The Dollar has traded moderately softer in thinning year-end markets. This has seen the narrow trade-weighted USD Index (DXY) ebb to a low of 97.30, down from the one-week high seen yesterday at 97.47.

A rebound in Cable has weighed on the US currency, with Sterling finding a footing after plunging by nearly 3.5% from last week’s post-UK election rally high at 1.3515. Cable’s low yesterday was 1.3060, and the pair has since recovered to the lower 1.3100s, though still remains over half a big figure below the levels that were prevailing ahead of the election.

The BoE’s Monetary Policy Committee has amid its final meeting of the year, and will announce at 12:00 GMT in London today. No change to prevailing settings is widely anticipated, though there will be a focus on the two dissenters, Saunders and Haskell, who last month voted for a 25 bps cut in the repo rate, to see if they will maintain their dovish dissent in light of the strong victory of the Conservative Party at last week’s election. Either way, we expect the BoE to remain on a neutral footing heading into 2020, though, with inflation running at three-year lows at 1.5% y/y, comfortably below target, the BoE won’t be in any rush shift to a tightening bias.

Elsewhere in forex markets, EURUSD lifted out of the one-week low seen yesterday at 1.1100, but remains mired in narrow ranges in what is now the sixth consecutive session trading on a 1.11 handle. USDJPY has also continued to ply narrow ranges, pivoting through though the pair still managed to scratch out a six-day high at 109.68, which is 2 pips shy of the 17-day high seen last Friday, and 4 pips shy of the seven-month peak seen on December 2. The Australian dollar recovered the losses seen following the wake of the RBA minutes on Tuesday following an above-forecast 39.9k gain in employment, along with an unexpected dip in the jobless rate to 5.2%, from 5.3%. AUDUSD posted a two-day high at 0.6883 moving some 0.42% during the Asian session.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

FX Update – Holiday Consolidation– 20th December 2019.

USDJPY, H4

Narrow ranges have continued to be the norm as markets wind down into the Christmas and New Year holiday period. EURUSD has mustered a less than 10-pip range so far today, holding in the lower 1.1100s in what is now the seventh consecutive trading day the pair has been trading on a 1.11 handle. USDJPY has managed a 15-pip range, with the base marked at 109.25. The pair is consolidating below the seven-month high at 109.72 seen in early December, which is the culmination of a rally from the late-August low at 104.45, a three-year low. Rallying global equity markets and a pricing out of Fed easing expectations have been keeping USDJPY buoyant.

While equity markets have settled today, the USA500 yesterday hit a sixth-straight record high, which is the longest streak since January 2018. All three major US indexes posted new record closing highs yesterday. The Santa Rally has certainly come to life this year, The gains came after US Treasury Secretary Mnuchin said the US and China would sign their Phase-1 trade deal trade pact in early January, and the US House of Representatives having approved the new North American trade deal.

Elsewhere among currencies, the Australian Dollar managed fresh highs, building on gains seen after yesterday’s above-forecast Australian jobs report. AUDUSD printed a one-week high at 0.6900. The Pound has found a footing after tumbling to fresh lows against the Dollar just after the London book closing yesterday. Cable posted a 16-day low at 1.2989, since recouping back above 1.3000, though set to close out today with its biggest weekly loss in just over two years

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Events to Look Out For Next Week 23rd December 2019.

*Brexit is finally getting underway and global trade talks progressing in this final weeks of 2019. Although, the risk around these events has been trimmed, ample uncertainties remain, leaving scope to further whipsaw markets into the new year.

Holiday-thinned staffing in Europe, Asia and the US in the middle of the week ahead will severely curtail trade, though what this means for volatility is anyone’s guess.

Monday – 23 December 2019

* Leading and Coincident Index (JPY, GMT 05:00) – The indices are expected to come out unchanged at 91.8.

* Gross Domestic Product (CAD, GMT 13:30) – The 0.1% gain that is expected for October GDP will keep Canadian GDP growth weak. Canada’s slowing in GDP growth during Q3 matched BoC expectations, in turn not moving the needle on the outlook for no change in rates for an extended period. GDP slumped to a 1.3% rate in Q3 (q/q, saar), identical to the BoC’s 1.3% estimate from the October MPR.

* BoJ Meeting Minutes (JPY, GMT 23:50) – The BoJ minutes, similar to the ECB Reports, provide a detailed assessment of the bank’s most recent policy-setting meeting, containing in-depth insights into the economic conditions that influenced the rate decision. They are usually a cause for FX turbulence.

Tuesday – 24 December 2019

* Christmas Eve – Early close for Major Markets

* Durable Goods (USD, GMT 13:30) – Durable Goods is the leading indicator of production in the US. November Durable goods orders are expected to grow 2.4% with a 6.7% bounce in transportation orders, after a 0.5% headline orders increase in October, and a -1.5% decline in September. Boeing orders for planes bounced to 63 in November from 10 in October, with a boost from the Dubai Air Show.

Wednesday – 25 December 2019

* Christmas Day – Nearly all major Markets closed

Thursday- 26 Decemmber 2019

* Boxing Day – Nearly all major Markets closed – Except US and Japan

* kyo Core CPI (JPY, 23:30) – Tokyo CPI is usually a good proxy for the Japanese economy’s overall inflation rate. In December, the CPI is expected to have stood at 0.6% y/y, the same as in November, even though projections may be revised when Retail Sales are taken into consideration.

