-elections, triggering resignation of Party Chairman Dowden. European Futs +1.0%. USDJPY cooled further as NZD & AUD outperformed in Asian session.

* USDIndex tested 104.50 yesterday before slipping back to 104.00 now.

* Equities – USA500 closed +35 (3795), US500FUTS higher at 3824 now.

* Yields 10-year yield lower, closed down at 3.133% , trades at 3.018% now.

* Oil & Gold had mixed sessions – USOil rallied to $106.80 before slipping back to $104.50 now. Gold spiked to $1845 again but trades at $1822 now on weaker Yields and USD.

* Bitcoin continues to pivot around $20K, trades at $20.7k now from a test of 21k.

* FX Markets – EURUSD tested 1.0500 yesterday now back to 1.0536, USDJPY cooled again to 134.60 now. Cable trades at 1.2270 now, from lows at 1.2170 yesterday, despite by-election results and weak Retail Sales data, UK recession risks are stacking up.

Overnight - Japanese Core CPI inline & unchanged (2.1%) SPPI hotter (1.8%) UK Retail Sales a tick better than expected (-0.5% vs -0.6%) but down significantly from 1.4% last month.

Today - German Ifo, US New Home Sales, Speeches from Fed’s Bullard & Daly, ECB’s de Cos, BoE’s Pill.

Biggest FX Mover @ (06:30 GMT) NZDUSD (+0.49%). NZD out performed today. Rallied from 0.62500 test yesterday to 0.6300 now and a key resistance. MAs aligning higher, MACD histogram positive & rising, RSI 56.58 & rising, H1 ATR 0.00127, Daily ATR 0.00843.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 4 – USD & Stocks hold gains, Yields slip.

Trading Leveraged Products is risky

USD holds around Fridays close (USDIndex 104.85), Stocks closed higher on Friday (S&P500 +1.06%) but FUTS have slipped and Yields are down again (-4.51%). Asian shares are mixed after Chinese developer Shimao defaults and Covid concerns rise again. (Hang Seng -0.30%, Nikkei +0.84%) Oil ticks higher, Gold tests $1815 & BTC tests $19k. European FUTS also mixed. Russia claims victory in “liberated” Luhansk region and accuses Ukraine of shelling Belgorod. AUD outperforms in Asian session.

Week Ahead – Topped by NFP on Friday, FOMC Minutes on Wednesday and RBA rate decision tomorrow.

* USDIndex tested 105.36 Friday before slipping back to 104.85 now.

* Equities – USA500 closed +39 (3825), US500FUTS lower at 3810 now.

* Yields 10-year yield lower, closed down at 2.889% , trades at 2.880% now.

* Oil & Gold had mixed sessions – USOil has rallied to $108.70 now from $104.55 Friday. Gold spiked to $1815 earlier from a $1785 low on Friday.

* Bitcoin continues to trade under $20K, testing $19K today.

* FX Markets – EURUSD tested under 1.0400 Friday following record CPI (8.6%) now back to 1.0425, USDJPY cooled again to 134.75 on Friday back to 135. 40 now. Cable trades at 1.2110 now, from lows at 1.1975 Friday after weak PMIs.

Overnight - Australian Building Approvals jumped surprisingly to 9.9% vs -2.0%. German Trade Balance, missed significantly, turning negative at -1.0b vs. 4.2b, & Swiss CPI, hotter at 0.7%.

Today - EZ PPI, Speeches from ECB’s Elderson, Nagel & de Guindos, US Independence Day holiday.

Biggest FX Mover @ (06:30 GMT) AUDJPY (+0.60%). AUD out performed today. Rallied from 91.40 test on Friday to 92.64 now and a key resistance. MAs aligning higher, MACD histogram negative but rising, RSI 58.3 & rising, H1 ATR 0.251, Daily ATR 1.432.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 5 – USD Hold Gains, RBA Acts, Stocks Steady.

Trading Leveraged Products is risky

USD holds at highs (USDIndex 104.85), Stocks closed higher in Europe and hold gains in Asia with US FUTS higher too. Yields are flat but off recent lows. Asian markets buoyed by positive Yellen-Liu He meeting, prospect of Chinese & Australian Fin. Min. meeting this week and better PMI data from Japan & China, all despite action from the RBA. Covid concerns continue to weigh (Hang Seng +0.07%, Nikkei +1.04%) Oil ticks to $110, Gold holds over $1800 & BTC regains $20k. JPY underperforms in Asian. RBA raises rates in line with expectations by 50bp to 1.35%.

* USDIndex tested 105.00 Monday before slipping back to 104.85 now.

* Equities – USA500 closed +39 (3825), Friday US500FUTS higher at 3854 now.