* Retail Sales (JPY, GMT 23:50) – Following a precipitous 14.4% dive in October due to the Japan’s recent sales tax hike, Retail Sales are expected to climb slightly to 4.6% on a m/m basis in November. The overall rate is expected hold lower at 4.6% y/y decline from 7.1% y/y last month.

Friday – 27 December 2019

* EU Bulletin (EUR, GMT 09:00) – European Central Bank launches a new publication, the Economic Bulletin, to replace the ECB Monthly Bulletin. It is published two weeks after each Governing Council meeting and it contains the statistical data that policymakers evaluate when setting interest rates. The report also provides detailed analysis of current and future economic conditions from the bank’s perspective.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

XAUUSD – Trend towards the end of the year– 24th December 2019.

XAUUSD, Day – Although gold prices are significantly less volatile, due to the progress of trade negotiations between the US-China since October, however, this morning, gold prices continue rising further to a new high in the month of 1489.57. This followed as USD slight weakness on the disappointing US durable goods released last night. the data were not in line with market expectations while the uncertainty around Brexit and the US-China trade agreement remains.

In the technical perspective, volatility has clearly decreased since the end of October. The gold futures went down to a 3-month low of 1445.55 on 12 November and gradually sideway until the end of November within the lower territory of the downchannel seen since September. In December meanwhile it started moving northwards towards the upper trendline of the channel, which currently retests. Therefore, it is essential to look whether gold prices will be able to break through the upper border of the channel (solid line).

MACD lines meanwhile, have turn in the positive territory since the UK election day last week. A cross of the signal line above neutral zone could confirm the turn of Gold’s outlook into positive in the medium term.

In addition, during the holiday break, it is possible that the price of XAUUSD may be within the sideways framework, as thin trading conditions prevail.

However, during sparse trading, we sometimes see Flash Crash event as participants closing their positions for year’s end, similar to what we saw in the AUDJPY earlier this year. That is assumed to be caused by low trading volumes.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

FX Update – 2020 Day 1 -January 2– 2nd January 2020.

EURUSD, H1

The Dollar has found a footing after coming under pressure over the Christmas week and earlier this week. Liquidity has picked up, though some centres in Asia have remained closed, including Tokyo (still the most significant Asian market). The narrow trade-weighted USDIndex (DXY) has lifted above 96.50, up from the six-month low seen earlier in the week at 96.36. EURUSD has concurrently ebbed back under 1.1210 after pegging a four-month high at 1.1239 on Tuesday, but holds S1 and the key 1.1200 handle. The US currency is also showing moderate gains against most Asian currencies, including the Yen. USDJPY has lifted to an intraday high at 108.79, up from the three-week low that was seen earlier in the week at 108.47. USDCHF has been the best performing pair so far today, up some 0.41% and back over the key Daily support and psychological level at 0.9700. AUDUSD has also moved down to a key round number and support level at 0.7000.

Stock markets have opened the new year on a strong footing, aided by the PBoC’s decision, announced yesterday, to trim the reserve requirement ratio for banks and inject some 800 billion Yuan ($114.9 billion) in funds for lending, effective Jan. 6. This followed President Trump saying yesterday that the US-China phase-1 trade deal will be signed on January 15 in Washington. There has been no comment from China. The MSCI Asia-Pacific Stock Index rallied by 0.5%, building on the 5.6% gain that was seen in December. The MSCI’s all-country World Index has remained buoyant after posting a record high on December 27.

Elsewhere in the forex markets, the Pound has started the new year on a soft footing, reversing some of the gains seen over the last week. Brexit is set to happen on January 31, at which point the UK will enter an (at least) 11-month transition phase, during which time the country will remain in the EU’s single market and customs union.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

FX Update – January 3 – Risk Off & Weak EZ Data– 3rd January 2020.

EURUSD, H1

The Yen, and to a lesser degree, the Dollar have rallied amid a dash for safe havens following US air strikes that killed the head of Iran’s elite Revolutionary Guard’s overseas unit. The news also saw gold prices rally by over 1%, and oil prices by over 3%, while stock markets, richly valued after recent gains (Apple shares traded above $300 for the first time yesterday, for instance), declined.

Out of the main currencies, AUDJPY has, not surprisingly, been the biggest mover, with the cross showing about a 1% decline soon after the London interbank open. AUDJPY, which has rallied strongly amid the recent risk-on phase in global markets, dove to a two-week low to breach 75.00 and trade at 74.94. The Cross is down by over 2% from the highs seen on Monday. USDJPY plunged under 108.00 to a two-month low, at 107.90, while AUDUSD fell to a two-week low at 0.6935. The New Zealand Dollar, and most developing-world currencies, also declined, while the Canadian Dollar held up relatively well on the back of the rise in oil prices.

Elsewhere, EURUSD and EURJPY fell to respective one- and three-week low, at 1.1152 and 120.35. Cable and GBPJPY hit four- and eleven-day lows respectively. In stock markets, S&P 500 futures are showing a 1% loss after the cash version of the index hit fresh record highs on Wall Street yesterday. The MSCI Asia-Pacific index turned negative after opening strongly, correcting from 18-month highs. In Europe the GER30 trades down some 1.8% at 13,186.

EURUSD came under further pressure, breaching 1.1140, as German jobless numbers rose 8K, more than anticipated, French inflation jumped to 1.6% y/y in December, from 1.2% y/y in the previous month and Eurozone loan growth decelerated as loans to non-financial corporations declined to 2.6% from 3.1% in October.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Events to Look Out For Next Week 06th January 2020.

*As we have already entered 2020, with relatively good news in terms of economic growth, the progress on US-China trade, USMCA, Brexit, the fresh Hong Kong protests, ongoing uncertainty in the Middle East and central bank accommodation, will remain inevitably the key events of the year ahead.

Monday – 06 January 2020

* Markit PMIs (EUR, GBP, USD, GMT 08:55-14:45) – The German but also the overall Eurozone composite PMI reading for December are expected to hold steady. The UK Service PMI meanwhile, is expected to come out at a slightly higher level than last month but to remain below neutral at 49.2. The US Markit services rose to 52.2 in the first release from 51.6 in November and is anticipated to remain unchanged for December.

Tuesday – 07 January 2020

* Consumer Price Index (CHF, GMT 07:30) – Expectations suggest that Swiss inflation would have flattened at 0% y/y in December, compared to the fall to 0.1% last month. Meanwhile, the SNB downgraded inflation expectations for 2020 and 2021. The 2019 conditional inflation forecast stands at 0.4%, with a 0.1% forecast for 2020 and a 0.5% forecast for 2021.

* Consumer Price Index (EUR, GMT 10:00) – The Euro Area preliminary CPI is expected to come out a tad higher at 1.3% y/y in December, while Core is seen unchanged.

* Trade Balance (USD, GMT 13:30) – The trade deficit is expected to widen in November to -$50.8 bln from -$47.2 bln in October. The exports should rise 0.5% to $208.1 bln, while imports should grow by a larger 1.8% to $258.9 bln.

* Non-Manufacturing PMI (USD, GMT 15:00) – The index is expected to rise to 54.5 in December from 53.9 in November and a prior 19-month low of 56.1 in March, versus a 13-year high of 60.8 in September of 2018. Most of the “soft data” measures have oscillated around lean but positive territory since June, though with headline hits to some surveys from the UAW-GM strike that lingered into November.

Wednesday – 08 January 2020

* Building Permits (AUD, GMT 00:30) – Building permits are a known leading indicator of the housing and the overall market. Following the decline in dwelling approvals in October, it will be interesting to observe whether permits will increase or pullback once again. The consensus for November is at 4.0% m/m, compared to the drift at -8.1% last month.

* ADP Non-Farm Employment Change (USD, GMT 13:15) – The ADP Employment survey is seen at 150k for December following the lean 67k November ADP rise.

Thursday- 09 January 2020

* Australia’s Trade Balance (AUD, GMT 00:30) – The trade balance in November could spike to 6,100M from 4,502M last month.

* Consumer Price Index (CNY, GMT 01:30) –One of the restrains for PBOC to ease the monetary policy last year was the rising pork prices, a key component that stoked inflation. Declines in pork prices in December are likely to slow the CPI growth in this period.

* Unemployment Rate (EUR, GMT 10:00) – The Euro Area unemployment rate is expected to stand at 7.5%, the same as in October.

* Housing Starts (CAD, GMT 13:15) – Canadian housing starts are expected to remain positive at 205k, slightly stronger than the 201.3k November figure.

Friday – 10 January 2020

* Event of the Week – Non-Farm Payrolls (USD, GMT 13:30) – A 180k December Non-Farm payroll rise has been forecasted, following a 266k increase in November. The jobless rate should hold steady, average hourly earnings should rise 0.3% m/m, for a y/y gain of 3.1% for a second month in a row. The jobs data face upside risk from firm consumer confidence and a December up-tilt in producer sentiment, but downside risk from the rise in claims through the period of holiday volatility and a lean ADP path.

* Labour Market Data (CAD, GMT 13:30) – The plunge in November employment challenges the BoC’s economic resiliency argument. Employment fell -71.2k after a -1.8k dip in October, contrasting with expectations for a modest recovery, while the unemployment rate jumped to 5.9%. However, the December reading is anticipated to jump back to 20K while the unemployment rate is expected to fall at 5.8% m/m from 5.9% last month.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

AUD Pressured as tensions persist– 7th January 2020.

AUDUSD, H1

The Australian Dollar has remained under pressure, despite global stock markets having taken a turn higher as markets reappraise the US versus Iran standoff. A Caixin report saying that China will not increase its annual low-tariff import quotas for US agricultural produce raised doubts with regard to the yet-to-be-signed “phase-1” trade deal. There was also a research note from Citi analysts highlighting that upside Chinese data surprises have been diminishing since mid December. This appeared to weigh on the Aussie, which is widely seen as a liquid China proxy currency.

AUDUSD dropped just over 0.5% in making a two-week low at 0.6898, while AUDJPY fell by a similar magnitude in making a 26-day low. The pairing and cross are showing respective losses of 1.9% and 1.6% from their closing levels on December 31. Australian OIS is pricing in a 54% probability for the RBA to cut interest rates by 25 bps at its early February policy meeting, up from the around 38% odds that were being factored in late December. Of all the Aussie crosses it is the perky Pound that is the best performer in the London session, up some 0.62% and also printing five-day highs against the Dollar, Euro and Yen today.

Elsewhere, the Yen weakened against the Dollar and some other currencies, outside the case for AUDJPY, as some of its safe haven premium unwound, though firmed back some in the latest phase. USDJPY lifted to a 108.50 rebound high, up from yesterday’s 107.77 low. The Dollar traded mostly firmer, retracing losses seen yesterday by varying degrees. The narrow trade-weighted USDIndex (DXY) rebounded about half of the drop it saw yesterday in lifting back above 96.75. This saw EURUSD ebb back under the 1.1200 level to trade down to 1.1185.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

FX Update – The Usual Suspects & USDCAD– 8th January 2020.