* Yields 10-year yield lower, closed down Friday at 2.889% , trades at 2.880% now.

* Oil & Gold had mixed sessions – USOil rallied to $110.40 earlier from $108.00 Monday. Gold holds between resistance at $1815 and support at $1800, trading at $1808 now.

* Bitcoin continues to trade around $20K, testing $20.3K today.

* FX Markets – EURUSD remains pressured at 1.0430, USDJPY rallied to 136.30 earlier from under 135.00 Monday. Cable trades at 1.2110 now.

Overnight - China Services PMI’s better at 54.3 vs 47.3, Japanese Service PMI also improve at 54.0 vs 52 last time.

Today - EZ/UK Services and Composite Final PMIs, US Factory Orders, BoE Mins. & FSR, Speeches from BoE’s Bailey & Tenreyro.

Biggest FX Mover @ (06:30 GMT) EURJPY (+0.54%). JPY weaker today. Rallied from under 140.00 Thursday to 142.20 now, next resistance, 142.75 & 143.00. MAs aligning higher, MACD histogram positive & rising, RSI 66.00 & rising, H1 ATR 0.212, Daily ATR 1.402.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 6 – Dollar Dominates on Global Recession Fears.

Trading Leveraged Products is risky

USD moves to 20-year highs (USDIndex 106.34), US Stocks fell 2% on open but closed positively (NASDAQ +1.75%). Global PMI data overall in line. European markets fell 2%+ & Asian markets are negative (Hang Seng -2.38%, Nikkei -1.2%). Yields closed down -2.77%. Oil tanked -8.2% trading under $100, Gold closed under $1765 & BTC rotates at $20k. EUR fell to new 20-year lows with parity in sight. Heavy fighting in Donetsk adds to the sombre mood. UK PM lost two cabinet ministers adding to woes for Johnson and Sterling.

* USDIndex tested 106.55 and remains on Bid at 106.25 now.

* Equities – USA500 closed +6.0 (3831), after a weak day, US500FUTS at 3818 now.

* Yields 10-year yield lower, closed at 2.808% , trades at 2.802% now.

* Oil & Gold had weak sessions – USOil tanked under $100.00 to $97.30 lows, back at $100 now. Gold fell to 1762 earlier, 1768 now.

* Bitcoin continues to trade around $20K, testing $20.1K today.

* FX Markets – EURUSD remains pressured at 1.0260, USDJPY rallied from under 135.00 to 135.80 now. Cable trades at 1.1932 now.

Overnight - German Factory Orders better at 0.1% from -1.8%.

Today - EZ Retail Sales, US ISM Services PMI, FOMC Minutes, Speeches from Fed’s Williams & BoE’s Pill.

Biggest FX Mover @ (06:30 GMT) CADJPY (-0.42%). CAD JPY weaker today. Fell from allied from under 106.00 Tuesday to 103.50 today before recovering. MAs aligning lower, MACD histogram neagtive but flat, RSI 41.00 & rising, H1 ATR 0.291, Daily ATR 1.378.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 7 – Fed focused on Inflation, USD bid, Stocks flat, Gold tumbles.

Trading Leveraged Products is risky

USD moved down from new to 20-year highs at 107.00 but remains in demand (USDIndex 106.64), US Stocks flat on close (NASDAQ +0.35%). FED Minutes leaned to the hawkish side. – ‘more restrictive’ policy as likely if inflation fails to come down. Asian markets are mostly positive (Hang Seng -0.13%, Nikkei +1.4%). Yields closed up +3.3%. Oil fell another -1.0%, Gold plummeted again to $1735 & BTC rotates at $20k. UK PM Johnson has now lost over 50 members of his government but refuses to resign. AUD outperforms overnight.

Yesterday US ISM Service PMIs were better than expected but still at 25-mth low & JOLTS showed 11.25m job vacancies (1.9 jobs for every unemployed person).

* USDIndex tested 107.00 and remains on Bid at 106.65 now.

* Equities – USA500 closed +0.36% 13.69pts (3845), US500FUTS at 3854 now.

* Yields 10-year yield higher, closed at 2.92%, trades at 2.90% now. Yield curve inverted again yesterday.

* Oil & Gold had weak sessions – USOil traded down to $95.10 lows and remains under $100.00 at $98.48. Gold fell to 1732, next support at 1725, trades at 1745 now.

* Bitcoin continues to trade around $20K, testing $20.3K today.

* FX Markets – EURUSD remains pressured at 1.0200, USDJPY rallied from under 135.00 to test 136.00 now. Cable trades at 1.1950 now.

Overnight - German Industrial Output missed at 0.2% from 1.3%. Australian Trade Balance much better at 15.97b vs 10.7b & 13.25b prior.

Today - US ADP Employment & International Trade, ECB Minutes, EIA Oil Inventories, Speeches from Fed’s Waller & Bullard, ECB’s Lane & Enria, BoE’s Pill.

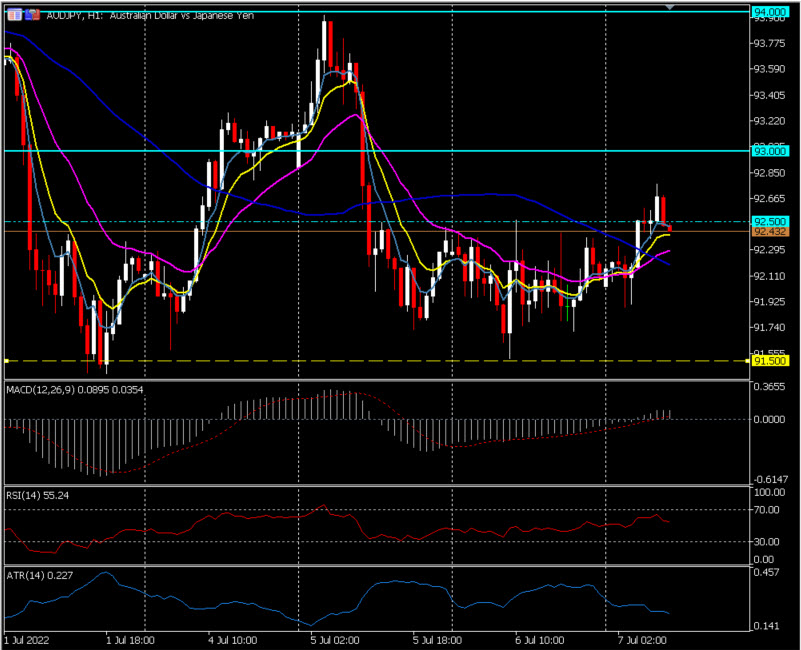

Biggest FX Mover @ (06:30 GMT) AUDJPY (+0.42%). AUD lifted by trade data. Rallied form allied from 91.50 Wednesday to 92.70 today before cooling. MAs aligning higher, MACD histogram positive & rising, RSI 55.24 & rising, H1 ATR 0.227, Daily ATR 1.398.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 8 – Stocks Rise, USD holds, Johnson Resigns, Abe Shot.

Trading Leveraged Products is risky

USDIndex tested 107.00 again following safe haven bids for USD & JPY following shooting of former Japanese PM Shinzo Abe (he remains in a critical condition). US Stocks rallied into close (NASDAQ +2.28%), lifting on hopes of less restrictive FED despite the tone of the minutes. Asian markets were positive before shooting closing flat. (Hang Seng +0.22%, Nikkei +0.1%). European FUTS positive too. Yields closed up +3.85%. Oil rallied 4.3%, Gold flat up 0.2% & BTC rallied to $22k. UK PM Johnson resigned but will remain caretaker PM for now (FTSE100 gained 1.14%, Cable recovered to 1.2000).

* USDIndex holds the bid at 107.00

* Equities – USA500 closed +1.50% 57.54pts (3902), US500FUTS at 3899 now.

* Yields 10-year yield higher, closed at 2.85%, trades at 3.05% now.

* Oil & Gold had volatile sessions – USOil traded up to $104 from $96.60 lows and remains over $100.00 at $102.00. Gold fell to $1742, and rotates their currently.

* Bitcoin rallied from $20K, testing $22.4K today on chatter of major investments coming.

* FX Markets – EURUSD remains pressured at 1.016, USDJPY capped by 136.00 traes at 135.50 now. Cable traded to 1.2050 at 1.2000 now.

Overnight - A weak set of data from Japan – Household spend -0.5% vs 2.2%, Econ. Watchers Sentiment 52.9 vs. 55.0.

Today - US & Canadian Labour Market Reports, US Wholesale Inventories, Speeches from ECB’s Lagarde & Fed’s Williams.

Biggest FX Mover @ (06:30 GMT) GBPJPY (–0.39%). JPY safe haven bid following ABE shooting stemmed the rally to 164.00 from 160.40 on Wednesday. Down to 162.80 now. MAs crossed lower, MACD histogram positive but falling, RSI 44 & falling, H1 ATR 0.319, Daily ATR 1.983.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 11 – Stocks pressured, USD gains.