USDCAD, H1

The Yen surged and then sharply unwound gains in volatile trading during trading in Tokyo. The rally in the Japanese currency was part of a broader dash for safe haven assets and currencies following news that Iran had fired missiles at two US bases in Iraq. The US reported no casualties, and President Trump’s initial tweet responses were notable for the lack of bellicosity, saying that “All is well!” and “So far, so good.” Official Iranian statements were also measured, though warned of “a painful response” to any further US action, while the Islamic Revolutionary Guard Corps said that “Operation Martyr Soleimani” had only just begun. The more hawkish members of Trump’s Republican party also signalled that Tehran had gravely miscalculated US resolve. Trump said he would make a statement later today, which will be a major focus for markets. More volatility in global markets seems assured given the uncertainty about the situation, although both sides are showing a clear desire to avoid a full-blown war.

The burst of Yen buying drove USDJPY to a three-month low at 107.65 before the pair rebounded to near net unchanged levels in the mid 108.00s. The rebound mirrored a recovery in stock markets in Asia, though most of the indices across the region, while off their lows, have remained firmly in the red. Oil and gold prices also spiked to fresh trend highs before retreating some. EURUSD remained in a narrow range around 1.1150. Sterling ticked moderately higher, but remained within its respective Tuesday ranges against the Dollar and Euro. AUDUSD printed a fresh three-week low at 0.6850 before rebounding back above 0.6880.

USDCAD dropped back below 1.3000 concomitantly with oil prices rising to fresh trend highs following the overnight news. The pairing remained above the three-month low seen on December 31 at 1.2951. The surge in oil prices over the last several months, which has been extended by the flare-up in US-Iran tensions, has been underpinning the Canadian Dollar. USOil is up by some 24% from the lows seen last September. Gains of that magnitude, if sustained, are a big boon to Canada’s terms of trade, hence the correlation between oil prices and the Canadian currency. The Fed’s removing of a forecast for a 25 bps hike in 2020 at its FOMC policy meeting in December has also been weighing on USDCAD, with markets presently discounting about 60% odds for the Fed to cut rates by 25 bps or more by the end of 2020. The pairing looks likely to continue to trade with an overall downside bias. A breach of the 1.2950 support area will bring 1.2900 and even the September 2018 low of 1.2780 into play. A sustained break and breach of 1.3000-50 is required for the pair to move back to the upside. The 20-day moving average and S3 sit at 1.3100.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Yields moved higher and stock markets bounced back, as investors bought into hopes that the US and Iran will step back from deeper military conflict, despite two rockets exploding near the US Embassy in Baghdad last night.

Fears of an immediate escalation into war in the Mideast have been scaled back for now, following Trump’s address on Iran, although the situation clearly remains fragile. The president said Iran appears to be “standing down”, and made no mention of further US military actions. Iran’s overnight missile attack aimed at US forces in Iraq looked to be more of a face-saving operation than anything, and looks to have gone some way to calm markets.

Indeed, Wall Street has rallied sharply following the speech, while Oil prices have tanked. The risk-back-on reaction has been the main driver of USDJPY strength as well. The pair rose to 109.28 amid a broadly weaker Yen, from near 108.60 earlier.

After crossing the 20- , 50- and 200-day SMA yesterday, the asset looks ready to sustain the bullish sentiment in the near term as today’s move above Wednesday’s peak suggested more positive bias in the short term, even in the case of fading geopolitical tensions.

The key upside level comes at the 6-month high and December’s Resistance at 109.70. Hence it will be interesting to see if there is a break above at the end of the day/week. However, as we have already entered the European session bulls might face some short-term dips in the next few hours as the USDJPY presents overbought signs, with RSI testing the overbought barrier while the candles have been flirting with the upper BB line in the past 5 4-hour sessions. Immediate Support area is at 109.00-109.14.

This said, 109.00 is a key Support level pointing towards a move lower as it will attract sellers getting back in business, while 109.70 is a significant Resistance level pointing towards a switch from a neutral outlook into a positive one in the medium term basis.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

FX Update – JPY Weak & NFP Preview10th January 2020.

USDJPY, H1

The Yen posted fresh lows as global stock markets hit new record highs, (APPLE, the world’s largest company, moved up over 2% to $308 following good iPhone sales in China) while the likes of the Australian Dollar and many developing-nation currencies rallied. USDJPY, now in its fifth consecutive up day, printed a fresh two-week high at 107.60, which is just 12 pips shy of the seven-month high that was seen in early December. A close over 109.50 today would suggest more upside for the pair next week. AUDJPY lifted to a five-day high and was the best performing pair, moving 0.33% and holding over 75.25, having topped at 75.41 and rolled over from its overbought condition at the London open. EURJPY also rose to an eight-day high.

In stock markets, the MSCI All-Country World Index hit a new record high today, which followed the record highs that the three main US indices and the pan-Europe Stoxx 600 Equity Index saw yesterday. Oil prices remained heavy, some 11% down on the high seen just a couple of days ago, with the US and Iran having stepped back from the cliff edge. News that iPhone sales in China rose 18% y/y in December gave tech stocks a boost, while also boding well for US-Sino relations, with China’s Vice Premier Liu, head of Beijing’s trade negotiation team, travelling to Washington next week to sign the phase-1 trade deal with the US.