Trading Leveraged Products is risky

The NFP report was slightly disappointing overall (372k June payroll gain & -74k in downward revisions). USD & Yields spiked, with USDIndex 107.59. Fed funds futures are dropping as the jobs report gives no reason for the FOMC to slow its policy trajectory, keeping a 75 bp hike at the July 26-27 FOMC intact and 50 bp move at the September 20-21 meeting. Stocks remain under pressure. Asian stocks struggled further overnight, with China bourses once again hit by lockdown concerns. Chinese CPI hotter at 2.5% vs 2.1%, but PPI cooler 6.15 vs 6.4%. COT report shows long positions on USD were reduced.

China discovered its first case of a highly transmissible Omicron subvariant in Shanghai and that new cases jumped to 63 in the country’s largest city from 52 a day earlier.

* USDIndex is heading for a new 20 year high – eased a bit at 107.23.

* Yields: The 2-year rate is up over 3.119%, 3-year at 3.165% & 10-year higher at 3.095%.

* Stocks : USA30 was down -0.15%, while the USA500 was off -0.08%. The USA100 rose 0.12%. In Europe, the picture is not much better and GER40 and UK100 futures are down -1.4% and -1.0%. Twitter fell 5% (with more to come) after MUSK withdrew the $44bln offer. The market mood will be tested by earnings from JPMorgan and Morgan Stanley on Thursday, with Citigroup and Wells Fargo the day after.

* Oil prices fell slightly today reversing some gains amid lockdown fear in China, i.e. concerns about tight supply. USOIL at $102.96 – New mass COVID testing in China potentially hitting demand.

* Gold steady for a 3rd day at $1,732-$1,750.

* FX Markets: USDJPY at 137.26 – 24-year high. Japan’s ruling conservative coalition’s strong election showing indicated no change to lose monetary policies.

Today - Fed’s Williams speech.

Biggest FX Mover @ (06:30 GMT) EURUSD (–0.62%) down to 1.0105. MAs aligning lower, MACD histogram negative & declining, RSI 31, H1 ATR 0.0014, Daily ATR 0.01032.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 12 -USD spiked, Oil fell & Euro closer to parity.

USD spiked, Oil fell and the Euro inched closer to parity. The strong haven bid rise as the prospect of further tightening by central banks, renewed COVID outbreaks in China and Europe’s energy shortages spooked investors. The Fed’s George, the dissenter in favor of a 50 bp June hike, noted concerns over aggressive policy action & the hawk Bullard still favors a 75 bp move. Recession angst again cropped up and hammered equities with weakness in megacap tech knocking the USA100 down -2.26%. USDIndex above 108.00. Wall Street’s losses have deepened. China imposing strict covid restrictions amid a rise in the subvariant BA.5 Omicron. Earnings season starts on Thursday with JPMorgan kicking it off. It could be a tough season for profits given rising costs. Bloomberg cites IBES data from Refinitive showing Q2 y/y earnings growth of 5.7% which would be the slowest since Q4 2020 and down from 6.8% from April 1.

Twitter Inc TWTR.N sent a letter to Elon Musk saying his effort to abandon his $44 billion takeover is “invalid and wrongful” and that Twitter has not breached any of its obligations, according to a regulatory filing.

* USDIndex broken through the 108.00 level, currently at 108.32 – highest since October 2002.

* Yields: 10-year sector was the outperformer yesterday, back below the 3.00% level again to 2.97%.

Stocks: USA100 tumbled -2.26%. The USA500 is off -1.15%, and the USA30 has slid -0.52%.

* USOIL down to $102.00 support.

* Gold steady for a 3rd day at $1,730.

* FX Markets: EURUSD dip to within 4 pips of parity at 1.0004, USDJPY spiked to 137.47. The AUDUSD slumped and was one of the worst performers versus the USD amid growing recession angst that has overshadowed the two consecutive 50 bp hikes from the RBA.

* Today – PepsiCo earnings, German ZEW, & BoE’s Governor Bailey speech

Biggest FX Mover @ (06:30 GMT) GBPJPY (-0.25%) Fallen from a test of 164.50 on Monday, to 162.40 now, traded below 162.00 on Thursday. MA’s aligned lower, MACD histogram & signal line lower and below 0 Line, RSI 33.00 and falling. H1 ATR 0.287, Daily ATR 1.895.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 14 – Focus on PPI & Earnings.

Trading Leveraged Products is risky

It was all about June CPI and the report did not disappoint. Risk was for a hot report and the Administration warned of rising pressures. The most dramatic movers were the hot CPI report and the BoC’s 100 bp hike. Those opened the door for an outsized Fed move and in turn heightened risk for a recession. A bearish curve inversion play as the data nail the coffin for a 75 bp hike on July 27, with nontrivial risk of more aggressive action, either with a 100 bp increase which the BoC just effected, or with consecutive 75 bp moves in July and September. USD sustained gains, Oil settled at 200 DMA and Stocks traded mixed. Stocks were up 0.6% and 0.4% in Japan and Australia respectively, the latter helped by a record low unemployment report (50-year low) while Chinese imports continue to linger as the country’s Covid policy keeps a lid on activity. The AUD rallied on the numbers, as traders boosted speculations for a 75 bp rate hike from the RBA in August.