Elsewhere in the forex markets, the Dollar has traded mixed, leaving the narrow trade-weighted USDIndex (DXY) net unchanged. EURUSD remained settled in a narrow range near 1.1100. The Dollar lost ground to the Australian currency, with AUDUSD lifting to a two-day high at 0.6882 in what is the pair’s first up day of the year so far. Cable remained below the 1.3100 level, while USDCAD settled just above 1.3050, below the two-week high seen yesterday at 1.3104.

The release of the US December employment report will be a major focus for markets today. Expectations from the monthly Reuters poll have the median increase for NFP set at 164k with a range extending from 125k – 2266k. However, there is potential downside risk from weak producer sentiment, the rise in claims through the holiday period, and a lean ADP jobs path, even though Wednesday’s number was a significant beat at 202K versus expectations of 150k.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

FX Update January 13 – Sterling Stressed 13th January 2020.

GBPUSD, H1

Sterling has taken a turn lower in early week trading, with markets reacting to both dovish BoE-speak and to a report from the UK’s Institute for Government finding that it will be impossible to deliver the computer systems for the special arrangements for Northern Ireland’s border by the end of the year. Prime Minister Johnson has pledged, and worked into the Withdrawal Agreement legislation, to leave the post-Brexit transition period by the end of the year, hence the negative reaction by markets. Ireland’s deputy Prime Minister Coveney also said that forming a new trade deal between the EU and UK is “probably going to take longer than a year.” Member of the BoE’s Monetary Policy Committee Vlieghe, meanwhile, said in the FT over the weekend that he is ready to cut rates if data doesn’t improve, similar to the view expressed by governor Carney last week. Cable has dropped nearly 0.5% in printing a 17-day low at 1.29845, while EURGBP has risen by a similar magnitude in making a 17-day peak at 0.8560. However, the biggest mover has been GBPAUD down some 0.55% and trades blow 1.8800 once again.

Elsewhere, EURUSD has lifted above its Friday high in making 1.1132 in a move driven by moderate Euro outperformance. EURJPY has posted a two-week high at 122.05, while EURCHF and other Euro crosses have also seen gains. The Yen remained on a generally weak footing as Asia’s MSCI Asia-Pacific index hit a new 19-month high with investors anticipating Wednesday’s signing of the US-China phase-1 trade deal. USDJPY was buoyant, though remained below Friday’s 18-day high at 109.68, and could not close the weak over 109.50, strong resistance sits at 109.70. AUDJPY posted a fresh 10-day peak. AUDUSD posted a six-day peak. Liquidity was below par in Asia with Japanese markets closed for a public holiday. The US-China trade deal will be a major focus this week as the details haven’t been made public, a reported 86-page document is to be signed and questions remain over Chinese compliance and their ability to actually fulfill their obligations and from the US side, their willingness to reimpose tariffs in an election year.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Optimism pressures Safe Havens while Crypto rallies

Optimism pressures Safe Havens while Crypto rallies – A fresh injection of risk-on trading saw the Yen decline further and stocks rally overnight after trade data out of China showed a drop in exports to the US last year.

[MEDIA=youtube]oxXJDxJtdws[/MEDIA]

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

GOLDMAN SACHS and the 4th Quarter of 2019 15th January 2020.

As Earnings season is kicking off again, focus is on the Banks’ reports this week. JP Morgan, City Group and Wells Fargo published their Q4 2019 reports yesterday before the US market open. JP Morgan and City Group beat expectations strongly, whilst Walls Fargo missed and saw its shares falling over 4% right after the report.

Today, investors’ attention is on whether Bank of America and GS will follow JP Morgan’s success story.

Goldman Sachs is scheduled to release its Q4 and full-year 2019 results before the US market open. In Q3 2019, the bank beat revenue forecasts but missed in earnings, while it posted a decline in Revenue and earnings in comparison with the previous quarter, affected by weakness seen in Investment Banking and Lending. Overall, in the past 2 years it has beaten earning and revenue estimations 88% of the time.

GS , in an attempt to improve its profitability and stock performance, has proceeded with several changes and several restructure and expansion plans for the near future and also the next 5 years. One of their latest projects, which was launched in August, was the development of credit cards with Apple, while they also introduced a long-awaited app last week (January 8), which according to Reuters, ” will integrate with the financial giant’s digital bank, Marcus”. Marcus is Goldman Sachs’s consumer banking unit, which was founded by Goldman Sachs in 2016, named after the bank’s founder Marcus Goldman.

In the long term meanwhile, GS has focused on its request to the China Securities Regulatory Commission (CSRC). As the China Morning Post stated, GS is one of the US banks which has an official branch in China and has been applying to the China Securities Regulatory Commission (CSRC) since last August to take majority control of its venture known as Goldman Sachs Gao Hua Securities, seeking to raise its stake to 51% from 33%. The hiring push on the mainland is part of the US bank’s new five-year plan in which Chief Executive David Solomon is looking to improve its profitability and share price performance.

It will be interesting to see whether all the above expansion plans will affect the bank’s earnings report today, but also how they could expand its wealth management business and broaden its revenue streams in 2020.

Zack’s estimates for Q4 Earnings are:

EPS Estimate: $5.20

Sales Estimates:

* Low: 8.70B

* High: 8.82B

* Year over Year Growth: 8.37%

Earnings Estimates:

* Low: $4.54

* High: $5.42

* Year over Year Growth: -13.91%

Technical overview:

The monthly chart shows the free fall seen on GS shares in 2018 to $151.60 from its all-time high in March 2018 at $275.60. In 2019, shares managed to recover by nearly 78%, as the price moved successfully to $274.64.

However, in the Daily chart, momentum indicators suggest that positive bias is starting to lose some ground , with OBV indicator unable to move further to the upside, suggesting nearterm weakness. The asset price is still moving upwards, however it’s moving outside the upper Bollinger Bands area, with RSI crossing above 70, both suggesting that the asset looks overbought. This comes in line with OBV. Hence from a technical perspective a correction could be seen in the medium term as the asset is overbought. From the data perspective, positive bias could theoretically strengthen if the upcoming earnings report beats expectations.

Resistance levels: $249, $261, $275

Support levels: $236, $227, $214

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

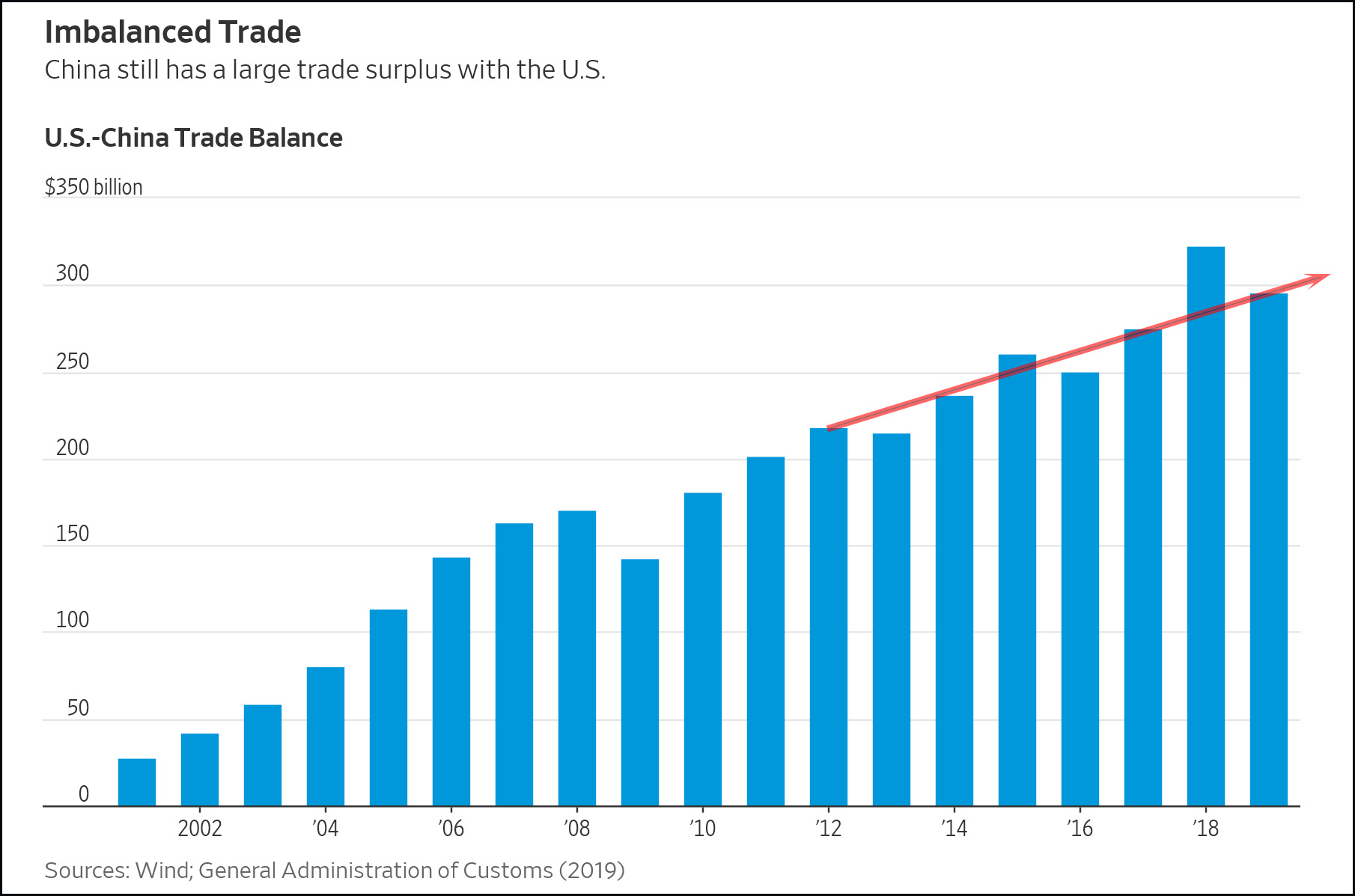

Narrow US trade gap in Q4 – Its meaning and what to expect in 2020? 16th January 2020.

A drop in the bilateral trade deficit between the US and China in Q4 sharply understates the underlying improvement, thanks to a powerful seasonal pattern in goods trade between the two countries that bloated the Q4 deficit. A plunge is anticipated in the gap to a February trough that should mark the narrowest deficit since 2013.

Though the overall US trade gap will widen in 2020 if the economy grows, phase-one agreement will be followed by news over the coming three months of a collapsing US-China trade deficit.

The US-China trade deficit for goods narrowed sharply last winter to just $20.7 bln in March of 2019 from a peak of $43.1 bln in October of 2018, with a gyration that was exacerbated by tariff front running.

The seasonal widening into Q4 of 2019 failed to occur, while a seasonal narrowing is expected into the Lunar New Year that should prompt a February goods deficit in the $20 bln area — less than half of the peak just 16 months earlier.