* USDIndex held above 108.00 level, but failed to break 3-day resistance.

* Yields: the 10-year ended over 7 bps lower at 2.89%, reflecting credibility in the FOMC’s policy stance. Fed funds futures priced in a 54% chance for a 100 bp rate hike on July 27 with rising odds for 170 bps in hikes from here.

* Stocks: USA100 tumbled -0.15%. The USA500 is off -0.45%, and the USA30 has slid -0.67%.

* USOIL traded at $95 holding above 200-day SMA.

* Gold found a bid but gains were trimmed. Currently down to $1,706.

FX Markets: EURUSD holds fractionally above parity at 1.0002, USDJPY skyrocketed to 139.28, Cable fell to * 1.1856. AUD and to a lesser extent the NZD gained.

* Today – US calendar has jobless claims and PPI, but the earning releases are in the spotlight with JPMorgan Chase & Co., Morgan Stanley, First Republic Bank, Cintas etc.

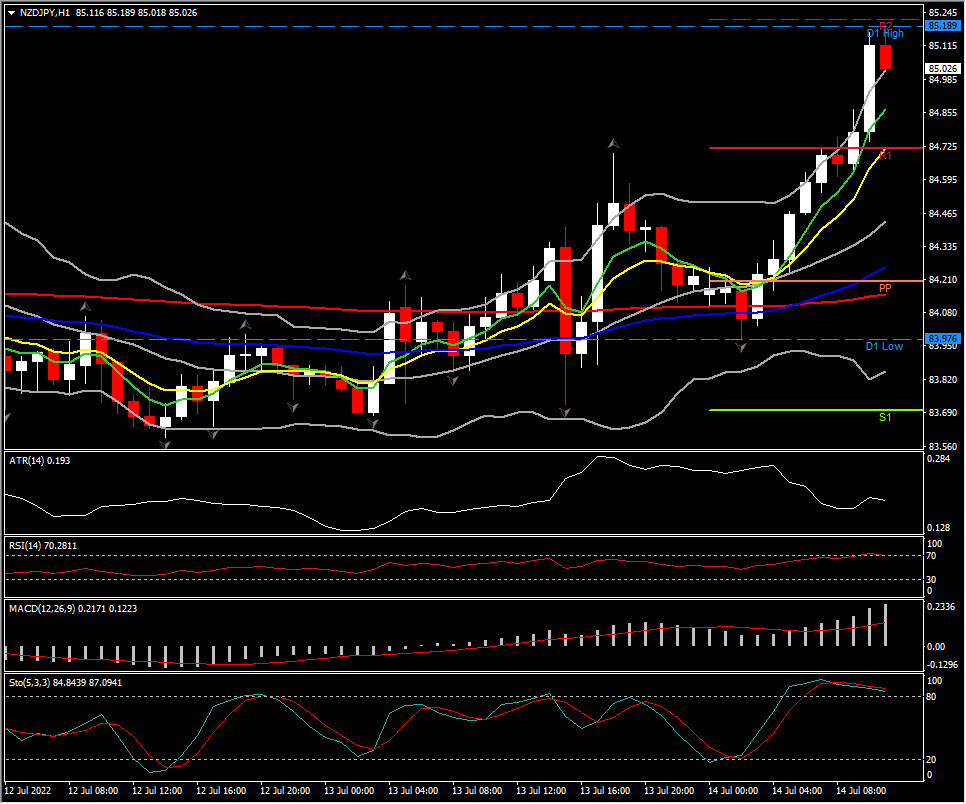

Biggest FX Mover @ (06:30 GMT) NZDJPY (+1.62%) breached 85.20. MAs aligned higher, MACD histogram & signal line extend further northwards, RSI above 701 but falling. H1 ATR 0.193, Daily ATR 0.975.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

USD steady at 108.50, Oil holds above 200 DMA, Stocks and bonds weaker on poor earnings news and bearish spillover from Europe on recession fears and political turmoil, and dove on the initial PPI print which kept the door open for a hefty 100 bp rate hike from the FOMC at the upcoming July 26-27 meeting. China bourses were under pressure after weaker than expected data that included a 0.4% y/y rise in GDP, which clearly missed expectations for a 1.0% y/y rise.