The seasonal pattern is mostly driven by the US import data from China. The unusually large gyration in 2018 was due to tariff front running, which pulled imports ahead into Q4 from Q1. Goods imports appeared to resume their seasonal climb until they reached a $41.5 bln level in July of 2019, leaving an -11.9% shortfall from July of 2018. From their, the seasonal climb oddly ended, and imports fell to just $36.5 bln in November to leave a y/y drop of an enormous -21.6%.

If the seasonal drop now unfolds, imports from China should fall to the $28 bln area by February. The drop will be exacerbated this year by a relatively early Lunar New Year date of January 25.

The seasonal pattern for imports has been quite stable over the years, until the big deviation in the pattern in 2019, which suggests that the atypical seasonal behavior this year is due to the “trade war.”

The seasonal pattern is less stable, and less pronounced, for US goods exports to China, and the pattern of US exports has been fairly erratic over the last year. The dominant pattern over the past two years has been a drop in US exports to China between the start of the “trade war” in early 2018 to a trough in January of 2019, before largely stabilizing since then.The fact that Chinese policymakers cut all unnecessary trade with the US over this period, leaves little room for further cuts through 2019 and into 2020.

Beyond the “trade war,” there have been two other major patterns in the US trade data that will likely have the effect of narrowing the US-China bilateral trade deficit over the coming year. One is the depressing effect on US exports from the 737 MAX grounding since March of 2019, leaving a likely dramatic rebound over the year following the lifting of the FAA ban presumably later this year. The other major pattern is the steep climb in US exports of petroleum products, as the Permian Basin is rapidly transforming into a major export center thanks to ongoing innovations in pressurized and lateral drilling.

The seasonal patterns are expected to allow a deficit to return for the last time between December and April, before the US becomes a “permanent” net petroleum exporter. China is dependent on petroleum imports, and hence it is anticipated that US exporters capture more of this market over the coming years, especially given that the phase-one deal involves a shift in Chinese purchases toward US commodities.

The combination of a narrowing US-China trade deficit, strength in US exports of petroleum-related products, and an assumed Boeing-led surge in capital goods exports at some point this year, may all suggest a narrowing US trade gap.

Hence to be sure, as the trade gap declined to the lowest during Donald Trump presidency, will add to GDP if not in the long term definitely in the near term, possible during February-March with help from the Chinese New Year and Phase-1 deal.

Overall however, a US GDP growth out-performance versus other countries in 2020 is anticipated, and a firm Dollar with strong capital account inflows, that should fuel a widening trade deficit through the year despite the narrowing bilateral gap with China.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Positive bias on the back of US & Chinese Data 17th January 2020.

Positive bias on the back of US & Chinese Data – Sentiment was supported by robust US retail sales on Thursday, ongoing good will following the Phase One trade deal and good earnings data, despite the slowdown of Chinese GDP growth to the lowest in 29 years.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Events to Look Out For Next Week 20th January 2020.

*An important week is coming up with regards to economic announcements and central banks, as PBoC, BoJ, BoC and ECB rate decision are expected to take place although none are expected to shake the market. Meanwhile, reduced liquidity will define trading on Friday as the Chinese Lunar New Year holiday begins.

Monday – 20 January 2020

* Interest Rate Decision (CNY, GMT 01:30) – The PBoC is expected to keep its interest rates at 4.15%.

Tuesday – 21 January 2020

* Interest Rate Decision and Conference (JPY, GMT 03:00) – The central bank signaled its commitment to keep interest rates at current levels “for an extended period of time, at least through around spring 2020”. The BoJ Governor said in his last statement that cutting rates further is a possible policy option, adding that he doesn’t think that Japan is near the reversal rate. He also said that he doesn’t think the BoJ needs to change the forward guidance for now. Hence this is likely to remain the scenario in this week’s Monetary Policy Statement.

* Employment and Earnings (GBP, GMT 09:30) – Earning growth excluding bonus is expected to have declined by 3.4% in November, below the 3.5% the previous month. The ILO unemployment rate (3M) for November could rise to 3.9% from 3.8%.

* ZEW Economic Sentiment (EUR, GMT 10:00) – German Economic Sentiment for January is projected at 4.3 from the 10.7 seen last month, as the current conditions indicator for Germany turned negative. The overall Eurozone reading though is expected to decline further to 5.5 from 11.2. A lower than expected outcome ties in with the stagnation in market sentiment at the start of the month.

Wednesday – 22 January 2020

* Consumer Price Index and Core (CAD, GMT 13:30) – The average of the three core CPI measures for December is expected to have come out slightly lower than last month, at 2.1% y/y from 2.2% y/y. The CPI backstops continue to back the BoC’s steady policy outlook.

* Interest Rate Decision and Conference (CAD, GMT 15:00) – No change is seen in the current 1.75% policy setting, alongside an announcement and MPR that are consistent with steady policy through year end.

Thursday- 23 January 2020

* Labour Market Data (AUD, GMT 13:30) – Australia’s recent employment report showed a slowdown in jobs growth also affected by the bushfires crisis. In December, the unemployment rate is anticipated to jump back to 5.3% while the employment change is expected to fall to 14K from 39.9K last time.

* ECB Interest Rate Decision and Conference (EUR, GMT 12:45 & 13:30) – The ECB is expected to keep policy on hold in January as policy review starts. The ECB kept policy on hold and re-affirmed easing bias at the December policy meeting.

* Consumer Price Index (NZD, GMT 21:45) – The overall New Zealand CPI for Q4 should rise to 2.2% y/y from 1.5%.

* Monetary Policy Meeting Minutes (JPY, GMT 23:50) – The BoJ Minutes report provides the BoJ Members’ opinions regarding the Japanese economic outlook and any views regarding future rate changes.