Equity Market: JPMorgan and Morgan Stanley missed earning forecasts. Net income at both lenders fell nearly 30% in the second quarter as work on IPOs and SPACs dried up. It was the first earnings miss from either JPMorgan — the largest US lender by assets and an industry bellwether — or Morgan Stanley since the start of 2020. Alibaba Group Holding Ltd. dragged Chinese tech shares lower as concerns about a crackdown on the sector resurfaced after company executives were reported to be facing an inquiry linked to the theft of a vast police database.

* USDIndex garnered strong early support and rose to 29on diverging central bank stances and political uncertainties before drifting to 108.55.

* Yields: the 10-year was 2.8 bps higher at 2.961%, versus a 3.02% intraday peak.

* Stocks: In China, fresh worries of regulatory pressure are adding to a decline in tech stocks. The ASX also struggled and corrected -0.7%, but the Nikkei found a footing and lifted 0.5%, with the GER40 gaining nearly 1%, the UK1004%, and a 0.2% rise in the USA100.

* USOIL traded at $95.50 holding above 200-day SMA.

* Gold near 5th consecutive weekly loss. Currently down to $1,704.73.

* FX Markets: EURUSD slumped below parity to 9952before it bounced to 1.0023, USDJPY is still at a very high level at 138.70, Cable at 1.1820.

* Today –US Retail Sales. Earnings: UnitedHealth Group, Wells Fargo, BlackRock, Citigroup etc.

Biggest FX Mover @ (06:30 GMT) CHFJPY (+0.56%) breached 141.66. MAs aligned higher, MACD histogram & signal line extend further northwards, RSI above 70 but falling. H1 ATR 0.212, Daily ATR 1.404.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 18 – Stocks Rally, Dollar Dips, Biden Fist Bump.

Trading Leveraged Products is risky

USDIndex continued last week’s slip to test 107.60. US data on Friday (Retail Sales, Empire State & UoM Con. Sentiment) all better than expected. Bullard talked 75bp not 100bp for July. US Stocks rallied into close (DOW +2.15%), despite misses from Wells Fargo & BlackRock. Asian markets positive, (Hang Seng +2.42%, Nikkei +0.43%). European FUTS positive too. Yields closed down -1.25% but the rate curve is still inverted. Oil up to $98, Gold up to $1714 BTC has rallied to $22k. Biden fist bumped Crown Prince Mohammed bin Salman but got little from visit, Yellen pushes minimum global corporation tax, IMF are “exceptionally uncertain” over global growth & Reuters report on 12 countries on brink of default.

Week Ahead – ECB & BOJ Rate Decisions, RBA Mins, a raft of CPI & Retail Sales data and Earnings Season gets into full swing including Banks & IBM today, Netflix, Tesla, Twitter and Johnson & Johnson later in the week.

* USDIndex slides further from Thursday’s 109.00 to 107.60 now as expectations of a 100bp rate hike next week recedes.

* Equities – USA500 closed +1.92% 72.54pts (3863), US500FUTS at 3897 now. Citi BIG Earnings beat +13.2%, Wells Fargo profits fell 50% but stock closed +6.2%, United Health +5.4%, BlackRock +2%, Netflix +8.2%, BAC +7.04%. 35 companies have reported; 80% have beat estimates.

* Yields 10-year yield higher, from close +2.92%, trades at 2.935% now.

* Oil & Gold had volatile sessions last week – USOil trades up back to $100 from $90.90 lows last week, following inconclusive Biden visit to Mid-East; OPEC next meet Aug 3. Gold fell under $1700, last week but back to $1714 now on weaker USD.

* Bitcoin rallied from $19K, testing $22.2K today on more chatter of major investments coming.

* FX Markets – EURUSD remains pressured at 1.0100 but moving up today, USDJPY down from 139.30 to 138.20 now. Cable trades back to 1.1900 from 1.1760 lows last week. Race to be new PM is reduced to two contenders this week. New PM Sept 5.

Overnight – NZ CPI hotter than expected (1.7% (32-year high at ) vs. 1.5%). NZD jumped too.

Today – Little economic data, speech BOE’s Saunders. Earnings – Bank of America, IBM, Goldman Sachs & Charles Schwab.

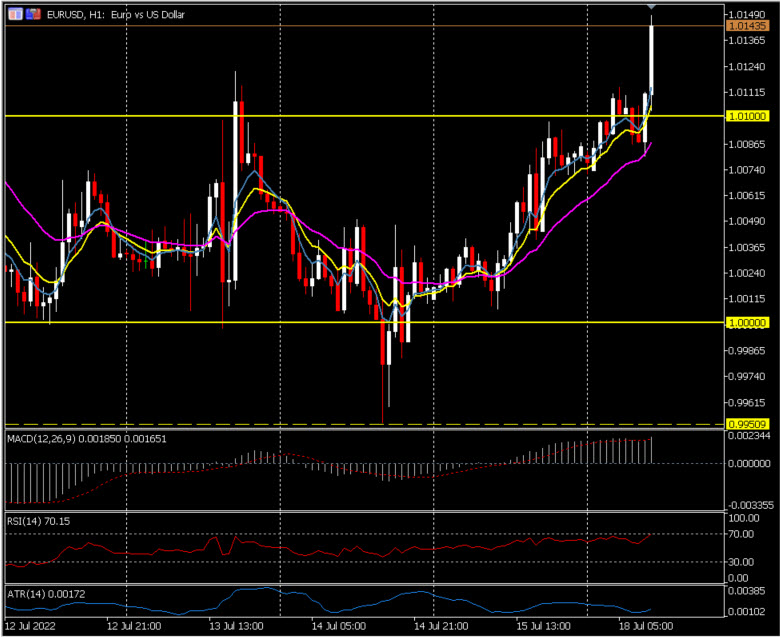

Biggest FX Mover @ (06:30 GMT) EURUSD (+0.68%). EUR rallying ahead of ECB this week ? From under Parity (0.9951) on Thursday to 1.01400 now. MAs aligned higher, MACD histogram positive but flat, RSI 69 & rising, H1 ATR 0.00172, Daily ATR 0.01088.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 19 – USD & Stocks Cool Ahead of Central Banks.

Trading Leveraged Products is risky

USDIndex continued last week’s slip and tested 106.80, before recovering. US Stocks dropped into close following +1% on open (NASDAQ -0.81%) after a plunge in the NAHB home builder index. Goldmans & Bank Of America, beat expectations but saw profits down -47% & -37%, respectively. IBM beat after hours, but shares fell -4.32%. Reports that Apple (-2.06%) is to freeze hiring weighed. Asian markets are choppy, (Hang Seng -0.82%, Nikkei +0.70%). European FUTS also mixed. Yields are up +1.72% & the rate curve is still inverted. Oil holds $100, Gold down to $1710 BTC holds at $22k. Gazprom warnings of European supply issues and 700 new Covid cases reported in China, weigh on sentiment.

Week Ahead – ECB & BOJ Rate Decisions, RBA Mins, a raft of CPI & Retail Sales data and Earnings Season still has more Banks, Johnson & Johnson and Netflix today,with Tesla, Twitter & Snap later in the week.

* USDIndex slides further to test 106.80 and rotates around 107.00 now as expectations of a 100bp rate hike next week evaporate. AUD outperforms in Asian session.

* Equities – USA500 closed -0.84%, 32.31pts (3830), US500FUTS at 3850 now. A strong +1% opening rally was wiped out following weak Housing data and the Apple news.

* Yields 10-year yield higher, into close at 2.986%, trades at 2.96% now.

* Oil & Gold had volatile sessions last week – USOil trades up back under $100 now from a test of $102.00 yesterday. Gold tested to $1724 yesterday but back to $1707 now.

* Bitcoin rallied to $22.8K yesterday and holds $22k now, on more chatter of major investments coming.

* FX Markets – EURUSD remains pressured but tested 1.0200 yesterday & back to 1.016 now and USDJPY is down again to 137.85 now. Cable tested back to 1.2000 from 1.1760 lows last week. Race to be new PM is reduced to two contenders this week. New PM Sept 5.

Overnight – NZ CPI hotter than expected (1.7% (32-year high at ) vs. 1.5%). NZD jumped too.

Overnight – RBA Minutes – “committed to doing what is necessary on inflation” no new insight, UK Earnings (6.2% vs. 6.8%) & Payrolls are weaker and CHF Trade Balance lifted 70 bln CHF.

Biggest FX Mover @ (06:30 GMT) AUDUSD (+0.60%). AUD continues to recover from last weeks 0.6680 low and no surprises today from RBA Minutes. Next resistance 0.6850 & 0.6900. MAs aligned higher, MACD histogram & signal line higher, RSI 67 & rising, H1 ATR 0.00124, Daily ATR 0.00908.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – July 20 – Stocks rallied; USD down.

Trading Leveraged Products is risky

USDIndex down to 106.52. US Stocks continued to rally overnight, after European and US markets posted broad gains yesterday (NASDAQ +3.11%) amid strong earnings and the expected resumption of Russian gas supply to Europe helping lift risk-on sentiment and ease fears of a recession. UK CPI inflation lifted to 9.4% y/y in June from 9.1% y/y in the previous month. Core inflation eased slightly, but at 5.8% y/y still remains far, far above target. German PPI inflation eased slightly.