Friday – 24 January 2020

* Chinese New Year’s Eve – Asia Markets closed

* Markit PMI (EUR, GMT 09:00) – The prel. December manufacturing PMI was revised up to 46.3 from 45.9, still down from 46.9 in November. The manufacturing sector has been stuck in recession for eleven successive months. The composite PMI for January meanwhile is expected to be lifted to 51.0 along with a possible rise in services.

* Markit PMI (GBP, GMT 09:30) – The prel. UK Services PMI for January is forecasted to register a downwards reading to 49.4 after the upwards revision last week at 50.0.

* Retail Sales (CAD, GMT 13:30) – Retail Sales should register a gain in November to 0.1%, after the -1.2% plunge to 0.1% in total sales values in October.

* Manufacturing PMI (USD, GMT 15:00) – The Manufacturing PMI is expected to have decreased to 52.3 in January, compared to 52.4 in December.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

FX Update – US Closed & USD Softer 21st January 2020.

EURUSD, H1

The Dollar has seen modest weakness in quiet early-week trading. Volumes are likely to remain on the low side today with US markets closed for the Martin Luther King holiday.

Stock markets in Asia remained buoyant after bellwether indices in the US and Europe hit record highs (again) on Friday. Mostly upbeat earnings, reduced trade uncertainty and, more fundamentally, accommodative central banks (the Fed’s capping of repo rates is of particular note, which has swelled its balance sheet by 11% since last September) along with a persisting benign inflationary picture, have been maintaining the bull run on global stock markets.

EURUSD steadied after dropping over the last two days of last week, which left a 10-day low at 1.1085. Earlier, German PPI inflation ended 2019 at -0.2% y/y, up from -0.7% y/y in November and in fact a tad higher than anticipated. However, the uptick was mainly due to the fact that negative base effects from energy prices fell out of the equation, which was already evident in HICP readings and thus the PPI number doesn’t change the overall outlook. Inflation remains too low for the ECB’s liking and both the definition of the benchmark inflation rate and the target itself are set to the part of the ECB’s strategic policy overhaul that is set to start in earnest this week. EURUSD is once again testing the 1.1085 and the key 61.8 Fibonacci level at 1.1079, and S1 sits at 1.1070 and the December/November low 1.0980.

USDJPY went into narrow-range mode, posting just less than a 15-pip range in Asia through to the open of the London interbank market. Cable edged out a five-day low at 1.2985, and EURGBP lifted above its Friday peak in making a high at 0.8456. The possibility of the BoE cutting rates at its MPC meeting this Thursday should keep the Pound under pressure. The UK finance minister remarked over the weekend to the Financial Times that the UK would not be a “ruletaker” after Brexit, urging businesses to “adjust”. This has been taken negatively by businesses and has also weighed on Sterling today. USDCAD ebbed fractionally lower, to a 1.3055 low, which is near the midway point of the range seen over the last week.

Oil prices rallied at the opening of trading today, which sent front-month USOil to an 11-day high at $59.66. Reports that two large production sites in Libya closed in the face of military blockades (the country is amid a long-running civil war) underpinned prices. This was ahead of the Libya Conference in Paris at the weekend and seen as muscle flexing by the main opposition group. Elsewhere, AUDUSD recouped nearly half of the decline seen on Friday in carving out a high at 0.6888. The Aussie Dollar on Friday printed a 10-day low at 0.6871. RBA money markets positioning has continued to imply a 56% probability for the RBA trimming the cash rate by 25 bp at its February-4 policy meeting, unchanged since last Thursday.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Bitcoin – Exposed to corrections; bias cautiously bullish 22nd January 2020.

Bitcoin, Daily and Weekly

For the past two days, Bitcoin has been consolidating gains seen during January in a a safe haven play on rising concerns about the US-China trade war, geopolitical tensions and Iran sanctions, but also following the launch of options on the CME Globex.

Bitcoin staged a stunning upside reversal around the $6,400- $6,800 support area a week ago, with the price surging back above the 200-day Simple Moving average and towards two-month highs.

Currently however, sellers are pushing for a recoil below the 61.8% Fibonacci of $8,562 of the downleg from $9,904 to $6,407, a break of which could see the retest of the $8,148 barrier, which reflects the 50% Fibonacci level. Particularly if the 50% Fibonacci does not hold and sellers move below it, then the $8,000 number could come back into play.

However, moving higher, above the psychological resistance at $9,000, could next captivate trader’s attention and trigger another bullish action towards $9,570 – $9,904, i.e. the October-November upswings.

Still, with the RSI close to overbought waters,as the indicator moves softly towards its 70 overbought mark, downside corrections cannot be ruled out in the near term. On the contrary, MACD lines keep gaining ground in the positive territory. If MACD and RSI keep gaining ground in the positive territory, the price may continue to head higher.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

How To Improve Your Trading Mindset 23rd January 2020.

Our Head Market Analyst, Stuart, explains how to improve your Trading Mindset. Understand the importance of emotional control and discipline through an unmissable Q&A session.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HotForex Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Новости

Новости Фотогалерея

Фотогалерея Клубы

Клубы Каталог

Каталог Оставить отзыв

Оставить отзыв Пользователи

Пользователи Объявления

Объявления Хостинг

Хостинг Технический анализ

Технический анализ Конкурсы фото

Конкурсы фото ПОЛНЫЙ СПИСОК

ПОЛНЫЙ СПИСОК Блоги

Блоги