Earnings: Netflix shares jumped after earnings beat; it lost fewer subscribers than expected and says cheaper ad tier is coming in early 2023. Boeing rose on deal to sell jets to 777 Partners, Johnson & Johnson and IBM fell on dollar impact warning, Halliburton, Hasbro & Truist rose after profit beat. Johnson & Johnson beat analysts’ estimates on strength in its pharmaceuticals unit, even as the company cut its full-year adjusted profit forecast due to a stronger Dollar. Twitter Inc. and Elon Musk will go to trial in October over whether the billionaire must complete his $44 billion acquisition of the social media company, a Delaware judge ruled on Tuesday. Amazon.com filed a lawsuit against the leaders of more than 10,000 Facebook groups it accused of publishing fake reviews on the e-commerce site, the company announced on Tuesday.

* USDIndex is mired at two-week lows to 106.52. It has fallen 2 handles in two days from a 20+ year high of 108.54 last Thursday.

* Equities – USA500 climbed 2.76%, USA100 surged 3.11% followed by a 2.43% jump in the USA30. JPN225 gained 2.7%, the ASX 1.7% and Hang Seng and CSI lifted 1.6% and 0.2% respectively.

* Yields 10-year Treasury yield is up 0.2 bp at 3.02%.

* Oil down to 98.70 & Gold steady at $1707.

* FX Markets – EURUSD has climbed to 1.0233 ahead of Thursday’s ECB meeting. USDJPY has corrected to 137.52. Cable at 1.2008.

Today – Canadian CPI. Earnings – Tesla, ASML Holding, Abbott Laboratories etc. For Europe the day of reckoning will come tomorrow when the ECB meeting coincides with the day the Nordstream 1 pipeline is supposed to re-open after scheduled maintenance work. If Russia doesn’t re-open and the ECB announcement disappoints Eurozone stocks and the EUR are likely to sell off in tandem with Eurozone peripherals.

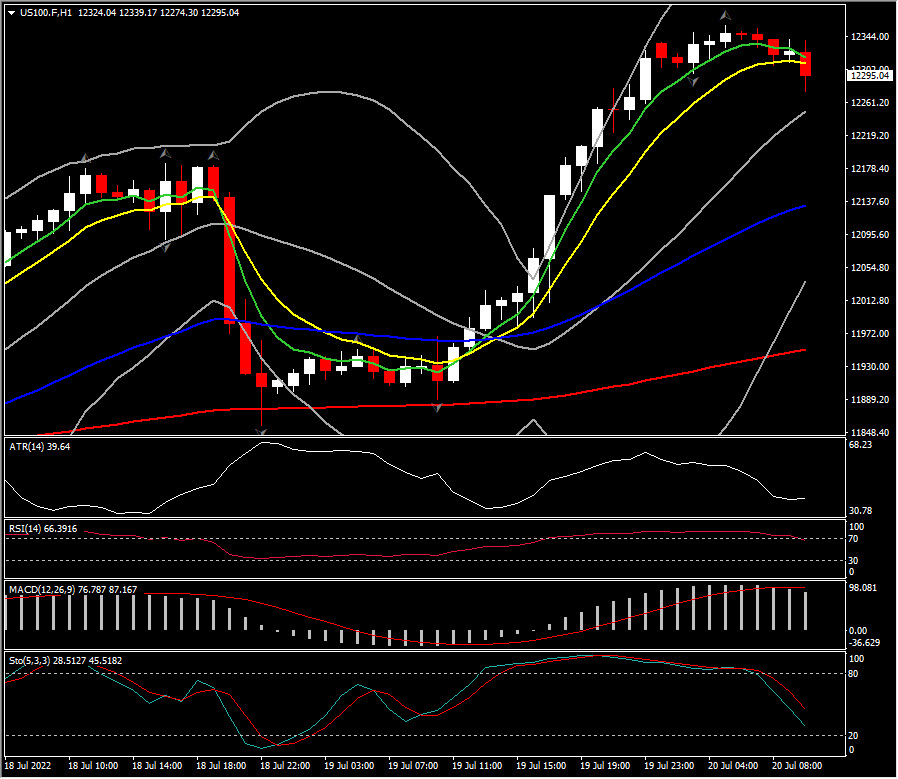

Biggest FX Mover @ (06:30 GMT) US100 (+3.10%). Spiked to 12,356. Next resistance 12,600 & 12,945. MAs aligned, turning lower in 1-hour chart, MACD histogram & signal line hold higher, RSI 66 but falling.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Новости

Новости Фотогалерея

Фотогалерея Клубы

Клубы Каталог

Каталог Оставить отзыв

Оставить отзыв Пользователи

Пользователи Объявления

Объявления Хостинг

Хостинг Технический анализ

Технический анализ Конкурсы фото

Конкурсы фото ПОЛНЫЙ СПИСОК

ПОЛНЫЙ СПИСОК Блоги

Блоги